To the thousands of Dads out there that read Rate of Return every week — we hope this day is a time for you to unwind and be celebrated.

Here’s your absurd fact of the day:

Interest alone on U.S. debt is expected to soon become the 4th largest expense of our government — even ahead of defense.

Interest on the debt is +25% compared to previous year and on pace for $900 billion on an annualized basis.

Interest expenses for the month of May were higher than that of veterans benefits & services, education, and transportation COMBINED.

Portfolio Updates:

Quick little reminder / update to all of the new folks who have joined us over the last several weeks after going viral on TikTok a few times in June — I’m actively building a dividend growth portfolio while opportunistically investing toward companies who are newly or expected to be free cash flow positive for the first time.

As you might remember from the post below — if you can predict the cash flow you, you can predict the stock price.

A few names I’m especially excited about right now from a cash flow perspective include:

Monday.com (MNDY)

Unity Software (U)

Uber Technology (UBER)

Paycom Software (PAYC)

Napco Security Technologies (NSSC)

My dividend growth portfolio (shown above) has been largely riding the ups and downs of the market for the last several weeks as most of my investable cash has been deployed into retirement accounts (index funds).

Now that those have been largely taken care of, I’ll begin deploying new capital into this account over the coming week or two.

Some of my most exciting non-dividend paying companies in the portfolio include Palo Alto Networks (PANW) and Crowdstrike (CRWD) as I believe both of these companies will continue to take market share of arguably one of the most important industries right now (cybersecurity).

Expect another “Top Stock Ideas” post to come from me this week as I have a few “small cap” ideas for the rest of 2023 I’m eager to share. Stay tuned!

Week in Review — Too Long, Didn’t Read:

Adobe continues to soar, Kroger is a hold in my dividend portfolio (for now), Oracle seems to have decelerating growth, CAVA gives hope to the IPO market, Retail Sales rise once again, JPMorgan settles in Epstein case, Jerome Powell gives a hawkish vibe amidst the rate hike pause, and inflation readings continue to move in the right direction.

Key Earnings Announcements:

Adobe’s digital media bookings saw their largest quarterly growth in two years, Kroger is worried about disinflation impacting profits in the future, and Oracle seems overvalued.

Adobe (ADBE)

Key Metrics

Revenue: $4.8 billion, an increase of +10% YoY

Operating Income: $1.6 billion, an increase of +6% YoY

Profits: $1.3 billion, an increase of +10% YoY

Earnings Release Callout

“Adobe delivered outstanding net new ARR and profitability in Q2, positioning us to raise our annual targets. Adobe’s ground-breaking innovation positions us to lead the new era of generative AI given our rich datasets, foundation models and ubiquitous product interfaces.”

My Takeaway

In our last update on the company I mentioned a few concerns, mainly their operating cash flow and lackluster +10% revenue growth expectations. Operating cash flow reported $110M higher than expected and revenue was in-line with expectations — a win in my book.

Adobe has been one of the larger “risky” positions I hold — now up +88% since opening the position earlier this year. I also shared the name as one of my favorite AI plays in this post last week, and it sure paid off (up +9% in one week)!

So is Adobe still a good idea at $495 / share?

I’d argue yes — here’s why:

Digital Media bookings experience their largest quarterly upside in two years and is set to continue this trend throughout the rest of 2023.

This quarter’s operating margin of 45.3% reflects the first year-over-year increase in six quarters and will likely remain at these levels.

Their free cash flow of $2.1 billion was $80M higher than expected — an incredibly important metric for me as an investor.

Above is Adobe’s stock price (in black) in relation to their free cash flow (in blue) — I believe the company is still undervalued / fairly valued and I’ll continue to dollar cost average.

