Wishing each of you a restful remainder to your weekend.

Below is something interesting to kick us off. It’s how the economy reacts to interest rates — of which we’ve had the most aggressive raises in decades.

HOPE = Housing, Orders, Profits, and Employment.

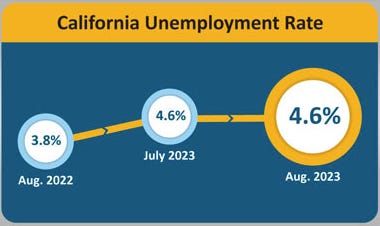

The reason we share this is because the Employment part of the equation could be very relevant, very soon. The U.S. unemployment rate unexpectedly rose to 3.8% in August — up from 3.5% in July and the highest since February 2022. Most analysts were expecting 3.4%-3.5%.

A more encompassing unemployment measure that counts discouraged workers as well as those working part-time for economic reasons jumped to 7.1%, a +0.4 percentage point increase and the highest since May 2022.

California’s unemployment rate is also an interesting stat to take note of. For many broader economic trends — California has been used as a good bellwether for where the country is heading.

At a time when we want as many people working as possible — companies like Chipotle Mexican Grill (CMG), Chick-fil-A, Yum! Brands (YUM), and Restaurant Brands International (QSR) have opposed this type of drastic raises. The reason? They won’t be able to employ more people when it’s that expensive for their franchises.

We’ll be sure to serve up continual updates on the ever-changing job market!

Portfolio Updates:

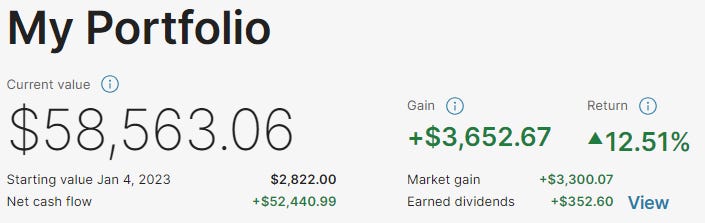

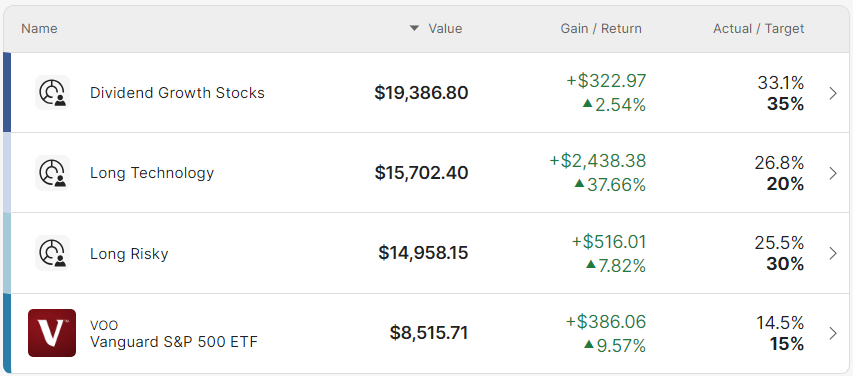

September has shaped up one of the softer months in 2023, with both the S&P 500 and the Nasdaq down -2%. The portfolio, however, seems to be holding up pretty well.

As shown above, the Dividend Growth Portfolio has outperformed the dollar cost averaged S&P 500 year-to-date by roughly +3%. Over the coming weeks I’m going to begin to cut out some of the losers and deploy that capital back into some of the biggest winners.

Just so we’re all on the same page right now, names I’m excited about for Q4 include:

Broadcom (AVGO)

Crowdstrike (CRWD)

Salesforce (CRM)

Amazon (AMZN)

Google (GOOGL)

Shopify (SHOP)

Uber (UBER)

William Sonoma (WSM)

Covered Call Update

I also really want to encourage you all to consider learning more about covered calls. Specifically, selling them against your existing holdings to generate income.

On Monday, I deposited $26,275 into my Robinhood account to purchase 100 shares of Tesla stock. I paid $262.75 each for them. I chose Tesla because I’m a long-term believer in both their management team and their products (Morgan Stanley just predicted an additional $500B in market capitalization could come from their Dojo product).

I’ll happily own their stock for years to come!

Immediately after purchasing my 100 shares, I sold a covered call option contract against those 100 shares with a strike price of $270 and an expiration date of October 20th. I was instantly paid $1,575 in cash to my brokerage account (now in my checking account) — a now guaranteed 6% return on my $26,275 investment.

Over the next 5 weeks (time between now and October 20th), we’ll see where Tesla shares are trading.

If they’re trading above ~$285 per share (high enough for someone to want to exercise their option contract considering they paid ~$15 per share in premium) — I’ll be forced to sell my 100 shares of Tesla for $270 each.

$270 – $262.75 = $7.25 profit per share x 100 shares = $725 profit.

Add my upfront +$1,575 to this $725 and I could realize a $2,300 total profit on my $26,275 investment in just 5 weeks time — an 8.8% return! I’d be very happy.

But what’s the downside?

Let’s pretend my shares of Tesla stock don’t trade up to that ~$285 / share range shared above — instead, they trade down to $250 / share for example.

