If you don’t like golf + beautiful scenes + $1.50 pimento cheese sandwiches — c’mon!

Two quick callouts before we dive in:

Eatin’ Cheap:

You thought the hot dogs at Costco were the only thing that was inflation-resistant? Make some room for the food menu at The Masters:

Stock Buybacks:

An incredible callout by Marlin Capital — Since 2000, US corporations have bought back $5.5T of stock. This has amounted to more demand than any other market participant, and it’s not even close.

We’re also well into a corporate buyback blackout period — which means the vast majority of the S&P 500 constituents are NOT allowed to buyback back their stock at the moment, leaving room for increased volatility to creep into the equation.

Portfolio Updates:

No major updates to share — everything is the same. With that being said, we’re experiencing a cryptocurrency correction at the moment — very common during bull markets.

I want to remind everyone that these corrections happen, and there’s much to be excited about over the coming 12-18 months. Use it as an opportunity to accumulate more before things really begin to heat up during Q3 and Q4 of this year.

Additionally, be weary. We’re looking at the highest VIX in over 9 months, the stock market is likely to open deep into the red tomorrow morning, and inflation is sticker than expected.

Have a plan, make a list of names you want to buy at a discount, and stay disciplined.

Week in Review — Too Long, Didn’t Read:

Beer is booming, BlackRock’s clients aren’t buying the stock market’s all-time-highs, JPMorgan is seeing an uptick in credit card delinquencies, Jamie Dimon’s warning signs, Google’s numerous reveals, Tesla’s taxi, the “second wave” of inflation MIGHT be coming, and a quick recap of the Fed’s Meeting Minutes.

Key Earnings Announcements:

Beer is booming, BlackRock’s clients aren’t buying the stock market’s all-time-highs, and JPMorgan is seeing an uptick in credit card delinquencies.

Constellation Brands (STZ)

Key Metrics

Revenue: $2.1 billion, an increase of +7% YoY

Operating Income: $629.0 million, an increase of +35% YoY

Profits: $392.0 million, an increase of +76% YoY

Earnings Release Callout

“Our enterprise results in Fiscal 24 exceeded our top-line growth outlook and delivered strong operating income growth.

We also generated strong operating cash flow, which enabled continued execution of our capital allocation priorities including: reducing our net leverage ratio from 3.6x to 3.2x, returning over $900 million to shareholders in dividends and share repurchases.”

My Takeaway

STZ handily beat their original guidance, issued forward guidance of +7% revenue growth and +10% EPS growth — higher than Wall Street was expecting. The company’s beer business is as strong as ever, while an improvement in wine & spirits remains a work in progress.

Wall Street is encouraged by their +7% revenue growth guidance — stating “This volume-led top-line should easily translate into +10-12% operating profit as the company drives efficiencies in markets and leverage on operating expenses.”

If you’re looking to add a recession-resistant stock to your portfolio (alcohol), Constellation Brands seems to be fairly priced at the moment. I’ll consider doing the same — as I add STZ to my watchlist, looking to buy on weakness.

