Social arbitrage, as pioneered and made famous by Chris Camillo and the Dumb Money team, is defined as profiting from an incredibly popular social trend.

Chris has publicly grown his brokerage account from $80K to $60M over the last few decades by betting on or betting against companies whose bottom lines will be impacted by popular social trends.

For example, Chris saw the “slime trend” early and realized a key ingredient to make at-home slime was Elmer’s Glue — owned by Newell Brands (NWL).

The popular trend catalyzed insane profits for a relatively “boring” company — just take a look at their stock price from 2013 to 2015.

Chris made millions by spotting this trend early, betting big on the company, and riding the wave. Another notable trade of his was Crocs (CROX) — every kid has them and every middle-aged dad owns a pair of Hey Dudes.

I mention this “social arbitrage” trading style in this portfolio update because I’m taking part in my own social arbitrage trade — Molson Coors (TAP) — Bud Light’s main competitor.

This isn’t political stance and I’m not betting on Bud Light’s downfall.

However, with all of the recent controversy happening with the company I’ve observed countless instances where people are choosing to drink Coors Light or Miller Lite instead of Bud Light.

Both of these beers are owned by Molson Coors (TAP).

I have a hunch that Molson Coors is seeing a huge influx of new customers and during their Q1 earnings call (May 2nd) will raise their full-year guidance in response — causing the stock price to rally.

A few notable callouts:

TAP’s daily trading volume hasn’t seen an uptick — causing me to believer this trade idea hasn’t exactly gone “mainstream” yet.

Wall Street has yet to publish any sort of report or update on the company, and they’re estimating TAP’s profits will decline by -1% during 2023.

It’s interesting to see real life examples of people on Twitter having a similar hunch — here’s an example.

What I’m doing:

I buying a few thousand dollars worth of call options on Molson Coors (TAP) — specifically the May 19 $57.50 contracts. I might also pick up some May 19 $60.00 contracts as well.

For this trade to be profitable, TAP’s stock price needs to rise above $58.80 by May 19 — or about +5%.

I think this is entirely possible assuming they report in-line earnings on May 2nd and raise their full-year guidance in response to the recent demand during the earnings call.

You’re more than welcome to trade alongside me on this idea, sit it out, share it with a friend — whatever you want to do! I’m just sharing the idea and how I’m personally executing upon it.

Quick update on the portfolio — I’ve deposited another $10K into my brokerage account — it should be deployed sometime later this next week.

I’m also opening a small position (3% of total portfolio weighting) in Meta Platforms (META) — the company has done a wonderful job proving their focus on efficiency and moving toward both profitability and free cash flow.

Since their public debut in 2012, the company’s stock price has closely followed free cash flow — as exacerbated by their recent decline in stock price. As these efficiencies compound on themselves, Meta Platforms seems poised for continued success.

I’ve also continued to expand my positions in Bitcoin and Ethereum — now having nearly $30K invested into these cryptocurrencies at a 75 / 25 split.

If you want to check out specific holdings — visit the Portfolio Tracker!

Week in Review — Too Long, Didn’t Read:

JPMorgan Chase sees $50B in new deposits, UnitedHealth Group reaffirms their +13% annual EPS guidance, Delta Air Lines is set to generate $6.2B in FCF through 2025, the IMF releases some negative outlooks on the state of the global economy, the botched Strategic Petroleum Reserve situation continues to haunt the U.S., Inflation results, our favorite quotes from the Fed Meeting Minutes, and the Small Business Index.

Key Earnings Announcements:

JPMorgan Chase sees $50B in new deposits, UnitedHealth Group reaffirms their +13% annual EPS guidance, and Delta Air Lines is set to generate $6.2B in FCF through 2025.

JPMorgan Chase (JPM)

Key Metrics

Revenue: $38.3 billion, an increase of +25% YoY

Profits: $12.6 billion, an increase of +52% YoY

Earnings Release Callout

“Our years of investment and innovation, vigilant risk and controls framework, and fortress balance sheet allowed us to produce these returns, and also act as a pillar of strength in the banking system and stand by our clients during a period of heightened volatility and uncertainty.”

