Before anyone tries to come for my head about the “definition” of a recession — I’m sorry, but the White House isn’t allowed to just change the long-standing accepted definition of what a recession is.

The CFA Institute (the most well-respected global association of investment professionals) defines a recession as two or more consecutive quarters of economic contraction — and for the purposes of this post I’m rolling with that.

Everyone is entitled to their own opinion (or definition), but I think we can all agree things have certainly been better.

What’s Been Going On?

I’m glad you asked.

Let’s take a step back to when we shared this post in late-June.

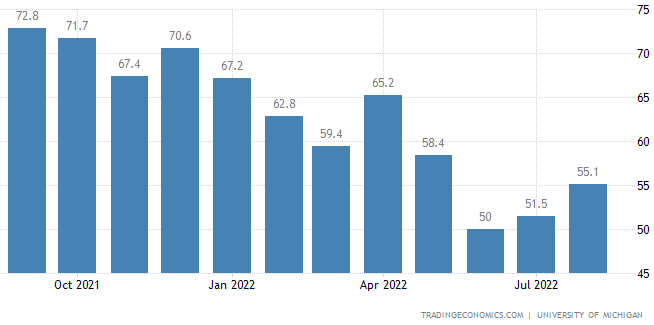

The markets were absolutely melting, inflation for the month of May was higher than expected (8.6%), the market was pricing in a +75 basis point hike from the Fed, consumer sentiment was at an all-time-low, and mortgage rates were sky-high.

University of Michigan’s Consumer Sentiment Index

But then something very important happened — Q2 earnings weren’t as bad as investors had originally feared, causing stock prices pop across the board.

— Then we received a flurry of positive data from credible sources

CEOs at major banks chimed in saying “Right now, everything is fine so we're investing into our business. Consumers are fine, businesses are fine, and jobs are plentiful.”

The NRF said a recession is unlikely in 2022 as the consumer outlook over the next few months seem favorable.

Amazon Prime Day broke records — showing continued strength in discretionary consumer spending.

Apple shared earnings results that confirmed consumers are still spending emphatically on iPhones and Apple devices, despite low broader sentiment.

Airbnb shared earnings results confirming their biggest quarter ever by gross bookings (revenue) — confirming travel demand remained high.

Disney shared earnings results confirming theme park attendance (and profitability) was back to pre-pandemic highs.

The good news above, paired with what seems to be cooling month-over-month inflation (8.5% vs. 9.1%), had the markets running hot! Not only were earnings better than feared, but the market was beginning to price in a pivot to a dovish stance from the Fed — which meant potential rate cuts in 2023.

In case you’re unaware, a dovish stance simply means the Fed is planning to cut rates and be more ‘accommodative’ — which would drive stock prices higher from trading multiples expanding.

So, What’s Happening Next?

We’re in the market for a crystal ball, let me know if you’re selling one.

Before I can answer that question, I think it’s important to understand what drove prices higher over the last several weeks. Sure, we had a flurry of positive news which seemed to push the markets up — but remember, hedge funds have been actively shorting (betting against) the market for weeks now.

Doing everything they can to profit on what seemed to be an impending move lower in late-June… but, we saw the opposite happen.

This caused near-record amounts of “short covering.”

TL;DR.. when you bet against a stock and you’re right — you make money. When you’re wrong, not only do you lose money — but you have to buy the stock back at whatever price it’s trading at. More about shorting stocks here.

This tells me that a lot of the buying we’ve experienced over the last several weeks came not just from investors, but hedge funds and other traders covering their short positions — causing the stock market to grind higher.

— Could this just be another bear market rally?

Perhaps — as not every BMR is the same in duration, return, and breadth.

Below is an awesome Tweet that illustrates the BMRs we’ve experienced in 2022 and compares them to 2002 and 2008.

Just so we’re all on the same page, after the Dot Com Bubble in 2000 — the Nasdaq rose +20% seven separate times (bear market rallies) before forming a true “bottom” after trading down -82% from its peak.

— Looking a few weeks ahead

Covered shorts, positive news regarding earnings, and no immediate negative catalysts over the coming weeks is a recipe for smooth sailing — until Jerome Powell takes the stage in Jackson Hole on 8/25.

If at the Jackson Hole Economic Symposium (8/25 — 8/27) Powell reaffirms plans of quantitative tightening — I’m not sure how well the markets will take it. Powell wants QT to be on autopilot, but as we explained here, the market’s liquidity has been poor.

How I’m Playing This

To summarize, the markets rallied on better than expected earnings, cooling inflation, and a handful of other catalysts. There seems to be no immediate catalysts for a market sell-off on the horizon — however, the Jackson Hole Economic Symposium in late-August could become that catalyst.

Folks are torn if we’re in a bear market rally or if we’ve truly turned the tide and we’re back in a full-blown bull market.

In my humble opinion, I don’t think the markets will turn “bull” until we’ve completely extinguished inflation.

Sure, seeing the numbers come down from 9.1% to 8.5% is decently good — but for us to head back to our historical ~2% the Fed is going to have to continue raising rates and keeping them there.

The “keeping them there” part is what’s scary.

I’ve been reading a lot about the 1970s and 1980s, specifically about inflation, the stock market, and interest rates.

Back then, the Fed raised rates quickly because of rising inflation (stock market crashed), then changed course prematurely thinking inflation was headed for the door — cutting rates quickly (causing the stock market to rally +35%).

Then once people realized the economy wasn’t growing, the markets dove again — making new lows only a few years later. The Fed had to begin tightening again to deal with inflation that seemed to have never went away — which sort of just turned into stagflation.

It caused the stock market to experience this volatile, kangaroo-type movement for several years. This was coined “The Lost Decade” for the US stock market.

This is exactly what I’m afraid of when the Fed says “soft landing.”

If inflation remains persistent around 4-5% in 2023 with random CPI spikes along the way, we’ll likely experience this kangaroo-like market — similar to the 1970s.

It’s imperative, in my opinion, for inflation to be completely under control and predictable before the market begins to make a true “bottom.”

Above are a few scenarios economists are assuming might happen depending on historical averages. Best case scenario, inflation is hovering around ~3% in Q1 of next year — worse case we’re at ~7% in Q1.

Regardless, it’s not where we need to be and until it’s truly under control it’s going to be hard to say when we’ve found a “bottom.”

— High Risk: Entering Stage 1

As I stated in this post a few months ago, I believe some of the most high-risk investments are nearing the end of their almost 2-year long bear market.