Starting off this jam-packed summary with a callout from our friend Jaguar Analytics:

He argues that we are currently in “Quad 4” of the S&P macro trends — the time in which defensive groups lead. It’s characterized as “lower inflation, low real economic growth.” Quadrants in the above graphic are numbered in a clockwise fashion.

Of course — it’s difficult to predict when the macro environment shifts from one quadrant to the next. A big increase to economic output could lead to rising inflation.

He believes that you will continue to see defensive groups lead: XLP for Consumer Staples and XLV for Healthcare.

Let’s jump into our most comprehensive update of the year thus far!

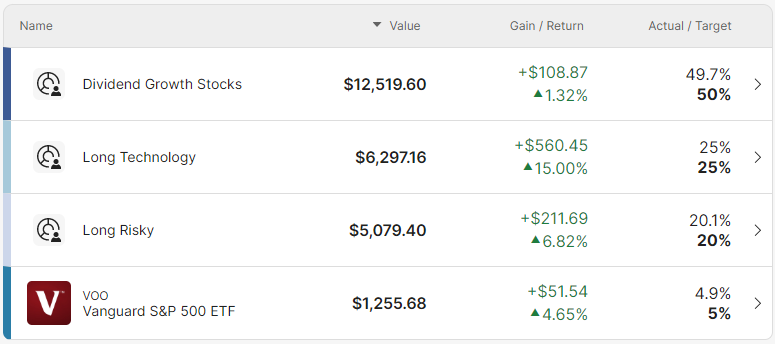

Portfolio Updates:

As I shared last week, I transferred $10K more into the Dividend Growth Portfolio.

Given the shakiness we’ve seen the crypto markets over the weekend, I’m expecting weakness in the stock market throughout the remainder of April — potentially giving me an opportunity to dollar cost average into my portfolio.

The Portfolio Tracker (paying subscribers-only) is completely up to date — having now also added both my new Verizon and Meta Platforms positions.

Quick Update: I opened and closed the $TAP call options last week for a +97% gain on my $2,200 invested — not bad for a few days work!

I still believe there is some upside to be had with these $57.50 5/19 call option contracts, I’m just not willing to take on the risk given the volatility we might experience heading into their May 2nd earnings call.

In other words, I took my money and ran.

Finally, it’s nice to see a few of the specific names we’ve called out over the last few months perform the way they have:

Kicking myself for not buying more Hims and Hers Health stock back in December, but also when it was below $4 during the Summer of 2022. Hindsight is 20/20.

Week in Review — Too Long, Didn’t Read:

Netflix delayed their crackdown on password sharing, ASML has $38B+ in their backlog, Tesla is practically giving away their vehicles, Americans are trapped in Sudan, Apple opens its first two storefronts in India, Lululemon regrets buying Mirror, a full breakdown of the Housing Market, The Conference Board’s Leading Economic Index still looks bleak, S&P’s PMI readings for Services and Manufacturing show some improvement, and St. Louis Fed President Bullard wants more hikes.

Key Earnings Announcements:

Netflix delayed their crackdown on password sharing, ASML has $38B+ in their backlog, and Tesla is practically giving away their vehicles.

Netflix (NFLX)

Key Metrics

Revenue: $8.1 billion, an increase of +4% YoY

Operating Income: $1.7 billion, compared to $2.0 billion last year

Profits: $1.3 billion, compared to $1.6 billion last year

Earnings Release Callout

“With Moody’s recent upgrade, we achieved investment grade status.

Netflix is the leading streaming service based on engagement, revenue and profit and we are working to build on that in 2023, by seeking to expand operating margin to 18%-20% and to generate at least +$3.5B of free cash flow (up from our prior expectation of at least $3.0B of FCF).”

My Takeaway

After reading through Netflix’s letter to shareholders, I noticed a theme — the company is “controlling their controllables.”

Essentially, their operating margin was 21% this quarter compared to the 25% last year’s quarter — while 3% of that 4% decline was due to a weaker US dollar. Their $1.7B in operating income came in +$100M higher than the $1.6B they forecasted, a good thing.

