And the market has been acting like the ‘Santa Claus Rally’ is nearing an end.

Are we certain of this? Absolutely not, but let’s see what five of the most influential investors in the world have to say about the 2023 outlook:

Jamie Dimon, CEO of JPMorgan:

“[Consumers] have a trillion and a half dollars more in their checking accounts than they did pre-Covid. So they’re spending it down, and that’s the good news… the other news — which is not good — is that rates are at 4% and on their way to 5%, inflation is eroding everything I just said, and that trillion and a half dollars will run-out some time mid-year next year. So, when you’re looking out forward — those things very well may derail the economy and cause this mild-to-hard recession that everyone is worried about.”

David Solomon, CEO of Goldman Sachs:

“If you’re running a big financial services firm, I think you have to assume that we have some bumpy times ahead. And you have to be a little more cautious with your financial resources, with your sizing and footprint of the organization. I think you have to expect that activity levels are going to be more constrained in a tougher economic environment… We’re predicting economic growth will slow… I certainly think we could see a recession in 2023.”

Rebecca Patterson, CIO of Bridgewater Associates:

“We continue to believe that there’s another shoe that has to drop. And that is — the economy. It’s resilient today still, with the exception of housing, but we think the Fed is going to have to push demand lower to get that wage inflation down.”

Stanley Druckenmiller, Former Chairman & President of Duquesne Capital

“I don’t rule out — it’s not my forecast — but I don’t rule out something really bad. Why? Because if you look at the liquidity situation that has driven this — we’re going from all this QE to QT, we’re following an asset bubble, we’ve been doing all this running down on the SPR… QT has been almost entirely offset by Janet Yellen running down the Treasury savings account… our central case is a hard landing by the end of ‘23.

Bill Ackman, Founder & CEO of Pershing Square Capital Managment

“I think once the market starts to see inflation taper, and taper pretty quickly, they can begin to predict that the Federal Reserve is going to take its foot off the brake a bit and perhaps start taking down rates. I think that will be a perceived and probably likely buying opportunity… More toward the end of 2023… We still have the overhang of a war… I think it’s not noble, but unfortunately I think it continues. And I think that will continue to cloud the economic picture in Europe, I think it will continue to have an impact on energy prices, food prices… It’s a challenging time.”

Accenture is seeing cyclical demand erode into their consulting business, Adobe seems undervalued, Oracle’s capital expenditures are ramping higher, Microsoft must convince the FTC that buying Activision Blizzard isn’t a power trip, Goldman Sachs is set to lay off thousands, Yum! Brands has a tasty investor day, inflation is improving, Jerome Powell says that rate cuts aren’t planned for 2023, and Retail Sales slump.

Key Earnings Announcements:

Accenture missed consulting booking expectations by more than $1B+, Adobe pulled in record operating cash flows, and Oracle is set to spend $9B+ in CapEx throughout 2023.

Accenture (ACN)

Key Metrics

Revenue: $15.7 billion, an increase of +5% YoY

Operating Income: $2.6 billion, an increase of +7% YoY

Profits: $2.0 billion, an increase of +10% YoY

Earnings Release Callout

“Today, all strategies lead to technology, and Accenture’s depth and breadth, leading ecosystem relationships and continuous innovation are enabling clients to digitize faster, build greater resiliency and optimize costs.”

My Takeaway

Accenture reported solid quarterly results — with revenue, margins, and earnings ahead of Wall Street’s estimates. Despite this, their stock traded down -6% likely because of a few things.

1) Consulting bookings of $8.1B were well below the $9.4B Wall Street was expecting. Their management team also said during the earnings call that they expect Consulting bookings to decline modestly next quarter.

2) Their forward margin guidance calls for a meaningful decline year-over-year.

Their management team also called out an increase in macroeconomic uncertainty with 2023 GDP estimates falling over the last 90 days. While clients continue to engage with ACN — they’re more focused on cost savings. More companies are becoming cautious with their decision-making timelines, and are leaning more toward shorter engagements.

