Unfortunately, even if inflation really did peak in June — the Consumer Price Index (CPI) wouldn’t reach the Fed’s 2% target any time soon. We’re not saying that you should sit on the sidelines, but it’s critical to remind you that this is likely to remain a stock-picker’s market and there’s probably going to be broader downside after this bear market rally concludes.

The markets have since traded down —9%.

We usually don’t think it’s fair to make such a blanket statement and say “don’t invest at all” — but as explained in this post, have continued to exercise caution.

Regardless of market conditions, there’s always a play to be found. However, we sure are glad to be mostly in cash right now. We believe better buying opportunities for indices and most stocks are yet to come.

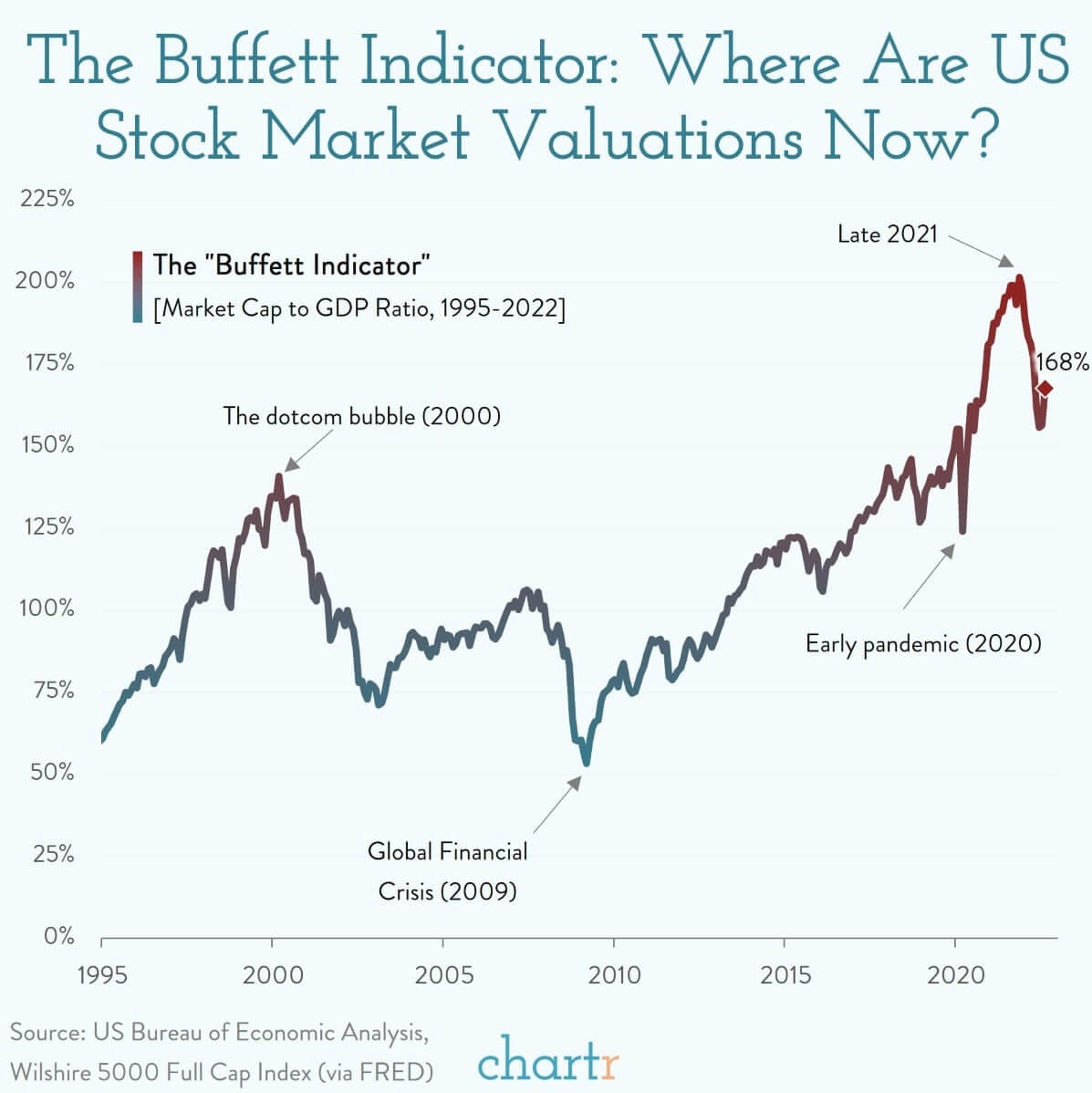

The simple ratio takes the value of the stock market vs. the annualized GDP of the US. At time of writing, this value is at 173%.

