One quick callout to get things started — the 3+ year pause of payments on federal student loans will resume in August for tens of millions of Americans.

What do you think happens as a result? Increased credit delinquencies on the way? This is something to keep an eye on when the fall rolls around.

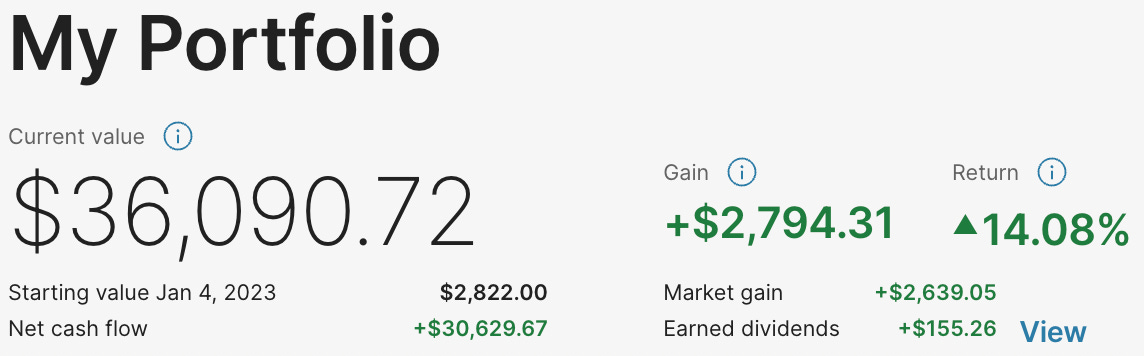

Portfolio Updates:

In case you missed it, I shared a deep dive into my favorite AI stocks right now — categorized by infrastructure developers and efficiency beneficiaries.

In this post I detail the names of companies I plan to expand positions inside of / open in the coming weeks. Beyond that, the portfolio is widely unchanged. For those of you who are Founding Members and joined our livestream Monday night, you might remember me sharing my excitement about the “Small Cap Catchup” trade.

I believe this trade is beginning to start showing some momentum as the (IWO) traded up +2.1% this week, while the S&P 500 gained only +0.3% and the Nasdaq 100 declined -0.3% during the same period.

We also briefly discussed how Cathie Wood’s ARKK, after underperforming YTD, might begin to “catch up.” This seemed to begin to take place this week as well.

I’m also excited about Adobe’s earnings release next week — given their viral AI tools, I’m expecting fireworks.

GitLab is ugly (but interesting), Ollie’s is probably going to be a new position in my “risky” category, DocuSign needs to improve profitability, Apple is set to charge $3500 for high-tech goggles, Saudi Arabia cements its dominance in the world of golf, Coinbase remains in the crosshairs of the SEC, Consumer Credit could get ugly over the coming months, and Factory Orders come in lower than expected.

Key Earnings Announcements:

GitLabs is slowing turning their ship around, Ollie’s is poised to explode, and DocuSign remains in a rut.

GitLab (GTLB)

Key Metrics

Revenue: $126.9 million, an increase of +45% YoY

Operating Loss: -$58.2 million, compared to -$42.9 million last year

Net Loss: -$53.0 million, compared to -$26.6 million last year

Earnings Release Callout

“Revenue of $126.9 million grew 45% organically year-over-year, and our non-GAAP operating margin improved by approximately 1,700 basis points year-over-year as the team continued to focus on addressing customer priorities and improving operating efficiency.

Against a backdrop of macroeconomic uncertainty, customers are looking to our AI-powered DevSecOps platform to drive efficiencies, increase productivity, and accelerate their pace of innovation. We are poised to make the most of the estimated $40B total addressable market opportunity before us.”

My Takeaway

If you want to see a nightmare in real life — just look at GTLB’s stock price. The company IPO’d and then their stock completely falls off of a cliff. GTLB is sort of a in a tough spot here — the company is “only” guiding to +30% growth next year, while still not adj. EBITDA or free cash flow positive.

