Last week was one of the crazier weeks of the second half of 2023.

Let’s jump right in.

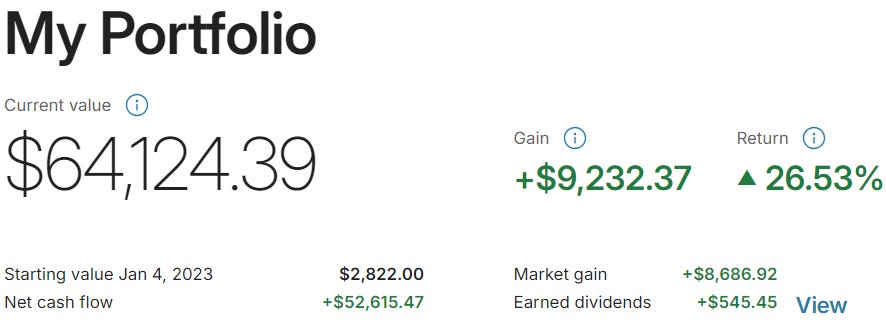

Portfolio Updates:

As you all can see, I’ve added another $10K to my crypto portfolio, having already invested $5K of that throughout the week. I’ll deploy the other $5K during the remaining few weeks left in the year.

I remain incredibly bullish on Bitcoin, Ethereum, and Chainlink as we head into 2024 / 2025 — I plan to hold these crypto investments for the foreseeable future. Below is a chart I shared with our Founding Member subscribers during a September livestream when Bitcoin was trading around ~$26K (up +69% since then) illustrating historical cycles of the cryptocurrency.

I obviously am not trying to predict the future here, but with the Spot Bitcoin ETF to be decided upon in the coming weeks — I believe we’ll continue to experience an uptrend over the coming 12-18 months (and I want to be along for the ride).

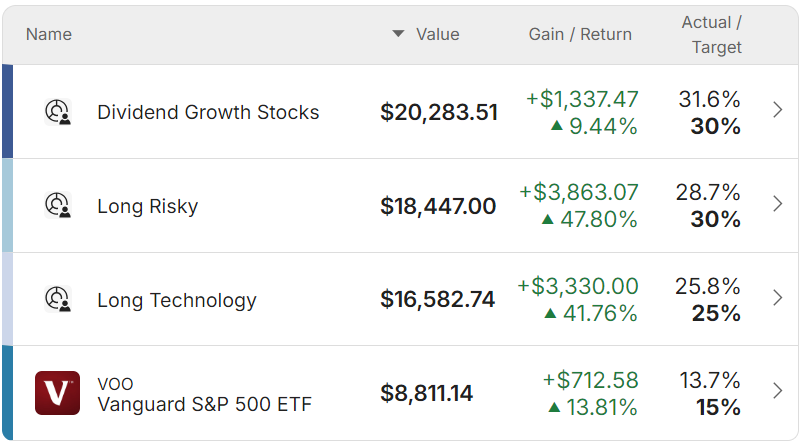

Beyond that, I’ll continue to deploy capital toward my Dividend Growth Portfolio shown above — especially into a few of the names we’ll talk about later in this post.

Week in Review — Too Long, Didn’t Read:

SentinelOne is flipping free cash flow positive next year, Broadcom guided to tens of billions in adj. EBITDA for 2024, Lululemon continues to take market share in the athleisure space, we gave a great heads-up on TLT, Jamie Dimon goes wild on Bitcoin, the Japanese carry trade could be coming to a close, labor market considerations, and an interesting insight into bank activity.

Key Earnings Announcements:

SentinelOne is flipping free cash flow positive next year, Broadcom guided to tens of billions in adj. EBITDA for 2024, and Lululemon continues to take market share in the athleisure space.

SentinelOne (S)

Key Metrics

Revenue: $164.2 million, an increase of +42% YoY

Operating Loss: -$81.4 million, compared to -$104.0 million last year

Net Loss: -$70.3 million, compared to -$98.3 million last year

Earnings Release Callout

“We delivered strong top-line growth and substantial margin expansion, showcasing the scale and breadth of our Singularity platform. Our gross margin reached a new record, and we achieved our ninth consecutive quarter of over 25 percentage points of year-over-year operating margin improvement.

Building on our third quarter outperformance, we are again raising our top and bottom line expectations for the fiscal year ‘24.”

Causing SentinelOne’s stock price to plummet as they were still focused on “growth” instead of “profitability.” However, this quarter’s earnings results were a tremendous step in the right direction — causing their stock price to climb +50% during the last 30-days alone.

SentinelOne shared three key takeaways during their earnings call —

1) This quarter was a clean beat against Wall Street’s annual recurring revenue (ARR) expectations while narrowing their EBIT loss.

2) 2024 net new annual recurring revenue (ARR) guidance is now north of $200M — which implies positive free cash flow during the second-half of 2024. This is a MAJOR milestone!

