Last week we briefly touched on the housing affordability index — specifically the fact that it’s at multi-decade lows. Before we jump into this week’s review, we want to spell out for you exactly what this means as well as offer a trade idea.

There are three factors at play in the housing market right now:

Interest Rates

Housing Inventory

New Construction Home Builds

As we all know, interest rates on 30-year mortgages are hitting multi-decade highs — now coming in around 8%. The higher the interest rate, the higher the monthly mortgage payment.

At time of writing this, the median cost to buy a house hit a new all-time-high of $2,748 / month — up a massive +90% since 2020. To put that number in perspective, that’s nearly $33,000 per year to own a home — making up 46% of the median pre-tax household income in the US.

Next on the list of factors impacting housing affordability is the inventory of single-family homes — which at the moment is hovering around 950,000.

There were 3.5 million single family homes for sale in 2008 — and roughly 3.0 million in 1987. And despite this massive drop in inventory over the last few decades, the US population has increased by +40%.

Think about it like this — because interest rates are high, it’s more expensive to own a home. If someone out there (like myself) has a mortgage with an interest rate of 3% — why would I want to sell that house right now?

There’s no reason for me (or anyone, generally speaking) to trade a 3% interest rate for an 8% interest rate.

Multiply this ideology by millions of home owners around the country and you get the graph above — people staying put in their homes because the alternative is a much higher monthly payment.

People aren’t selling their homes.

So if people aren’t selling their homes, how do we add supply to the markets?

Home builders — there are several companies out there trying their best to build reasonably-priced new homes for the everyday Americans to purchase and live in.

If we rewind to 2019, I was one of those everyday Americans. I purchased my Nashville house new for $280K at 3%.

However, the problem is these home builders started building 9-18 months ago when interest rates were 4%. Now, interest rates are 8% plus — pricing a lot of “everyday Americans” out of what was supposed to be affordable housing.

So now the housing market is essentially the image above — existing home sales are plummeting because the average homeowner’s interest rate is 3.6%, trapping them in their house.

New construction is more expensive than hoped for, but remains the only alternative for new market entrants as existing homeowners stay put in their 3.6% interest mortgages.

And the icing on top? Zillow is offering mortgages for 1% down in efforts to open homeownership to more borrowers.

This isn’t uncommon, however, as more and more home builders are offering a similar "deal” to anyone that will purchase a home from them. They’re sitting on thousands, if not tens of thousands, of newly built homes they can’t sell because the everyday American can’t afford 8% interest rates.

So the home builders are using their own money to buy down the interest rates for their customers — eating into their profit margins. It’s that or sit on a bunch of empty houses as your shareholders get more and more upset.

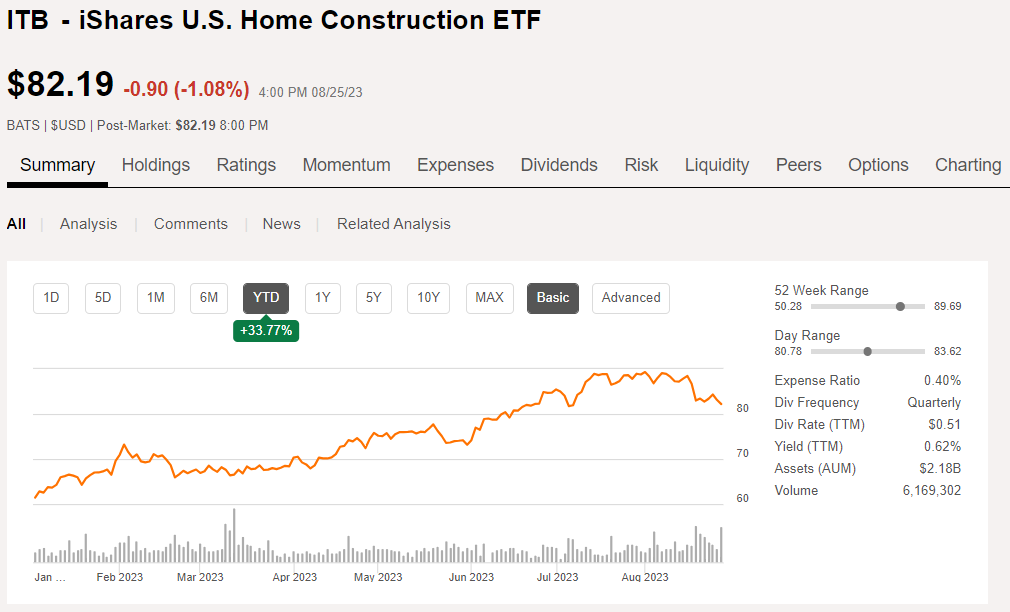

Trade Idea: short the home-builders, specifically the ETF “ITB”.