Sure, those figures are improving (as they should) but this company won’t be adj. EBITDA or free cash flow positive at least until 2025. With that being said, if you believe in the longevity of this company — now is the perfect time to buy.

Moving now toward their actual results: GTLB’s stock popped +30% after their management team guided toward higher 2023 revenue expectations. Investors were also enthused about the idea of GTLB leveraging AI to expand their Code Suggestion.

Their customer base also continued to move in the right direction, with their >$100K customers growing by +39% YoY. The company also introduced a new ModelOps product, priced at just $9 / seat, which further expands their total addressable market.

To be honest, the company has legs — annual recurring revenue is up, margins seem to be moving in the right direction (although very slow), and revenue continues to trend higher. With that being said, I’ll be keeping a close eye on their net retention rates as they seem to be slowing down faster than management anticipated at just 128%.

On the sidelines, but intrigued.

Ollie’s (OLLI)

Key Metrics

Revenue: $459.1 million, an increase of +13% YoY

Operating Income: $38.5 million, an increase of +124% YoY

Profits: $31.0 million, an increase of +147% YoY

Earnings Release Callout

“We are pleased with our first quarter performance, which exceeded our expectations and was driven by strong comparable store sales, new store productivity, and margin expansion. Customers are responding to our compelling deals, resulting in accelerating transaction trends and we are encouraged to see our product offerings appealing to a wider customer base that includes more higher income and younger-age shoppers.

Our deal flow remains robust, and we believe that we are well positioned in the current environment as consumers are increasingly looking for value. As a result of our strong first quarter performance and continued momentum in the business, we are raising our outlook for fiscal year 2023.”

My Takeaway

Main Street loves this company — but Wall Street doesn’t seem to realize that yet. OLLI reported comparable sales of +4.5%, above their +2.0% guidance — they also raised their Q2 comparable sales expectations to +2.5% (up from +1.5%).

Considering where the economy is right now — and where it might be headedduring the remainder of the year — I think bargain / value-driven retailers like OLLI are poised for growth in the coming 12-18 months.

Few things I like about this company right now: better-than-expected top-line growth and solid comparables growth, while transaction trends accelerated with more higher-income and younger shoppers. The strongest categories were food, candy, health/ beauty, lawn/garden, and flooring.

Inventory levels declined -4% YoY, while management noted their “close out” market remains very strong. Finally, this company has $275M in cash to repurchase stock if desired. They repurchased $12M during the quarter and have $125M more authorized to be repurchased.

What worries me: gross margins came in at 38.9%, lower than management’s 39.2% expectations. I’m hoping this doesn’t turn into a trend.

All-in-all, I’m liking this company a lot and believe as the economy continues to see turbulence they’ll benefit. I’ll open a position in my “risky” subsection of the portfolio in the coming weeks.

DocuSign (DOCU)

Key Metrics

Revenue: $661.4 million, an increase of +12% YoY

Operating Loss: -$4.6 million, compared to -$19.2 million last year

Profits: $0.5M, compared to -$27.4 million last year

Earnings Release Callout

“DocuSign's first quarter results, coupled with traction on our strategic objectives reflect a solid start to the year. While we have work ahead of us, I am encouraged by our progress to enable smarter, easier, trusted agreements. As we continue to execute on our strategy and leverage our competitive advantages, notably in AI, DocuSign is well positioned for the future.”

My Takeaway

DocuSign has always been that ugly step child — it’s a growing technology company, but it’s not yet profitable, their growth has slowed tremendously, and their gross profit margins are hardly impressive.

With that being said, things seem to finally be turning around for the company — their operating margins hit a record 26%, their free cash flow came in at a record $214M, and they seem to be integrating generative AI into their Intelligent Agreement suite.

With that being said — they’re also experiencing longer sales cycles, net retention rates are down -2% QoQ and are expected to continue trending lower next quarter, and competition continues to increase.

With that being said, I’ll remain on the sidelines until we see 1) product innovation that will reinvigorate customer growth or 2) profitability.