The company reiterated their long-term financial objectives of double-digit revenue growth, expansion of their operating margin, and positive free cash flow on a consistent basis.

However, they did delay the rollout of their password sharing crackdown from Q1 to Q2 — pushing back the extra revenue they expect to realize because of this crackdown now to Q3.

The company is trading around ~30X price-to-earnings, certainly below their historical average — but perhaps justified given their tremendous deceleration in revenue growth. With that being said, I’m considering adding it to the “Risky” section of my portfolio.

There are a few red flags (slowing growth, lower margins, etc.) but there is also a big focus on free cash flow growing by billions each year through 2026. I’ll bite.

ASML Holdings (ASML)

Key Metrics — reported in Euros

Revenue: $6.7 billion, an increase of +90% YoY

Operating Income: $2.2 billion, an increase of +181% YoY

Profits: $2.0 billion, an increase of +181% YoY

Earnings Release Callout

“We continue to see mixed signals on demand from the different end-market segments as the industry works to bring inventory to more healthy levels.

Some major customers are making further adjustments to demand timing while we also see other customers absorbing this demand change, particularly in DUV at more mature nodes. The overall demand still exceeds our capacity for this year and we currently have a backlog of over €38.9 billion. Our focus continues to be on maximizing system output.”

My Takeaway

As a quick refresher, ASML Holdings manufactures the machines that manufacture semiconductors — therefore their customers are semiconductor producing companies like TSM, AMD, and others.

The company is forecasting +25% growth in revenue in 2023, and their current backlog seems to have the capacity to support that. However, investors are beginning to become skeptical of how this might translate into growth during 2024 — TSM, for example, is cutting their capex which would negatively impact ASML.

Wall Street seems to believe Samsung and Intel will likely ramp up their capex spend in 2024, and others like AMD, Qualcomm, and Apple might join.

It’s also important to note that 20% of ASML’s $38B backlog comes from China — so as instability continues between China and the rest of the world, this might have a negative impact on the company.

With all of that being said, I’m going to remain a shareholder and continue to dollar cost average into my position. ASML has a monopoly on the semiconductor industry, growing stronger with every new EV, smartphone, laptop, and data center.

To me, it’s obvious where this company is headed. The volatility in the near-term will soon be forgotten as the stock price climbs back to all-time-highs in the coming years.

Tesla (TSLA)

Key Metrics

Revenue: $23.3 billion, an increase of +24% YoY

Operating Income: $2.7 billion, compared to $3.6 billion last year

Profits: $2.5 billion, compared to $3.3 billion last year

Earnings Release Callout

“In the current macroeconomic environment, we see this year as a unique opportunity for Tesla. As many carmakers are working through challenges with the unit economics of their EV programs, we aim to leverage our position as a cost leader.

We are focused on rapidly growing production, investments in autonomy and vehicle software, and remaining on track with our growth investments.”

My Takeaway

In my humble opinion, 2023 marks the year in which Tesla’s business model shifts away from optimizing for near-term cash flow to stay in business and instead toward maximizing long-term profitability per customer.

This was made evident after their comments around full self-driving to be on track commercialized by the end of the year — they’re focused on growing their upgradable used base. With that being said, there will likely be near-term margin pressures for the company as they continue to cut prices to maintain strong volume sell-through.

Tesla reiterated their guidance for 2023 production of 1.8 million vehicles, below their historical +50% compounded annual growth rate. They claim their Cybertruck production is expected to begin in Q3, with an S-curve ramp higher.

Tesla is essentially waging a price war — which is horrible news for other EV manufacturers. It’s abundantly clear that Elon is comfortable breaking even or potentially losing money on the hardware (their vehicles) and while actually making money selling the software (full self-driving, etc.) over time.

All in all, I remain a happy shareholder. Tesla is not going to see a material slowdown in volumes, they’ll continue to upsell their customers on high-margin software updates, and they have a cult-like following other EV companies cannot compete with.