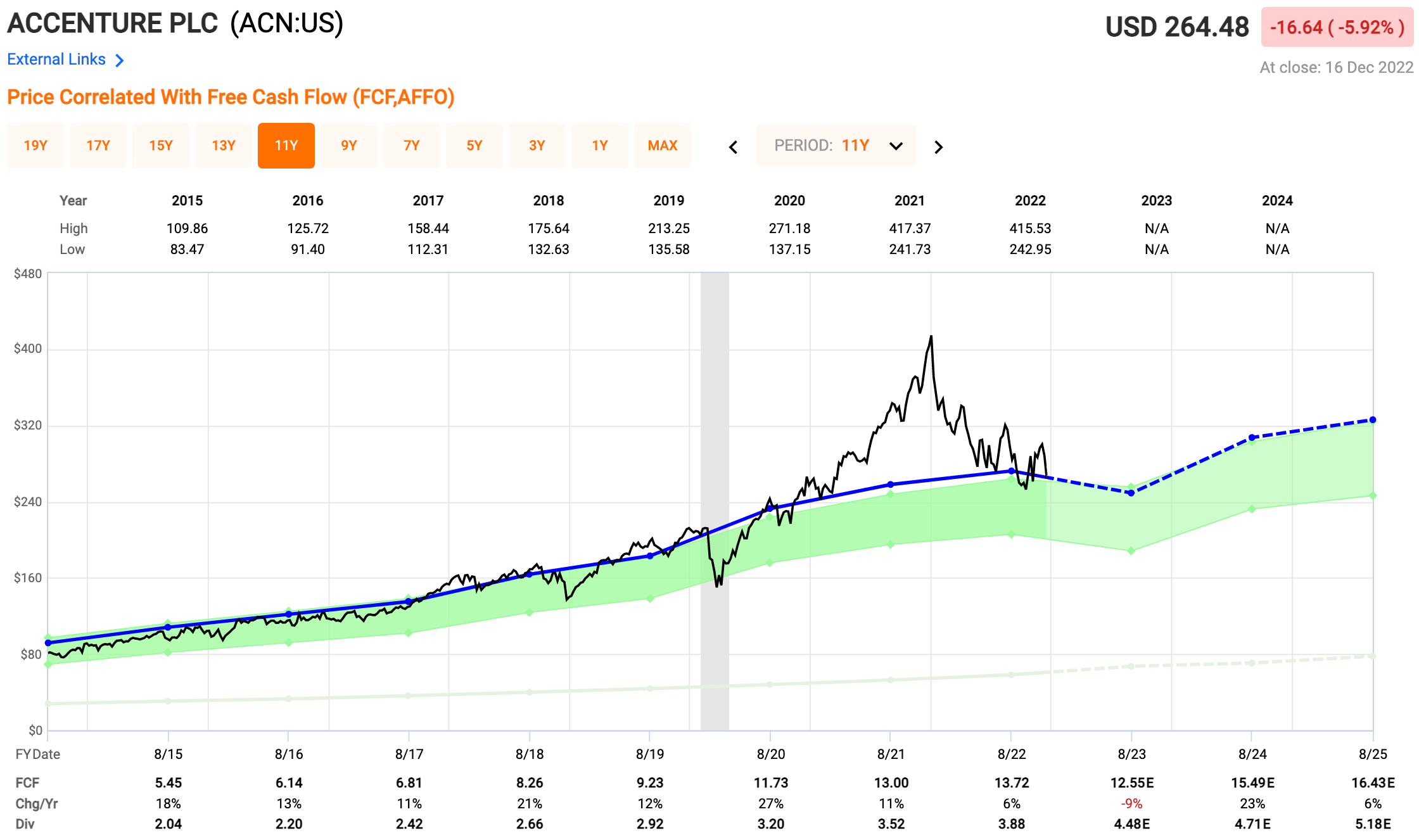

From a valuation perspective, it seems like ACN has really begun to fall off its wildly high forward FCF multiple of 32X and is now hovering around 19X — a historical average. Assuming all of Wall Street’s estimates about their future FCFs (blue dotted line) come true — the company would only be trading around the $320 / share range by 2H25. This +22% upside sounds great — but when extrapolated over the next ~3 years doesn’t leave much upside.

I’m going to pass — no position given their current consulting uncertainty.

Fast Graphs

Adobe (ADBE)

Key Metrics

Revenue: $4.5 billion, an increase of +10% YoY

Operating Income: $1.5 billion, flat YoY

Profits: $1.2 billion, compared to $1.23B last year

Earnings Release Callout

“Adobe’s outstanding financial performance in fiscal 2022 drove record operating cash flows of $7.84 billion. Strong demand for our offerings, industry-leading innovation and track record of top- and bottom-line growth set us up to capture the massive opportunities in 2023 and beyond.”

My Takeaway

Now this is a company I’m willing to get excited about — even during macroeconomic uncertainty. Re-read that quote above — record operating cash flow. Let’s go through some positives and negatives, then discuss stock price.

Positives: record net new Digital Media annual recurring revenue (ARR) of $576M — this increased +19% YoY and was +$26M above estimates. Creative ARR increased +4% quarter-over-quarter (fast sequential growth), Document ARR increased +23% YoY, and the company repurchased 5M shares of outstanding stock. Oh! Can’t forget the record operating cash flow of $7.8B.

Negatives: EMEA and Asia revenue growth has been relatively weak, remaining performance obligations grew at only +9% (slower than revenue), and operating margins compressed by -50 basis points.

Here’s my perspective — I’m encouraged by the broad strength across the business (creative, document, and experience clouds) as well as the incredible amount of operating cash flow generated during the quarter. However, I’m near-term cautious given the Figma acquisition. It’s really hard to try and predict how that completion will impact their share price in 2023.

With that all being said, it’s evident that the company’s stock price is trading at a discount to historical operating cash flow (blue line) multiples. Assuming the company is able to close the Figma acquisition and continue to provide and execute upon clear strategies and initiatives — there is clear upside to be had. $770 / share by 2H25 could be on the table with this one.

I’ll add this stock to the “opportunistic” side of the portfolio. I think this one will continue to trade sideways / down until we get more clarity on the acquisition — but there are clear tailwinds to invest toward.