“On its own that number doesn't mean much, but when placed in historical context it's striking. Even after the recent fallin markets the ratio is still one of thehighest on record, north of the ~140% recorded during the Dotcom bubble of 2000, and considerably elevated compared to the average since 1995 (109%).” — Chartr

More downside is likely, and we’re pumped to get more fairly valued shares of companies that we believe in for the long-term.

Week in Review — Too Long, Didn’t Read:

Cybersecurity remains a great bet, Lululemon is firing on all cylinders, Broadcom’s business is incredibly diversified, the Nord Stream pipelines from Russia have indefinitely suspended gas to Germany (and Europe), Taiwan shot down a drone in their airspace, Twitter’s bot situation just got worse, Snap is laying off -20% of their staff, and the jobs report came in as expected.

Key Earnings Announcements:

SentinelOne exceeded expectations across the board, Crowdstrike remains an incredibly attractive bet on the longevity of cybersecurity, Lululemon is outpacing Nike from a DTC perspective, and Broadcom is officially one of my new favorite stocks.

SentinelOne (S)

Key Metrics

Revenue: $102.5 million, an increase of +124% YoY

Operating Loss: -$108.2 million, compared to -$67.2 million last year

Net Loss: -$96.3 million, compared to -$69.0 million last year

Earnings Release Callout

“We delivered hyper growth and outperformance across all aspects of our business in Q2 - ARR, revenue, customer growth, net retention, and margins. Our business momentum remains extremely strong. We once again delivered a combination of triple-digit growth while steadily moving towards long term profitability. ARR growth accelerated to 122% and non-GAAP operating margins expanded 42 percentage points year-over-year.”

My Takeaway

About nine months ago I shared an update on the company — stating I was bullish, but not yet a buyer. Now that the stock has traded down -40% to $25 / share (10X 2023 revenue), they look much more attractive. I’ll absolutely be adding this to my “cybersecurity” basket of stocks.

Regarding the quarterly earnings — few major callouts that point to long-term momentum with the company.

First, dollar-based retention rates hit a record high of 137% during the quarter, pointing to SentinelOne’s ability to cross-sell and up-sell existing customers.

Second, they beat expectations across the board — revenue came in +7% higher, operating margins came in +17% higher, and they added +$15M more in net new ARR than expected.

Finally, they raised their revenue guidance for the year by +$11M to $416M — which included some conservatism given the macroeconomy right now. I’m so excited to see these results and begin building a starter position (2%) in this company.

CrowdStrike (CRWD)

Key Metrics

Revenue: $535.2 million, an increase of +58%

Operating Loss: -$48.3 million, compared to -$47.4 million

Net Loss: -$48.3 million, compared to -$57.3 million

Earnings Release Callout

“Ending ARR surpassed the $2 billion milestone, net new ARR reached a record $218 million and net new subscription customers reached a record 1,741 in the quarter. CrowdStrike delivered robust growth at scale and exceptional unit economics with over 80% year-over-year growth in operating and free cash flow. We are raising our guidance for fiscal year 2023, which reflects our technology advantage and strong industry tailwinds combined with a pragmatic view of current macroeconomic conditions.”

My Takeaway

Another cybersecurity winner!

Incredible quarter by the company — revenue beat expectations and grew +58% to $535M, while subscription revenue trended in the right direction to now accounting for 95% of total revenue. Gross margins were a bit lower than hoped for, but CRWD made up for it with their operating margins. The company reported 16.3% vs. 14.1% as expected — nice!

Another awesome callout by their management team was their guidance — raised it above the street’s expectations for the next quarter stating less seasonality during the second half of the year as the catalyst.

All in all, Crowdstrike remains an awesome cybersecurity winner in our books. They’ll continue to gain market share, cross-sell / up-sell to their clients, and help enterprises consolidate multiple products into one.