If you want to dig around its holdings and find a home builder who’s really poised to suffer from this, feel free. But be sure to share it with me!

Portfolio Updates:

Throughout the month of August I’ve deployed roughly $32,000 toward the dividend growth portfolio — however, a solid chunk of that went toward cryptocurrency as we saw a mild drawdown over the last several days.

As you all might know, Napco Security Technologies (NSSC) restated their quarterly financial statements year-to-date, causing their stock price to collapse by -45%. Unfortunately, Napco was a name I shared with you all earlier this year — causing a ton of you to have also been caught up in this mess.

With that being said, I’ve not exited my position — and I don’t plan to.

The company, in my humble opinion, is operating within a secular growth trends of “security,” something I’m confident will continue to see an uptick in demand as more and more unwarranted security breaches across schools, hospitals, and newly built commercial residential buildings take place.

According to this Twitter user, the current price of Bitcoin ($26K) is roughly around the cycle “bottom,” alluding to limited downside over the coming months. However, we all know with cryptocurrency “limited downside” might be another -20%.

Week in Review — Too Long, Didn’t Read:

Nvidia blew expectations out of the water, Lowe’s valuation multiple is closing in on Home Depot’s, Snowflake is sitting between the largest secular growth trends of the decade, 3M is set to pay $5.5B in damages, Marathon shut down the 3rd largest refinery in the US, Jerome Powell reaffirmed “higher for longer,” and both the Global Manufacturing and Services PMIs contracted.

Key Earnings Announcements:

Nvidia blew expectations out of the water, Lowe’s valuation multiple is closing in on Home Depot’s, and Snowflake is sitting between the largest secular growth trends of the decade.

Nvidia (NVDA)

Key Metrics

Revenue: $13.5 billion, an increase of +101% YoY

Operating Income: $6.8 billion, an increase of +843% YoY

Profits: $6.2 billion, an increase of +854% YoY

Earnings Release Callout

“A new computing era has begun. Companies worldwide are transitioning from general-purpose to accelerated computing and generative AI.

During the quarter, major cloud service providers announced massive NVIDIA H100 AI infrastructures. Leading enterprise IT system and software providers announced partnerships to bring NVIDIA AI to every industry. The race is on to adopt generative AI.”

My Takeaway

NVDA posted a very strong second quarter with revenue beating expectations by +21% and profits beating expectations by +30%. The strength was mainly catalyzed by their record Data Center revenue of $10B, up +141% from last quarter, and +171% from last year.

What surprised me, however, was their forward guidance — specifically the fact that they’re expecting $16B in revenue next quarter, beating expectations by +27%. Although the company did not provide profit guidance, they did mention their gross margins should land around 72% — which should cause their profits to land around +38% higher than Wall Street’s Q3 expectations.

The company’s potential downside risk comes from a single factor — meeting this incredible demand. I believe Nvidia has the ability to secure adequate capacity through its supply partners, as they’ve recently found new key supply partners to aid in the making of specific components such as wafers, packaging, and testing.

I’m bullish on Nvidia as the company has proven to be the world’s leading provider of semiconductors — essentially becoming the bridge between current technology and the generative AI technology of the future.

There’s absolutely a world where NVDA sees a $5T market capitalization (3X in stock price) by the end of the decade if this demand continues.