Well, that’s fine.

I’m a long-term believer in Tesla, and will happily own their stock for years to come no matter how high or how low it trades. Since it wouldn’t have traded high enough for someone to want to exercise their contract, the only profit I will have made is the $1,575 of cash premium paid to me when I sold the contract — a 6% return in 5 weeks.

Once the calendar rolls over to October 21st, I’ll sell another covered call option contract worth roughly $1,500 and the 5-week waiting game happens all over again.

As you can see, by simply owning 100 shares of Tesla stock — I’m able to consistently generate >$1,500 in passive income every 5 weeks or so.

I plan to use this extra cash to supplement my lifestyle, while other investors use the cash to buy more shares of the stocks they love. It’s entirely your preference!

I had a ton of you all get really excited about learning more about this income-generating strategy.

I’ll write an entire post dedicated to covered calls over the coming week — I’ll also include other stock ideas that don’t require a $26K initial investment.

For example, DraftKings (DKNG) could be a great name to experiment with at only $31 / share right now + free cash flow tailwinds into 2025.

More to come!

Week in Review — Too Long, Didn’t Read:

Adobe’s generative AI products created 5 billion images, Oracle reiterated their 2026 revenue projections of $65 billion, Apple’s ‘Wonderlust’ event gave plenty of new updates (most of which aren’t very exciting though), Citigroup layoffs are coming, More Google layoffs are already here, Delta Air Lines pissed off their biggest fans, and inflation metrics indicate that we “aren’t out of the woods” yet.

Key Earnings Announcements:

Adobe’s generative AI products created 5 billion images, and Oracle reiterated their 2026 revenue projections of $65 billion.

Adobe (ADBE)

Key Metrics

Revenue: $4.9 billion, an increase of +10% YoY

Operating Income: $1.7 billion, an increase of +14% YoY

Profits: $1.4 billion, an increase of +24% YoY

Earnings Release Callout

“We are unleashing a new era of AI-enhanced creativity around the world with innovations across our product portfolio. Adobe delivered world-class margins and earnings in Q3, while making significant investments in our technology platforms.”

My Takeaway

This quarter just solidified my conviction that Adobe is going to be a long-term winner in an emerging generative AI world. Adobe is aggressively pricing their AI-specific products for adoption and retention, with long-term profits taking the backseat at the moment. I believe this is the best way to play the secular growth trend and position yourself for long-term competitive success.

Outside of AI-specific revenue, results were led by strong net new Digital Media ARR ($464M vs. $410M expected) driven by better Creative ARR and solid Document Cloud ARR.

What Had Me Excited:

Revenue beating expectations by +13%.

Management shared that over 5 billion images were created using their generative AI tools, showing a clear demand for the products.

Operating margin came in about 1% higher than historical quarters.

Adobe repurchased 2.1 million shares during the quarter.

I’ll remain a shareholder in this company for a longtime. Below is an image of the company’s stock price in black in relation to their operating cash flow in blue. Generally speaking, these two figures move together — as operating cash flow increases, so does their stock price.

It’s obvious where their operating cash flow is headed over the coming years.

Oracle (ORCL)

Key Metrics

Revenue: $12.5 billion, an increase of +9% YoY

Operating Income: $3.3 billion, an increase of +26% YoY

Profits: $2.4 billion, an increase of +56% YoY

Earnings Release Callout

“As of today, AI development companies have signed contracts to purchase more than $4 billion of capacity in Oracle's Gen2 Cloud.

That's twice as much as we had booked at the end of Q4. The largest AI technology companies and the leading AI startups continue to expand their business with Oracle for one simple reason—Oracle's RDMA interconnected NVIDIA Superclusters train AI models at twice the speed and less than half the cost of other clouds.”

My Takeaway

The quarter was largely consistent with expectations. Revenue hit the midpoint of their guidance with better than expected operating margins — however, they missed expectations on their high-margin Licenses due to Cerner’s migration toward Cloud subscriptions.

Excitingly, AI-related Cloud bookings doubled quarter-over-quarter to $4 billion as management continues to work toward supplying enough GPUs to catch up to the strong demand they’re experiencing.

I’m optimistic about Oracle’s AI story — something that should drive accelerating revenue growth and margin expansion through 2026.

What Had Me Excited:

Total revenue hit their guidance expectations.

Excluding Cerner, their Cloud revenue grew by +29% — however, supply remains a headwind (GPUs).

Their forward guidance implies two straight quarters now of operating margin expansion — and their third straight quarter of operating income growth.

Their 2026 revenue target of $65 billion was reiterated.

I’m not a shareholder, but I might become one in 2024. I like what I see with AI, but their supply constraints worry me. I’ll keep you all in the loop!

Investor Events / Global Affairs:

Apple’s big event, Citigroup and Google tighten up their organizations, and Delta infuriates its most loyal customers.

Apple (AAPL) Event Recap

Apple announced the iPhone 15 and iPhone 15 Plus — which will have USB-C charging ports — starting at $799. Tim Cook & Co. also unveiled the iPhone 15 Pro and Pro Max — starting at $999.

Another key announcement was the brand-new Apple Watch — made with 95% titanium and an impressive 72 hour battery life, as well as updated AirPods.