My Takeaway

The bolded section above is the story here — after Silicon Valley Bank collapsed, every mid-sized tech company and startup moved their funds to either JPMorgan Chase or some other big bank.

For instance, JPM mentioned during their earnings call that they received +$50 billion in deposits during the quarter — specifically in the form of business bank accounts.

The most interesting observation from this quarter’s earnings results — and why the stock moved higher after the report — was their guidance around net interest income. In case you’re unfamiliar, interest income is income you make by parking cash in interest-bearing accounts — like a high-yield savings account.

However, instead of high-yield savings accounts banks take your deposits and park it into a ton of different things — including mortgage-backed securities, Treasury Bills, and more.

Considering JPM had $50B more in deposits to “play with” this quarter, they were able to generate a substantial amount of interest income — and will continue to for quarters to come.

I’m not an investor into bank stocks, and won’t be opening a position in JPM.

UnitedHealth Group (UNH)

Key Metrics

Revenue: $72.8 billion, an increase of +14% YoY

Operating Income: $8.1 billion, an increase of +16% YoY

Profits: $5.8 billion, an increase of +12% YoY

Earnings Release Callout

“Our strong, enterprise-wide growth this quarter is a direct result of our colleagues’ unwavering commitment to offering more health services to more people and connecting consumers with greater access to high-quality, affordable care.”

My Takeaway

UnitedHealth Group delivered strong quarter results — with revenue beating expectations by +$2B. The Optum business segment grew revenue by +25% YoY, candidly beating Wall Street’s revenue expectations by nearly +$4B.

Management attributed Optum’s continued growth toward an increase in value-based care patients — helped by the Change acquisition.

Despite the beat, shares of UNH traded down -2%. I think this is mainly because their updated earnings per share guidance seems to be “back-end” loaded, as more of their profits will materialize during the second-half of 2023.

What keeps me excited about this company is their Optum business segment. This subsidiary was created in 2011, and has since grown to make up nearly 60% of the company’s total revenue. I believe this business segment’s continued growth will be the ultimate catalyst for the company to continue to deliver +13% annual EPS returns through 2026.

UNH is always a great “buy the dip” stock.