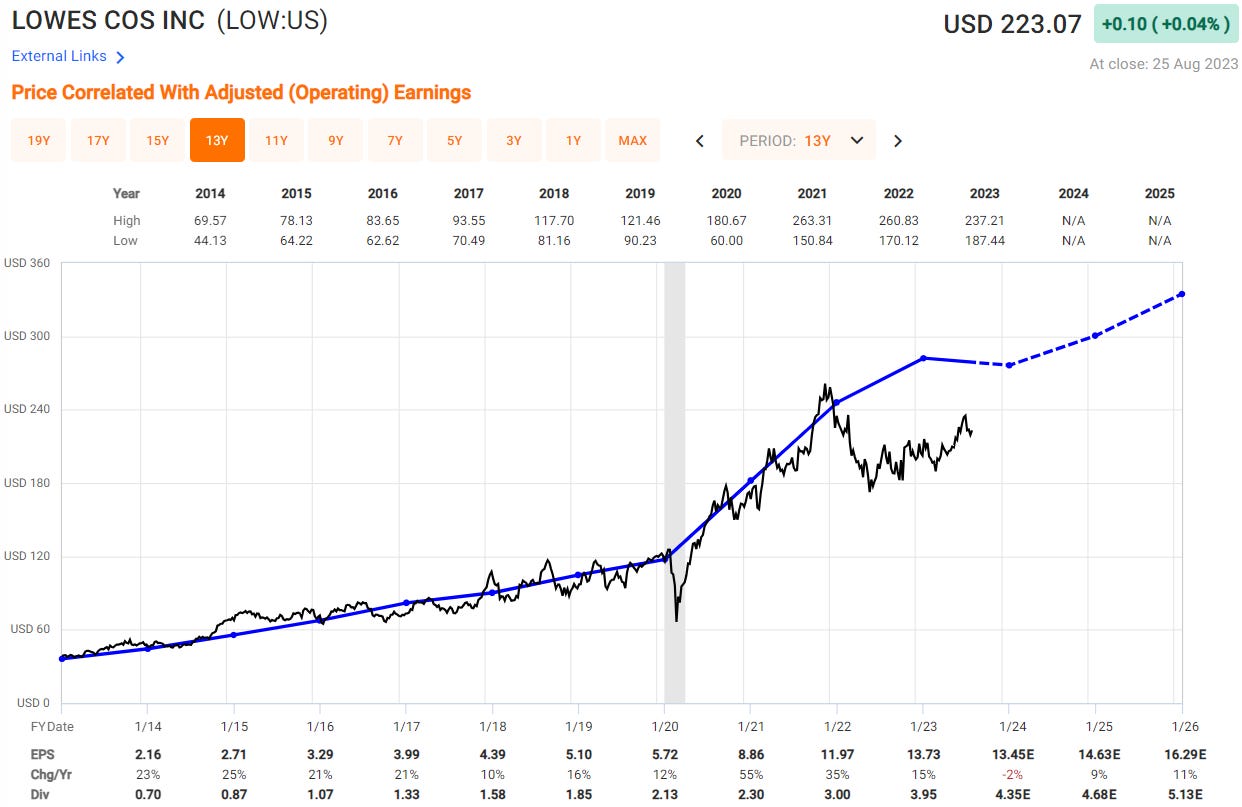

Lowe’s (LOW)

Key Metrics

Revenue: $25.0 billion, compared to $27.5 billion last year

Operating Income: $3.9 billion, compared to $4.0 billion last year

Profits: $2.7 billion, compared to $2.9 billion last year

Earnings Release Callout

“Our investments in our Total Home strategy continued to drive growth across Pro and online this quarter. And we are excited by our recent launch of same-day delivery nationwide and the expansion of our rural merchandising framework to roughly 300 stores.

During the quarter, the company repurchased approximately 10.1 million shares for $2.2 billion, and it paid $624 million in dividends.”

My Takeaway

Headline revenue and profits came in better-than-expected, and I’m continually encouraged by this management team’s execution. However, underlying trends remain mixed.

