Our sincerest thank you to all service members and veterans. To those reading that have lost a loved one defending our country — we are sharing our appreciation with you & yours, today & always.

Given this short week in the markets, the next Investing Week Ahead post will be delivered tomorrow.

Portfolio Updates:

No material changes have been made to the portfolio just yet. I shared the below post earlier last week. It detailed a few names I was excited about — so stay tuned to learn more.

With that being said, I’m thrilled to see my Broadcom (AVGO) position up +61% YTD — it’s so interesting to see “The Big Tech” trade be something that has taken over many portfolios in 2023.

Broadcom (AVGO) is part of my Dividend Growth Portfolio — and is carrying the performance of this portfolio YTD as Big Tech companies like Google, Nvidia, Apple, Amazon, Microsoft, and others rip higher.

With that being said, I think “Big Tech” is becoming a crowded trade — it’s time to focus on other (much smaller) technology companies such as the ones shared above.

I’m not at all saying I plan to exit my positions in my “Long Technology” subcategory, but instead that I plan to increase the weighting of my “Long Risky” subcategory in the coming months.

This subcategory is where I believe substantial alpha will be generated over the next 18-24 months as more and more “Big Tech” companies are stuck between a rock and a hard place, as I alluded to in this post re: Apple.

Week in Review — Too Long, Didn’t Read:

Nvidia reaches ridiculous valuations, but nobody truly knows if it’s overvalued yet, Palo Alto Networks continues to impress, the management team at Lowe’s is doing a quality job of controlling costs, Warren Buffett likes Capital One despite banking sector woes, Uber teams up with Alphabet’s Waymo, Meta receives a big fine from the EU and sells Giphy at a loss, Core PCE is ridiculously sticky, it’s becoming a coin flip whether the Fed will hike rates again in June, and high rates haven’t stopped New Home Sales as much as expected.

Key Earnings Announcements:

Nvidia soars, Palo Alto remains a favorite, and Lowe’s remains in my batch of stocks that I love to DCA into.