3) The company reported strong momentum and demand uplift in their emerging products — which means as they introduce new products over the coming 12-18 months their ARR is only set to grow.

As you all know, my favorite investing strategy is to buy names who are newly free cash flow positive or will be soon. SentinelOne is one of those names now. The market has baked in some of these expectations as their stock price has climbed +64% YTD — but if you’ve been dollar cost averaging into this name over the last several quarters like I have been, you’re likely in the green by now.

For perspective, I own ~50 shares at $15.96 per share — and will continue to expand my position into 2024 as I remain extremely excited about them flipped free cash flow positive and building upon this momentum in 2025 and 2026.

Broadcom (AVGO)

Key Metrics

Revenue: $9.3 billion, an increase of +5% YoY

Operating Income: $4.2 billion, an increase of +10% YoY

Profits: $3.5 billion, an increase of +7% YoY

Earnings Release Callout

“In fiscal year 2023 we achieved record adjusted EBITDA margin of 65%, generating $17.6 billion in free cash flow or 49% of revenue, demonstrating our stable and diversified business model.

With this transformational acquisition and expected increase in cash flows, we are increasing our quarterly common stock dividend by 14% to $5.25 per share for fiscal year 2024. The target fiscal 2024 annual common stock dividend of $21.00 per share is a record, and the thirteenth consecutive increase in annual dividends since we initiated dividends in fiscal 2011.

My Takeaway

I want each and every one of you to re-read the above statement — this is why we invest! Not only to realize the immense upside in stock price when companies succeed — but to also earn more each and every year through dividend payments as a loyal shareholder.

As you all might remember, Broadcom is the largest single-stock inside of the Dividend Growth section of my portfolio — and this is why!

Not only did I share with you all why I was so excited about the company in this post 6-months ago, but they made the cut originally because of their incredible history or paying and growing their dividend.

Their dividend just got hiked by a whopping +14% — that’s very exciting! Now on to the fundamental analysis…

While the company wasn’t able to duplicate the massive AI-levered upside Nvidia had reported last week, Broadcom’s management team delivered a very solid earnings report and gave encouraging guidance for 2024 — calling for $50B in revenue and $30B in EBITDA from their Semiconductor business segment, and $20B in revenue from their Infrastructure Software business segment.

More importantly, management noted they expect $8.5B in EBITDA from their VMware acquisition to be fully realized by the end of 2024 — two years ahead of schedule.

The company generated $4.8B in cash from operations, with $4.7B of that translating into free cash flow — representing 51% of total revenue generated during the quarter. That’s absolutely mind-boggling to think about — 51 cents of every dollar in revenue this company generates turns into cold hard cash in their bank account!

AI and ML related revenue accounted for $1.5B of their $9.3B quarterly revenue, and management continues to expect AI and ML to account for >25% of Semiconductor revenue in 2024 ($8B contribution).

I remain an excited dividend-focused shareholder of Broadcom.

Lululemon (LULU)

Key Metrics

Revenue: $2.2 billion, an increase of +19% YoY

Operating Income: $338.1 million, compared to $352.4 million last year

Profits: $248.7 million, compared to $255.5 million last year

Earnings Release Callout

“Our third quarter performance, which exceeded our expectations on the top- and bottom-line, reflects the ongoing strength of our business model and our teams' ability to successfully execute at a high level amid an uncertain macro environment.

As we look to the end of our fiscal year and into 2024, we remain focused on driving long-term growth and creating value for all our stakeholders.”

My Takeaway

As I’ve been saying for years now — Lululemon represents an increasingly established, yet still up and coming merchandising-led disruptor in the athleisure and apparel space. Their better-than-expected earnings results showcase their persistent underlying growth potential and resiliency.

Earnings per share grew +26% YoY as catalyzed by significant gross margin expansion (+220 bps to 58.1%) and better-than-expected expense management (-90 bps below guidance). Senior leadership indicated during the earnings call that Holiday 2023 is off to a great start, noting particularly strong traffic and demand trends through the Black Friday weekend.

Personally speaking, I actually knew a few guy friends who sought out Lululemon specifically during Black Friday to purchase their pants while on sale. Lululemon is now very much a male-focused apparel brand.

Ultimately, I believe Q4 is shaping up to be a solid quarter for the company as they continue to reap the benefits of strong demand (propping up gross margins) and SG&A deleverage. While Lululemon is trading at a premium to their peers, I think this is warranted considering their industry-leading growth (and market share gains) combined with consistent margin expansion.

I remain bullish on Lululemon and will be expanding my position in 2024.

Investor Events / Global Affairs:

We sniped bonds, Jamie Dimon wants to burn down Bitcoin, and Japan still looks so sketchy.

“We believe there’s significant opportunity in investing in long-term treasuries.”

Fast forward to present day — and bonds have had one of the best 4-6 week stretches in the last 50+ years.

