👉 Week in Review: 9/10/23

👉 Week in Review: 9/10/23

All eyes on Apple's $74 billion Chinese market...

We hope you had a great weekend.

Do you love Twitter (X)?

We’d really appreciate it if you gave us a ‘follow’ on the new account linked here!

Substack will remain the home base for all of the best economic and financial content around, but Twitter will allow us to share snippets from our research!

Please do us a favor and sign give us a quick follow! Thank you in advance!

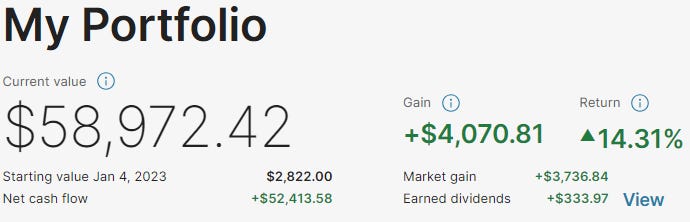

Portfolio Updates:

I have some very exciting news to share as it relates to the $2M Dividend Growth Portfolio! As you all know, for the last 9+ months I’ve been deploying capital across a few different brokerage accounts in efforts to publicly build a $2M portfolio from scratch.

Capital deployed during the Summer was mainly into Cryptocurrency — as that now makes up roughly $45K in value (1.5 BTC and 7 ETH). However, I was diligent to also invest straight into the M1 Finance portfolio as detailed in our Portfolio Tracker (paying subscribers-only).

With September’s capital allocation (roughly $28,000), I’m going to try something new in efforts to generate monthly passive income. I’m going to begin writing covered calls.

What is a Covered Call?

It’s pretty simple. As you all might already know, investors use option contracts to trade with leverage — 100X to be precise.

For example, someone might spend $1,000 to purchase a call option contract giving them the right to buy Tesla stock at $260 (strike price) per share by October 13 (expiration). If Tesla stock is trading at $300 per share on or before October 13, and this trader has the right to purchase 100 shares for $260 — then they’re going to make a big profit ($4,000) from flipping their Tesla shares back onto the market!

This hypothetical trader spent $1,000 to make a $4,000 profit — netting them $3,000 in total.

So, what am I doing? I’m selling them that call option contract and collecting that $1,000 in “passive income.” By owning the 100 shares of Tesla and giving someone that right to buy them from me for a higher price than I bought them for, I’m not only making a profit on my 100 shares — but I’m also collecting a cash “premium” of $1,000 in the process.

Here’s the math:

Austin buys 100 shares of Tesla for $250 each — which is $25,000 out of pocket.

Austin then sells a “covered call” against his 100 shares with a strike price of $260 and expiration date of October 13 — collecting $1,000 in cash upfront from whomever purchased it from me.

If the purchaser wants to “exercise” their contract, Austin is forced to sell his 100 shares of Tesla to them for a $10 per share profit ($1,000) on top of the $1,000 in cash I received upfront — netting Austin up to $2,000 in total profit on a $25,000 investment.

$2,000 in potential profit on a $25,000 investment is an 8% return in only 1 month. If the purchaser chooses not to exercise their right to buy the 100 shares, then I keep them while also generating $1,000 in “passive income” during the month — 4%.

$1,000 per month in passive income per 100 shares of Tesla — a company I believe in for the long-term. I’m very excited to begin testing this new passive income generating strategy with you all!

I’ve deposited $26K (extra in case Tesla trades higher in the near future) into my Robinhood account (easiest for covered calls) and I plan to buy my share + sell my covered call against them on Tuesday once the funds clear.

I’ll report back next Sunday and share my experience! If this passive income strategy is something you all want to learn more about, let me know by replying to this email or leaving a comment below.

Week in Review — Too Long, Didn’t Read:

Kroger could be in a tough position, Z-Scaler deserves a deeper look, Asana’s profitability quest, Apple’s relationship with China is rocky, Tesla forms an interesting partnership with Hilton, Saudi Arabia’s treasury holdings are worth noting, Fed officials are becoming more apprehensive toward raising rates, and a quick update on the U.S. job market.

Key Earnings Announcements:

Kroger braces for a rough second-half of 2023, Z-scaler surpasses $2B in ARR, and Asana inches closer to profitability.

Kroger (KR)

Key Metrics

Revenue: $33.8 billion, compared to $34.6 billion last year

Operating Loss: -$479.0 million, compared to $954.0 million last year

Net Loss: -$180.0 million, compared to $731.0 million last year

Earnings Release Callout

“Looking forward, we believe inflation will continue to decelerate and the environment will remain challenging for consumers. We therefore expect identical sales without fuel will be at the low end of our full-year guidance range and slightly negative in the second half of the year.”

My Takeaway

Kroger announced their divesture of 413 stores to C&S Wholesalers for $1.9 billion — allowing them to move forward with the Albertson’s merger in the eyes of the FTC. C&S Wholesalers may also purchase an additional 237 stores for additional cash if needed to ensure the Albertson’s merger goes through.

With that being said, Kroger’s Q2 numbers were a bit lighter than expected — both on revenue and profits. They also called for a challenging rest of the year, something I'm not particularly excited to hear. Management also mentioned elevated SNAP benefits rolling off earlier this year, resumption of student loan payments in October, as well as prices +25% higher today than they were two years ago — volumes are likely to continue to consolidate.

Kroger has been a long-time growth compounder, especially in relation to their dividend — but they seem to be stuck between a rock and a hard place. I’m going to continue following this one closely.

Z-Scaler (ZS)

Key Metrics

Revenue: $455.0 million, an increase of +43% YoY

Operating Loss: -$44.5 million, compared to -$82.5 million last year

Net Loss: -$30.7 million, compared to -$97.6 million last year

Earnings Release Callout

“We concluded our fiscal year with strong top line growth and record operating profits.

In less than two years, we doubled our annual recurring revenue, surpassing the $2 billion milestone. With cyber security as a high priority, IT executives are modernizing their legacy network security with our zero-trust architecture.”

My Takeaway

This is a really interesting company! I had them on my broad “cybersecurity” watchlist last year, but they’re definitely on my radar now that they’re running at $2B in annual recurring revenue.

They company beat Wall Street’s estimates catalyzed by broad-based demand, solid execution, and improvements in operating leverage. They also saw increased adoption in their new products — accounting for 18% of net new ARR. Their competition remains intense, as cybersecurity is a massive secular growth trend everyone wants a piece of.

With that being said, I’m impressed they’ve continued to see success in selling their broader tech stack to large enterprises. Looking ahead, I’d except ZS to continue to ramp up their sales hiring to continue taking advantage of the large market staring them in the face.

I’m going to begin researching Z-Scaler more — I’m loving their operating leverage story and think it could be a major catalyst for stock price appreciation in 2024 / 2025. More to come!

Asana (ASAN)