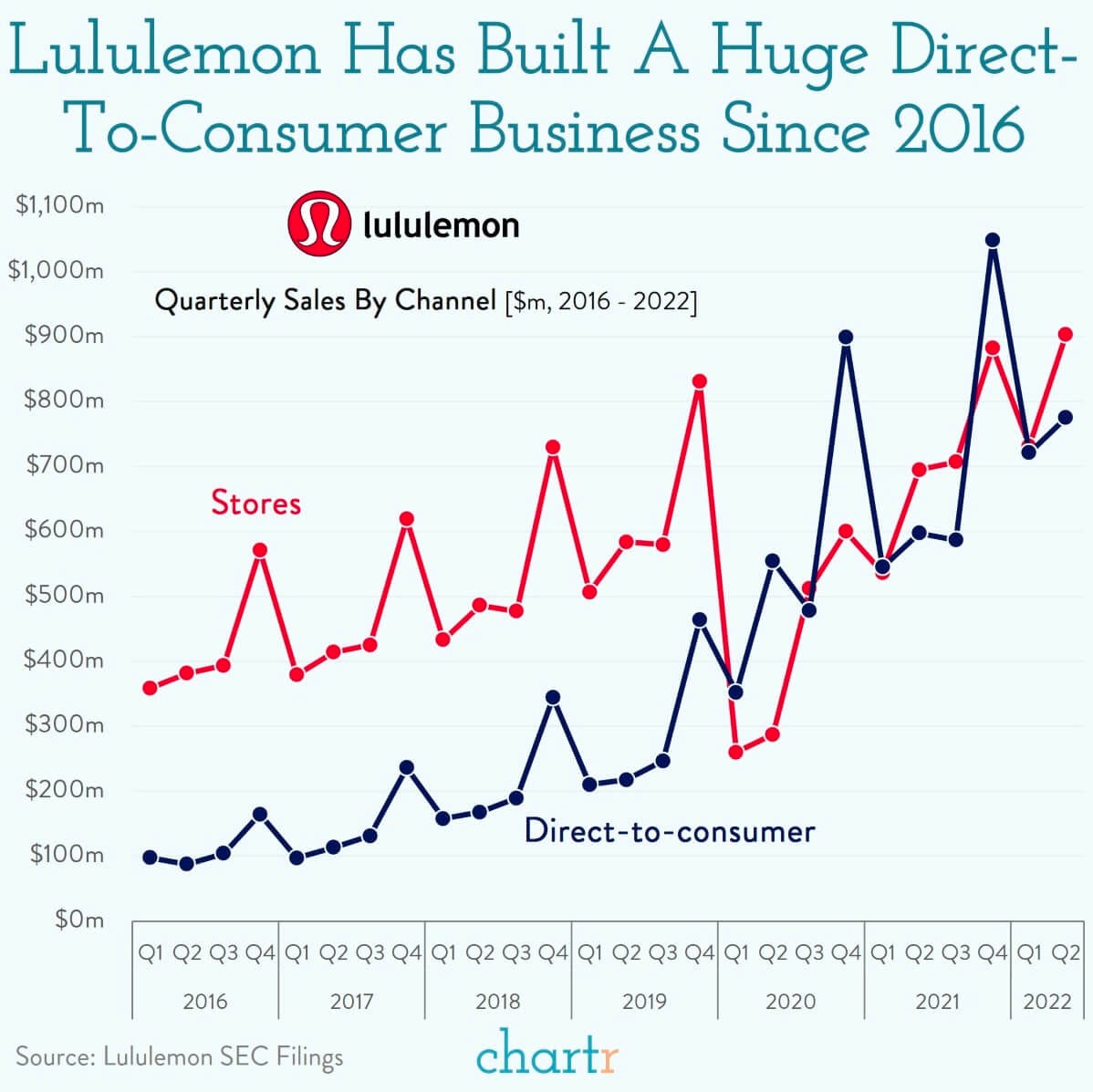

Lululemon (LULU)

Key Metrics

Revenue: $1.9 billion, an increase of +29% YoY

Operating Income: $401.2 million, an increase of +38% YoY

Profits: $289.5 million, an increase of +39% YoY

Earnings Release Callout

“The momentum in our business continued in the second quarter, fueled by strong guest response to our product innovations, community activations, and omni experience. As we look ahead, we're excited about our ability to successfully deliver against our Power of Three ×2 growth plan and create ongoing value for all our stakeholders.”

My Takeaway

First, major shoutout to our friend Chris Camillo for being completely correct on this company as they headed into their earnings release. Wall Street wasn’t excited and counted them out — but Chris took the other side of the trade.

Lululemon reported an awesome quarter — accelerating sales growth balanced between store sales and direct-to-consumer sales (shown below), while navigating macroeconomic slowdowns and uncertainty. Another notable callout by their management team was their improved gross profit margins due to supply chain relief — this relief has allowed the company to pull forward some distribution center investments while still netting better leverage than expected.

New customer growth also accelerated during the quarter — sales gains were balanced between men and women, and by geography. Solid quarter by LULU!