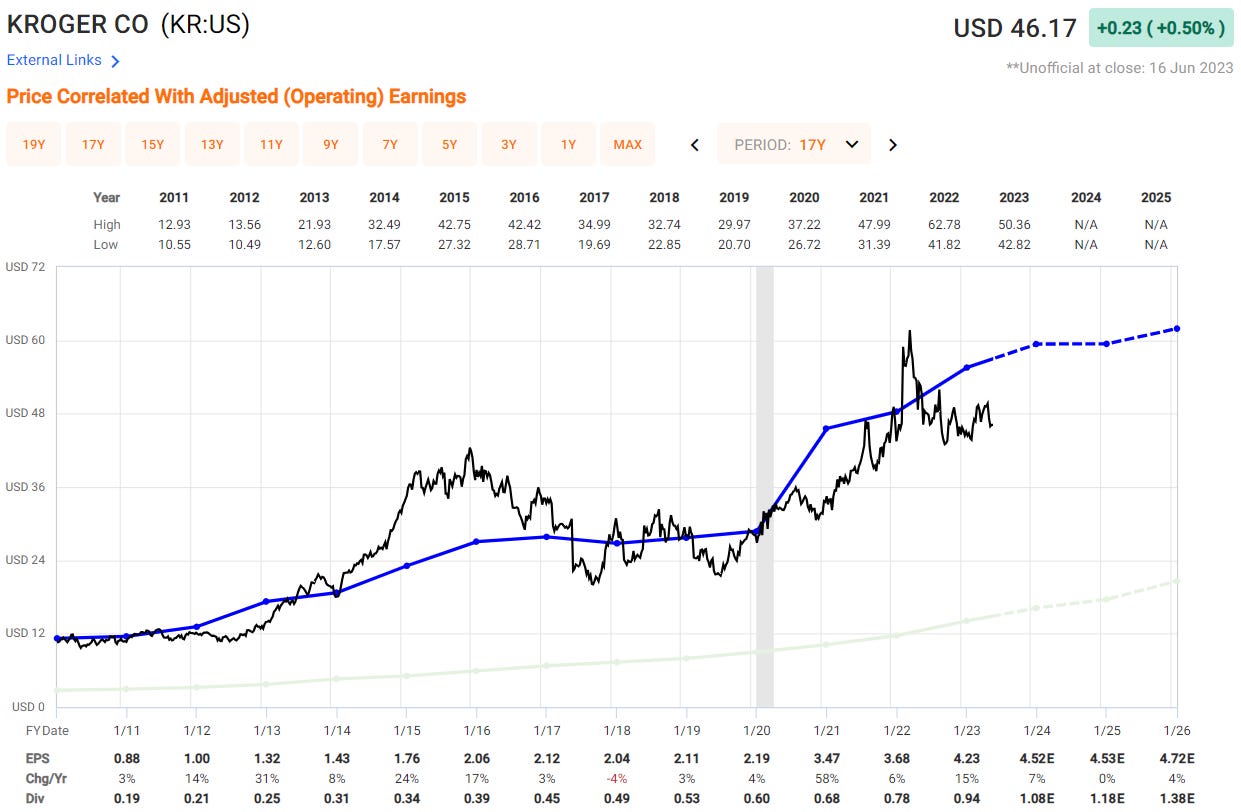

Kroger (KR)

Key Metrics

Revenue: $45.2 billion, an increase of +1% YoY

Operating Income: $1.5 billion, flat YoY

Profits: $962.0 million, an increase of +44% YoY

Earnings Release Callout

“Kroger's first quarter results demonstrate the durability of our business model in a more challenged operating environment. As more customers are feeling the effects of inflation and economic uncertainty, we are growing customer households by providing fresher products at affordable prices with personalized rewards.”

My Takeaway

Kroger remains a core position inside of my dividend growth portfolio, and despite a rare sight this quarter (in-line with expectations and NOT a beat and raise) they will remain.

Kroger highlighted an uptick in promotions during Q1 driven in large part by great consumer engagement with coupons and rewards. Kroger also saw -4% of disinflation during the quarter, a trend I expect to continue throughout the remainder of the year. Despite these good signs, investors seemed to be instead focused on management’s commentary re: their customers.

The current economic backdrop is significantly impacting more budget-conscious shoppers, especially those who have seen a reduction in SNAP benefits. Because of this (and a few other factors) management pointed to sales increase by only 2% throughout the back-half of 2023.

Another worry investors share is that as inflation begins to subside and disinflation begins to materialize over the next 6-9 months, volume will be the only driver of earnings power — as price increases will not make sense.

At time of writing, Kroger remains a position in my dividend growth portfolio — however, I’ll be watching this one carefully.

Oracle (ORCL)

Key Metrics

Revenue: $13.8 billion, an increase of +17% YoY

Operating Income: $4.1 billion, compared to $4.5 billion last year

Profits: $3.3 billion, an increase of +4% YoY

Earnings Release Callout

“Oracle's revenue reached an all-time high of $50 billion in FY23. Annual revenue growth was led by our cloud applications and infrastructure businesses which grew at a combined rate of 50% in constant currency. Our infrastructure growth rate has been accelerating—with 63% growth for the full year, and 77% growth in the fourth quarter.

Our cloud applications growth rate also accelerated in FY23. So, both of our two strategic cloud businesses are getting bigger—and growing faster. That bodes well for another strong year in FY24."

My Takeaway

Oracle reported solid quarterly results, with cloud revenue upside driving a top and bottom line beat for the company. I’m encouraged by the cloud revenue upside (+$370M more in revenue than expected) — but I’m even more encouraged by the company’s capital expenditures coming down by -$700M quarter-over-quarter.

With that being said, their remaining performance obligations decelerated to only +15% growth from +26% — I believe this is an indicator of slowing growth all around.

This sort of deceleration in growth reinforced the fact that cloud growth for Oracle is largely driven by database and application customers migrating from on premise to the cloud — and NOT net new customer workloads.

I don’t own Oracle, and I wouldn’t even consider opening a position at this valuation. The below shown chart explains this pretty clearly.

Investor Events / Global Affairs:

The IPO fun returns in a delicious way, Retail Sales remain buoyed by a heavy season of spending, and JPMorgan wants their name as far away from Jeffrey Epstein as possible.