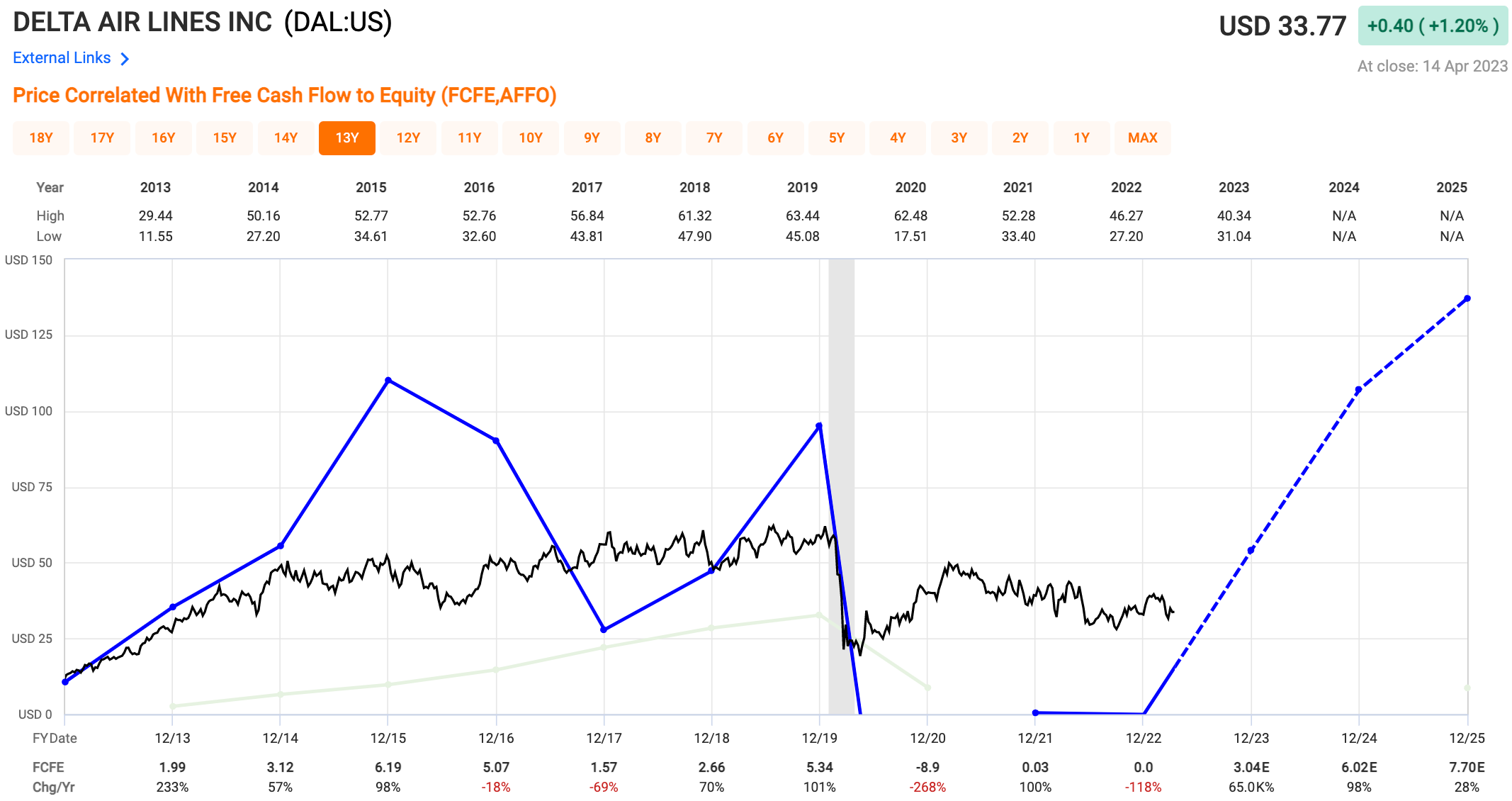

Delta Air Lines (DAL)

Key Metrics

Revenue: $12.8 billion, an increase of +36% YoY

Operating Loss: -$277.0 million, compared to -$783.0 million last year

Net Loss: -$363.0 million, compared to $940.0 million last year

Earnings Release Callout

“For the June quarter, we expect to deliver record revenue, and an adjusted operating margin of 14 to 16 percent with earnings per share of $2.00 to $2.25.

With solid March quarter profitability and a strong outlook for the June quarter, we are confident in our full-year guidance for revenue growth of 15 to 20 percent year over year, earnings of $5 to $6 per share and free cash flow of over $2 billion.”

My Takeaway

As you all know, I’m not an active investor in any sort of airline stocks — there are simply too many variables that negatively impact their bottom lines i.e. higher fuel costs, weather-related events, and more.

In my opinion, the key debate with airline stocks remains the strength of demand vs. macroeconomic headwinds of 2023 — however, Delta is an airline on the more affluent side of the aisle which could translate into resilience.

Again, I’m not an active investor in Delta — but if I was, their June Investor Day would likely be a near-term catalyst for the stock. The company will likely highlight their long-term revenue drivers as well as their SkyMiles cash flow.

According to some Wall Street analysts, DAL will generate $6.2B in free cash flow through 2025 — which includes $1.4B in 2023. As someone who loves cash flowing businesses, I’m tempted to learn more about Delta despite my concerns.

Maybe after their Investor Day… no position for now.

Investor Events / Global Affairs:

The International Monetary Fund’s grim forecasts and empty promises with the SPR.