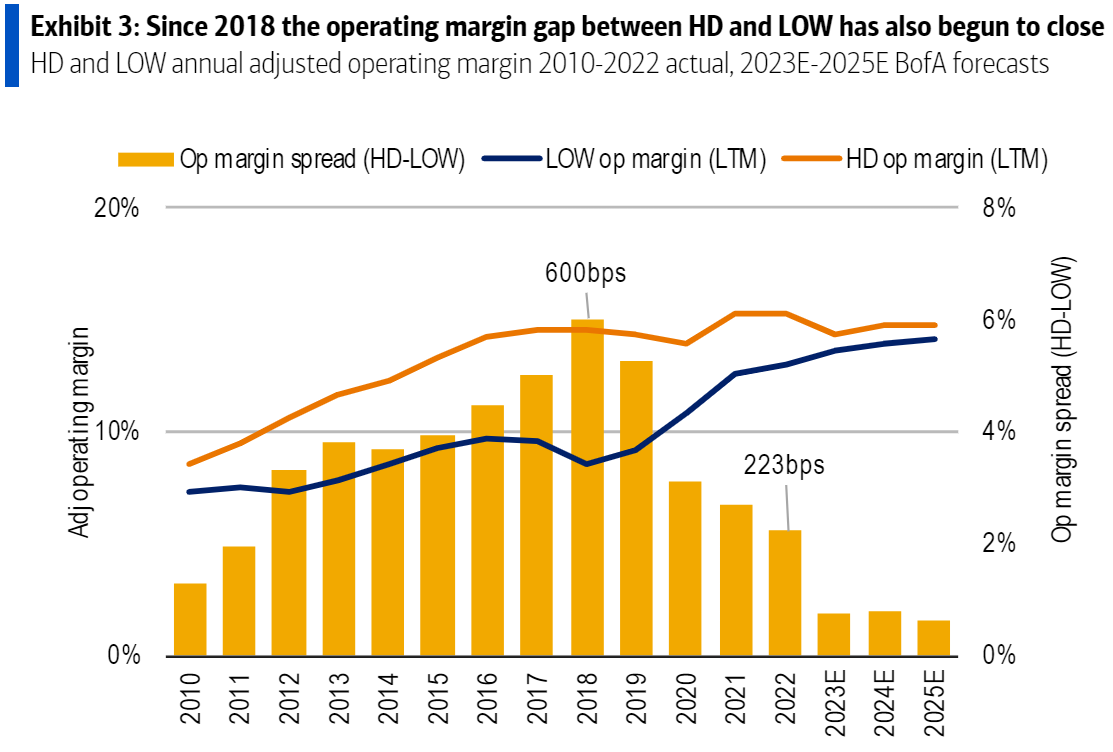

Considering the above-mention housing affordability index, expectations were high — and I think Lowe’s was able to reassure the markets that not much has changed for their story. They’re executing well during a difficult environment while taking market share from Home Depot and others.

Average ticket price was up +0.3%, improving sequentially and on a YoY basis. This reflects price increases from last year that have yet to be cycled through comparables. Ticket prices will stabilize and become more predictable in the second half of the year, which might be a risk to topline revenue.

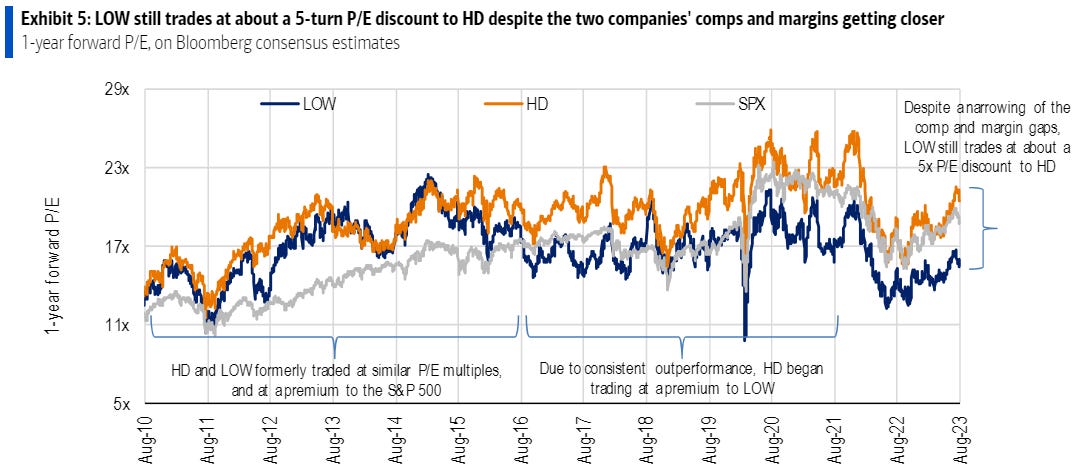

Wall Street sees +30% upside potential in Lowe’s as their competitor, Home Depot, continues to trade at a higher profit multiple — and believe Lowe’s deserves the same valuation given their ability to close the gaps in year-over-year comparables and operating margin.

As Lowe’s operating margin continues to close in on Home Depot’s, so should their discount to HD from a valuation perspective. This will be interesting to watch over the coming 6-12 months.

Lowe’s remains undervalued in my eyes, especially on a forward basis.

Snowflake (SNOW)

Key Metrics

Revenue: $674.0 million, an increase of +37% YoY

Operating Loss: -$285.4 million, compared to $207.7 million last year

Net Loss: -$226.9 million, compared to -$222.8 million last year

Snowflake as the global epicenter of trusted enterprise data is well positioned to enable the growing interest in AI/ML. Enterprises and institutions alike are increasingly aware they cannot have an AI strategy without a data strategy.”