Congrats to those that checked out TLT while it was at record lows, you’re likely up double-digits at this point. Stay tuned for more updates about bonds coming soon.

Jamie Dimon Rips Bitcoin

Source: Iev Radin / Shuttstock / Blockworks

Jamie Dimon — the CEO of JPMorgan Chase (JPM) — came out swinging at crypto last week. As the leader of the largest bank in the country, his words always carry a lot of weight.

“I’ve always been deeply opposed to crypto, bitcoin, etc…The only true use case for it is criminals, drug traffickers … money laundering, tax avoidance…

If I was the government, I’d close it down.”

During a time in which Wall Street is getting more and more comfortable with Bitcoin — it was quite a scene with Dimon sticking to his guns here. We’re excited to see where he stands on it all over the coming months.

Random but related…

Central banks are absolutely pouring money into gold. We wonder if Dimon has a vested interest in the success of gold and views Bitcoin as its primary competitor? Just a thought. Regardless — keep your eyes on gold and oil.

Warning Signs from Japan?

As we’ve discussed before — foreign exchange (“forex”) investors have thrived on predictable monetary policies, engaging in lucrative yen carry trades by borrowing yen at low rates and investing in higher-yielding assets.

This has been especially prominent with the yen-to-U.S. dollar carry trade. However, as central banks, particularly the Federal Reserve, signal a shift towards rate cuts — the stability of these carry trades is at risk.

The historically calm foreign exchange waters — marked by low volatility — are expected to change with Federal Reserve rate cuts and the probability of Japan raising rates.

See this link and this link for our previous writings on the Japanese carry trade.

Major Economic Events

Labor market results and keeping an eye on bank activity.

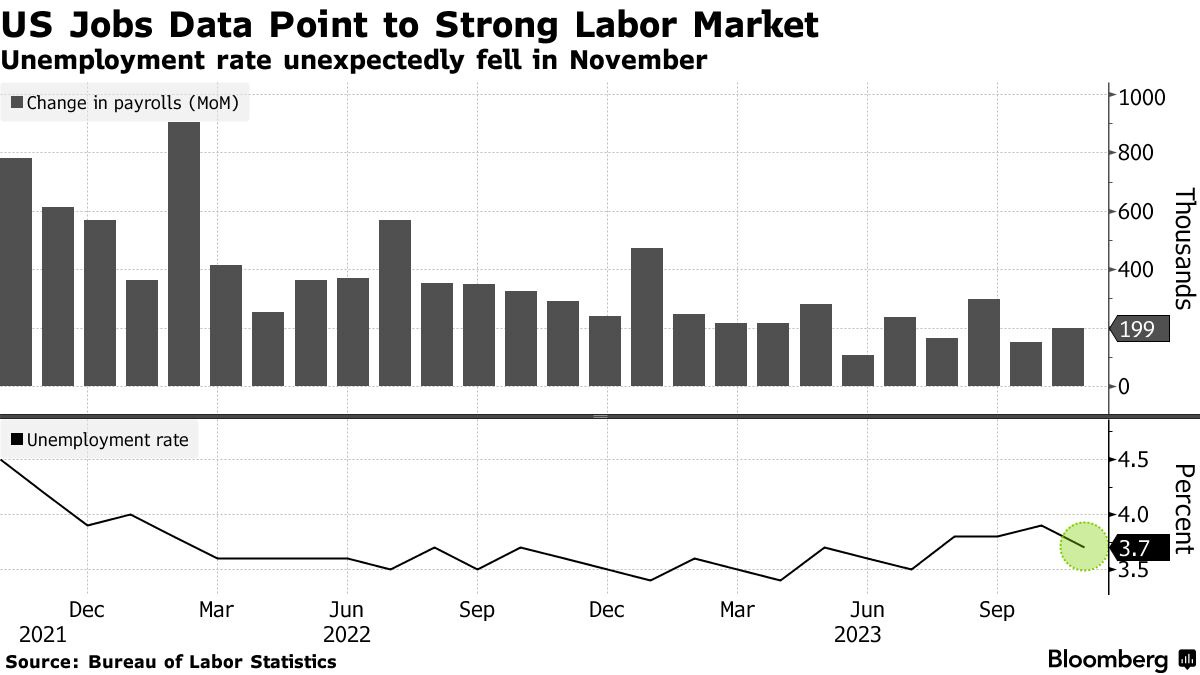

Jobs Report + Unemployment Rate

The U.S. labor market unexpectedly strengthened in November — with nonfarm payrolls rising by +199K, surpassing October's +150K increase.

The return of striking auto workers contributed an additional +30K jobs, and could have helped contribute to a decline in the unemployment rate to 3.7%.

Sectors such as health care, leisure, hospitality, and government hiring, along with the resolution of the United Auto Workers strike, fueled the payroll gains, contradicting expectations of a softer hiring pace.