On Thursday, the 10-year Treasury yield hit the highest level since 2007. That comes as the supply of Treasuries is expected to expand by $2.9 trillion this year and $2.4 trillion next year.

Now — Yardeni Research believes that “bond vigilantes” are “saddling up” as federal deficits continue to balloon.

The president of Yardeni Research is famous for coining the vigilantes term in the 1980s, referring to traders who protested massive deficits by selling off bonds to push yields higher.

“When asked on Bloomberg TV whether bond vigilantes are back, Yardeni replied, "I think they are. They're certainly saddling up."

He added that the bond market is typically driven by the outlook on inflation and the Federal Reserve's expected responses to it, with supply and demand for Treasurys usually less of a factor. That's because federal deficits have historically widened during recessions while the Fed is cutting rates, Yardeni explained.

"This time around, we've got the federal deficit widening when the economy is doing well. And I think the bond vigilantes are quite concerned about that," he said. "There's way too much supply."

“We don’t think this time it’s different…But from that first rate hike until recession could take a while. We continue to see a growing list of indicators which are only at these levels if the US economy is already in recession or about to enter recession.”

“We are seeing signs that equity investors are recognizing the outlook is not as sanguine as markets previously believed… A further selloff in bonds should foster a larger equity correction as investor should demand a larger risk premium to own equities.”

Takeaway: It feels like decision time has arrived for many investors — do I invest in stocks or bonds? Remember — when interest rates rise, bond prices typically go down. When interest rates decline, bond prices typically rise.

All eyes on the iShares Core US Aggregate Bond ETF (AGG):

Portfolio Updates:

What a month it’s been!

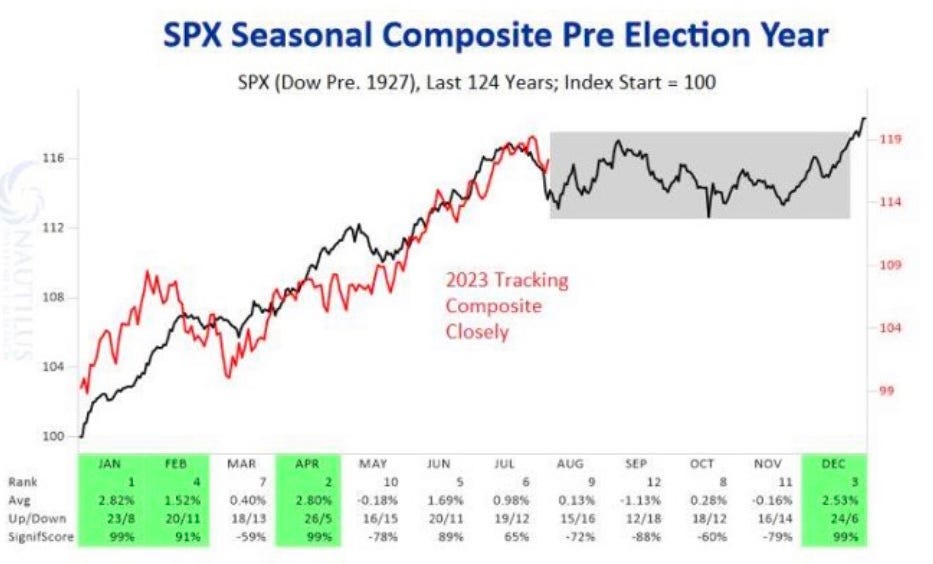

It seems like the stock market (S&P 500) peaked on the last day of July, and we’ve begun to enter a healthy correction (-4.6%). I’m not sure how low this correction might take us, but it seems like we’re right on track with how the stock market tends to perform the year before election years (in red).

Further, the pullback we’ve seen is right on track with historical norms. Below is a chart that illustrates both the median and average pullbacks the stock market has experienced after a +15% run up in price.

Assuming this pullback is truly “average,” we have another -4% or so to go. Which to me is a buying opportunity. As everyone has run for the hills — I’ve deployed more capital into both my dividend growth portfolio and cryptocurrency, lowering my average cost per share across the board.

The dividend growth portfolio is edging higher and higher, as well as outperforming the dollar-cost-averaged performance of the S&P 500 shown above (about 6.6% YTD).

The Bitcoin and Ethereum portfolio is worth around $35K and down some -$3,000. Again, nothing I’m worried about in the short-term as I fully expect the crypto market to bounce back with a vengeance in 2024 / 2025.

Week in Review — Too Long, Didn’t Read:

Monday.com continues to inch toward profitability, Walmart takes market share, Target feels the negative effects of a boycott, everyone seems to be hedging with put options, China is in a slump, homebuyers aren’t having fun, the Fed’s forward looking thoughts, and one of the most important national indicators continues to flash red.

Key Earnings Announcements:

Monday.com continues to inch toward profitability, Walmart takes market share, and Target feels the negative effects of a boycott.

Monday.com (MNDY)

Key Metrics

Revenue: $175.7 million, an increase of +42% YoY

Operating Loss: -$12.1 million, compared to -$46.2 million last year

Net Loss: -$7.0 million, compared to -$45.7 million last year

Earnings Release Callout

“We are encouraged by our second quarter results, with our strong execution resulting in quarterly records for our free cash flow and non-GAAP operating income.