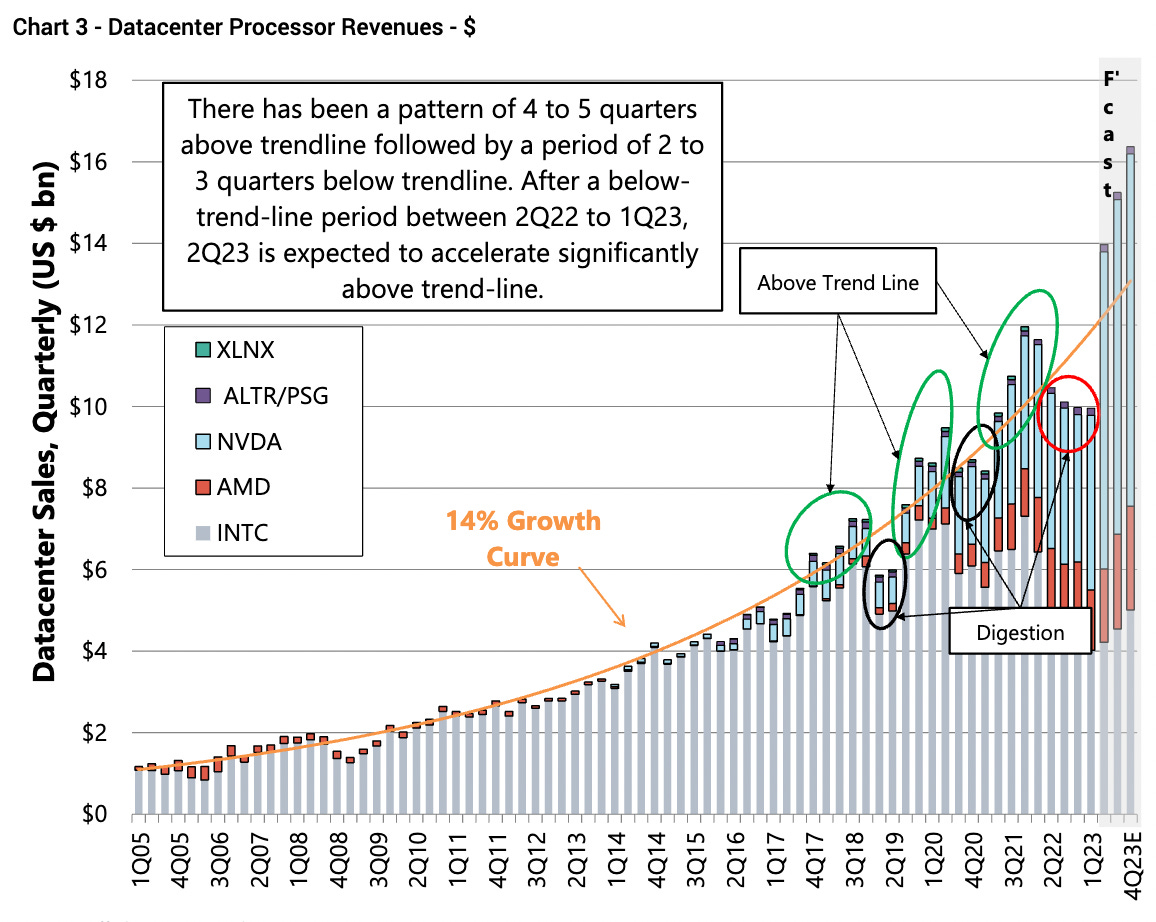

Nvidia (NVDA)

Key Metrics

Revenue: $7.2. billion, compared to $8.3 billion last year

Operating Income: $2.1 billion, an increase of +15% YoY

Profits: $2.0 billion, an increase of +26% YoY

Earnings Release Callout

“A trillion dollars of installed global data center infrastructure will transition from general purpose to accelerated computing as companies race to apply generative AI into every product, service and business process.

Our entire data center family of products — H100, Grace CPU, Grace Hopper Superchip, NVLink, Quantum 400 InfiniBand and BlueField-3 DPU — is in production. We are significantly increasing our supply to meet surging demand for them.”

My Takeaway

Unless you live under a rock, you’ve likely seen that NVDA blew their revenue expectations out of the water — causing the stock to skyrocket and hit all-time-highs. Personally, I didn’t see this coming.

Instead, I bet on ASML Holdings (ASML) — the company that makes the devices that chip companies like NVDA, AVGO, AMD, and others use to make their chips. I guess you could say I was betting on the manufacturer of the picks and shovels during the AI Gold Rush — thinking these folks would go back and purchase more picks and shovels over time.

ASML is up +40% YTD, while AVGO and NVDA are up much more than that.

Regardless, NVDA is now quickly approaching the $1 trillion market cap club — making it the 6th largest company in the S&P 500. But, at this new all-time-high, is the stock a “buy?”

Before I answer that question, check out this 2017 semiconductor report I found about the “4th Tectonic Shift” published by Jefferies predicting NVDA to become the biggest beneficiary.

Their newest report predicts NVDA taking 80% market share in data centers over the next 5 years — catalyzing $17 in EPS by 2026 (compared to NVDA’s $3.27 in 2023).

With that being said, it’s hard to say if NVDA is “over-valued” at the moment. For the best results, dollar cost average into the name over the long-term. That’s what I’ll begin doing in the coming weeks myself.

Palo Alto Networks (PANW)

Key Metrics

Revenue: $1.7 billion, an increase of +24% YoY

Operating Income: $78.7 million, compared to -$47.6 million last year

Profits: $107.8 million, compared to -$73.2 million last year

Earnings Release Callout

“We continued to demonstrate our commitment to profitable growth in Q3. As a result, we are raising our cash flow margin and operating margin guidance for FY'23 as we balance driving efficiency goals while investing for medium-term growth."

My Takeaway

As you all remember from this deep-dive post shared over a year ago now, I’ve been long-time bullish on cybersecurity. Specifically, Palo Alto Networks, Crowdstrike, and most recently SentinelOne.

Palo Alto Networks is up +52% YTD and remains a large position in my portfolio.

Annual recurring revenue (ARR) grew +60% YoY, outpacing expectations of just +56% — while free cash flow margins rose as well. While the microenvironment remains challenging, it’s obvious that PANW is gaining market share.

ARR will remain the most important metric to base PANW’s success against going forward, as it’s a precursor for free cash flow growth. As you can see in the results above, the company is finally operating in a profitable manner — this is largely due to the fact that 30% of the company’s revenue this quarter was software in nature, compared to only 10% of revenue just 3 years ago.

The company is trading around 20X forward free cash flow (EV/24FCF) which I believe is still attractively priced given their secular growth trend and opportunity to grow top line revenue by +20% YoY for the foreseeable future.

I’ll continue to dollar-cost average into an ever-expanding position. The below chart does a great job illustrating the future of this company in relation to its current stock price.