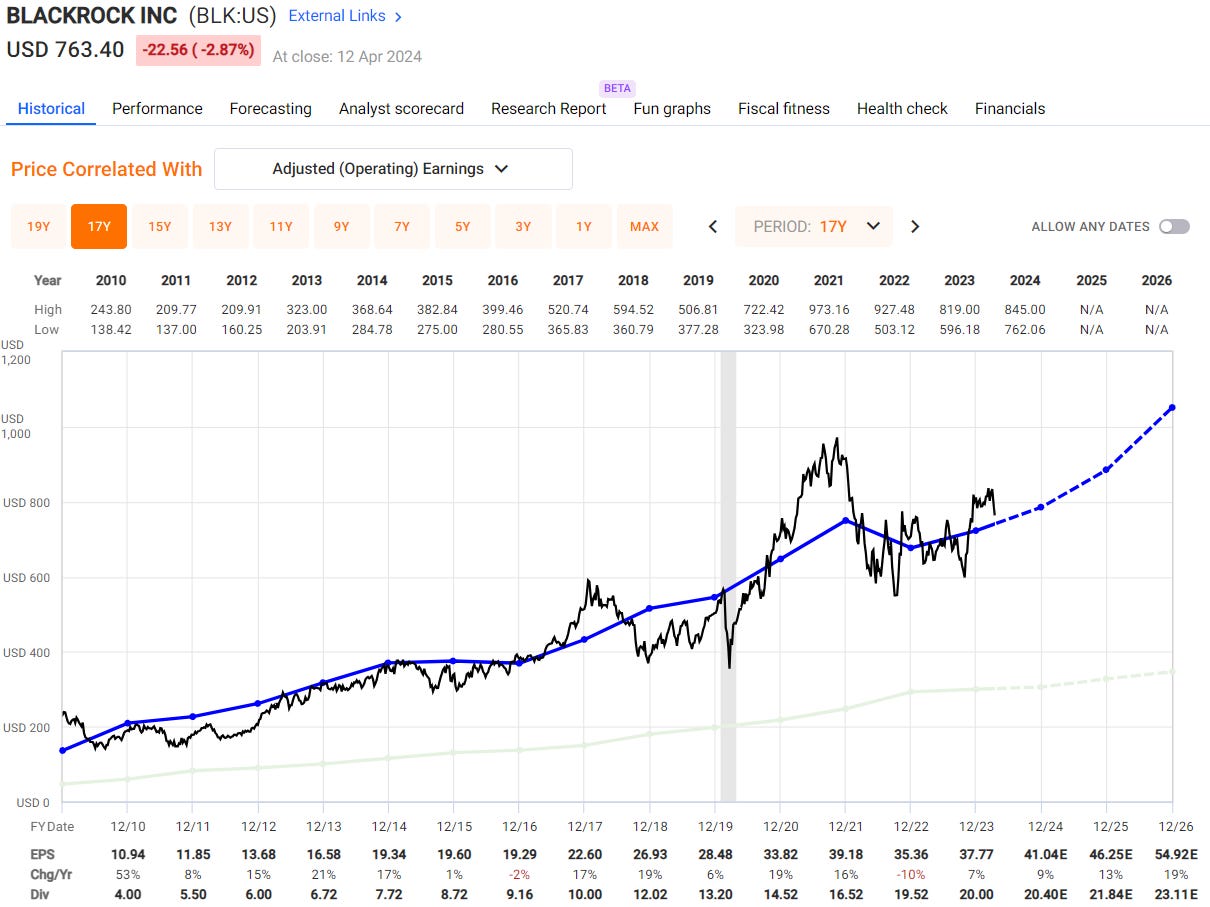

BlackRock (BLK)

Key Metrics

Revenue: $4.7 billion, an increase of +11% YoY

Operating Income: $1.7 billion, an increase of +18% YoY

Profits: $1.6 billion, an increase of +36% YoY

Earnings Release Callout

“BlackRock’s momentum continues to build, with accelerating client activity and line of sight into the funding of significant wealth, institutional, and Aladdin mandates. Organic asset and base fee growth accelerated into the end of the quarter, and first quarter long-term net inflows of $76 billion already represent nearly 40% of full year 2023 levels.”

My Takeaway

Q1 earnings results were mixed — on the positive side… cost control was fantastic, as their adj. operating margin rose to 42.2%. Their performance fees were also strong, at $204M vs. Wall Street’s $116M expectation. On the other side of the aisle, base management fees of $3.77B were below Wall Street’s $3.83B expectations on a slightly lower fee rate of 14.9bps.

Net inflows were broadly below forecasts, at $76B vs. $84B expected. BlackRock seems to be having trouble sustaining their 5% inflow growth rate of the last few quarters — with management stating their high conviction that organic base fee growth can improve.

A few areas to monitor moving forward — base management fee rate (need this to remain above 15bps), client reallocation (only saw $76B during the quarter, but could have been $100B if existing clients didn’t already have so much invested into equities i.e. the stock market is at all-time-highs), and fixed income flows (the yield curve is inverted).

BlackRock is a blue chip stock if you ask me — however, their valuation at the moment is on the frothier side. If you want to open a position, wait for things to cool down a bit.

JPMorgan Chase (JPM)

Key Metrics

Revenue: $41.9 billion, an increase of +9% YoY

Profits: $13.4 billion, an increase of +6% YoY

Earnings Release Callout

“Many economic indicators continue to be favorable. However, looking ahead, we remain alert to a number of significant uncertain forces. First, the global landscape is unsettling – terrible wars and violence continue to cause suffering, and geopolitical tensions are growing.

Second, there seems to be a large number of persistent inflationary pressures, which may likely continue. And finally, we have never truly experienced the full effect of quantitative tightening on this scale. We do not know how these factors will play out, but we must prepare the Firm for a wide range of potential environments to ensure that we can consistently be there for clients.”

My Takeaway

ROTCE was a strong 21%, earning per share rose by +8%, and tangible book per share was up +3% since the start of the year, and +15% over the last 12-months. Besides the FDIC hit of $725M, there were $366M of securities losses, and about $100M of hedge losses — which were partially offset by $72M of legal cost reversals and another $72M of loan loss reserve release.

Management reiterated the view that normalization of both net interest income and credit is expected to continue. Consumer credit / debit card sales volume rose a strong +9% YoY — however card losses rose to 3.32% from 2.79% last quarter.

As you all know, I don’t invest into bank stocks — with that being said, JPM seems to be historically undervalued at the moment.

Investor Events / Global Affairs:

Jamie Dimon’s warning signs, Google’s numerous reveals, and Tesla’s taxi.