We continue to demonstrate our ability to deliver sustainable growth despite the challenging macroeconomic environment, and the strength of our results through the first half of the year give us the confidence to raise our 2023 guidance.”

My Takeaway

One of my favorite stocks continues to deliver on expectations! Highly recommend everyone take 15 minutes to read their Letter to Shareholders for this quarter — it’s packed with financial and operational information that will really help you understand why I like this company so much.

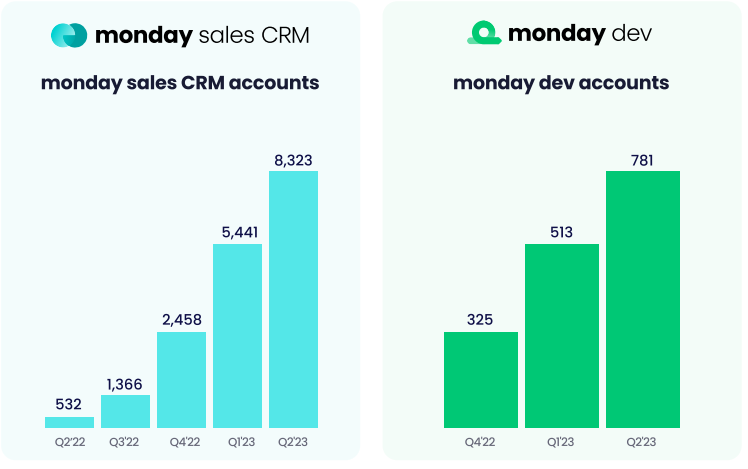

Something I’m personally very encouraged to see is the quick adoption of both Monday Sales CRM and Monday Dev by their existing customers.

This is that “land and expand” strategy we’ve seen some of the most successful technology companies implement. Beyond this quick adoption, their strong +42% revenue growth this quarter was again catalyzed by enterprises (>$50K in ARR) signing up for the platform, now sitting at 1,892 (+63% YoY).

And as always, I’m very encouraged by this quarter’s margin and operating expenses. Having gone from a net operating margin of negative -12% this quarter 2022 to now positive 9% in 2023. Not to mention their FCF margin climbed even higher to 26% — incredible!

Monday.com remains one of my largest “risky” holdings in my portfolio, and I have every intention to continue to expand upon that position by dollar cost averaging.

Walmart (WMT)

Key Metrics

Revenue: $160.3 billion, an increase of +6% YoY

Operating Income: $7.3 billion, an increase of +7% YoY

Profits: $7.9 billion, an increase of +53% YoY

Earnings Release Callout

“We had another strong quarter. Around the world, our customers and members are prioritizing value and convenience. They’re shopping with us across channels — in stores, Sam’s Clubs, and they’re driving eCommerce, which was up 24% globally.

Food is a strength, but we’re also encouraged by our results in general merchandise versus our expectations when we started the quarter.”

My Takeaway

Driven higher by their average ticket size being up +3.4% and transactions up +2.9%, United States comparable sales were up +6.4% this quarter — beating Wall Street’s +4.1% expectations. Food led the charge, with prices up high-single digits — while apparel, home, and sporting goods comped lower year-over-year.

Their private food brands gained about +0.5% market share throughout the quarter given its lower price point.

Given the company’s guidance, Walmart seems well-positioned to continue to take market share from other large retails this Holiday season. Another positive for the quarter is the incremental revenue they’re generating from Walmart Connect and Walmart+, ultimately supporting a higher valuation multiple when compared to their peers.

A few positives that caught my attention included 1) strength of their top-line revenue when compared to peers — alluding to market share growth, 2) well-managed inventories and 3) an acceleration in e-commerce sales (+4%).

Walmart’s stock price is now trading at 52-week highs again, which is great! However, I’m on the sidelines until I see a true “thesis” to invest.

Target (TGT)

Key Metrics

Revenue: $24.4 billion, compared to $25.6 billion last year

Operating Income: $1.2 billion, an increase of +273% YoY

Profits: $835.0 million, an increase of +356% YoY

Earnings Release Callout

“Our second quarter financial results clearly demonstrate the agility of our team and the resilience of our business model, as we saw better-than-expected profitability in the face of softer-than-expected sales.

At the same time, we continue to take a cautious approach to planning our business, and have therefore adjusted our financial guidance in anticipation of continued near-term challenges on the topline. This approach, along with the long-term investments we're making in our business and strategy, position us to deliver sustainable, profitable growth in the years ahead."

My Takeaway

Well, that was interesting! As you all might remember reading in the news, there was a nationwide boycott against Target earlier this summer — and it seemed to have worked. Target experience their first quarterly sales decline in six years.

Their stock price is also trading down -14% year-to-date, underperforming the S&P 500 by -28% since the start of the year.

By month, comparable sales declined by -3%, -7%, and -5% in May, June, and July. Trends in August were consistent with the summer-long decline. Wall Street is forecasting continual top-line pressure for Target given macro discretionary pressures, inflation, and student loan payment resumption beginning in October.

However, the Street does see a silver lining. In 2024, they’re forecasting margin expansion opportunities to present themselves from 1) freight and transportation cost recovery, 2) the non-recurrence of various inventory reduction investments, and 3) the continued shift-back to more profitable in-store and same-day delivery transactions.

However, shrink / theft remains a persistent headwind for the company.

I’m on the sidelines here. Too much risk, especially social, for me right now.