👉 Week in Review: 12/03/23

👉 Week in Review: 12/03/23

We're up +$24,722 in 2023...

Happy Sunday.

Before we dive in — Rest in Peace to a legend! For those unfamiliar, Charlie Munger has been the right-hand man of Warren Buffett at Berkshire Hathaway for decades. His humor and wisdom will never be forgotten.

“You don’t have a lot of envy, you don’t have a lot of resentment, you don’t overspend your income, you stay cheerful in spite of your troubles, you deal with reliable people and you do what you’re supposed to do. All these simple rules work so well to make your life better.”

Portfolio Updates:

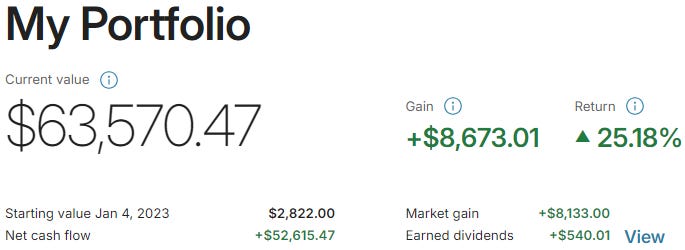

What an incredible year thus far — having deployed $98.8K across these two publicly-tracked accounts and having returned +$24.2K, a whopping 24.5% return.

This return is nearly double my “dollar cost averaged S&P 500 return.”

By that, I mean it’s nearly double the VOO +13.56% return shown above.

Of course, if I had deployed all $98.8K into the S&P 500 on January 3rd of 2023, I’d have received a +20% return YTD. However, that’s not how investing works — we invest small amounts of money throughout the entire year, changing our overall adjusted return profile.

Every time I invested into these accounts, I also invested into VOO — allowing me to track my “dollar cost averaged S&P 500 return.” By knowing this important figure, I’m able to more accurately benchmark my total adjusted return over time.

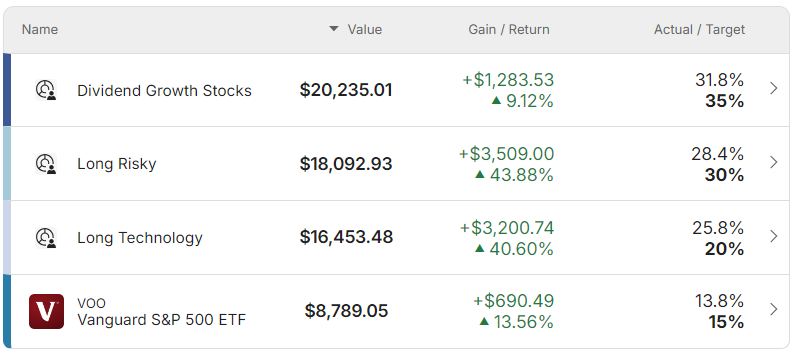

I will mention, an interesting observation is to see that the Risky section of the portfolio is now leading the pack — suggesting the names we chose (mainly those flipping profitable for the first time) are beginning to have value assigned to them by the markets.

Looking forward to 2024, I’ll continue to follow this strategy, as you can see it produced some incredible ideas this year — with cybersecurity being an awesome theme.

Both Palo Alto Networks and CrowdStrike were assigned some of the largest allocations in this section of the portfolio because I’m hellbent on the importance of cybersecurity — especially as AI continues to evolve.

Over the coming week or two, I’ll work on compiling a “biggest lessons learned” from the 2023 portfolio, as well as share new positions, updated weightings, and more.

Stay tuned!

Week in Review — Too Long, Didn’t Read:

Salesforce delivered a “cocktail” of positive news, Ulta is reinvesting into their business in 2024, Crowdstrike is on track to deliver $5B in ARR in 2026, McDonald’s introduces a new offering, the Cybertruck is here, Shein’s IPO is getting attention, Inflation data continues to improve, and construction spending reaches $2 trillion annually for the first time ever.

Key Earnings Announcements:

Salesforce delivered a “cocktail” of positive news, Ulta is reinvesting into their business in 2024, and Crowdstrike is on track to deliver $5B in ARR in 2026.

Salesforce (CRM)

Key Metrics

Revenue: $8.7 billion, an increase of +11% YoY

Operating Income: $1.5 billion, an increase of +226% YoY

Profits: $1.2 billion, an increase of +483% YoY

Earnings Release Callout

“We had another strong quarter of executing on our profitable growth plan we set in motion last year, delivering $8.7 billion in revenue and again raising our operating margin guidance for this fiscal year.

Over the last year we have transformed the company, enabling us to deliver another quarter of strong profitable growth with GAAP operating margin of 17.2% and non-GAAP operating margin of 31.2%.”

My Takeaway

WOW! What an incredible quarter reported by one of the largest software holdings in the portfolio.

As you all know, I’ve been incredibly bullish on Salesforce — even since late-2022. I rebalanced my portfolio to lean a bit out of CRM and instead heavier into AMZN — but now I’m kicking myself for doing that! Haha.

What’s important to consider when reviewing software company earnings is not just their revenue growth, but also the growth (or lack thereof) of their Remaining Performance Obligations (RPOs). Essentially, this is the revenue they’ve “not yet earned” in the eyes of the generally accepted accounting principles (GAAP). It’s a technicality — but gives us a glimpse into next quarter’s potential revenue.

CRM not only reported solid revenue growth of +10% during the quarter, but also reported RPO of +13% — hinting toward and even better quarter is just around the corner (Q4).

Comments from management during the earnings call were constructive — identifying green shoots while also recognizing the reality of a slowing economy. Impressively, deals worth over $1M saw an +80% increase YoY — driven by what their CEO called a “cocktail” of multi-cloud adoption.

AI has also garnered meaningful customer interest, now with 17% of their Fortune 100 customers using Einstein GPT.

I remain incredibly bullish on Salesforce.

Ulta Beauty (ULTA)

Key Metrics

Revenue: $2.5 billion, an increase of +6% YoY

Operating Income: $327.3 million, compared to $361.9 million last year

Profits: $249.5 million, compared to $274.6 million last year

Earnings Release Callout

“Our traffic trends remained healthy, our brand awareness increased, and we expanded our loyalty program to a record 42.2 million members.

As we look to the future, the outlook for the Beauty category is bright, and I am confident Ulta Beauty has the right plans in place to delight our guests this holiday season, expand our leadership position in specialty beauty retail, and deliver long-term shareholder growth.”

My Takeaway

This quarter’s earnings results had two main standouts to acknowledge:

Gross margin strength, despite a normalization in promotional activity.

Management’s initial 2024 framework — including +4% same-store sales growth and a 15% operating margin.

Performance this quarter was driven primarily by skincare — led by new brands and continued innovation in existing brands — as well as services. Specifically, in-store engagement such as haircuts, blowouts, makeup, and ear piercings.

Looking ahead, the company is on-track to deliver a laundry list of transformational projects in 2024 — including the transition of their digital store. In my opinion, these investments will continue to eat away at their bottom line — with benefits not taking place likely until 2025 / 2026.

To me, 2024 seems like a constructive year for Ulta Beauty. Because of this, I don’t plan to open a position anytime soon.

CrowdStrike (CRWD)

Key Metrics

Revenue: $786.0 million, an increase of +35% YoY

Operating Income: $3.2 million, compared to -$56.4 million last year

Profits: $26.7 million, compared to -$54.6 million last year

Earnings Release Callout

“CrowdStrike’s record third quarter exceeded expectations, delivering new milestones across the business: net new ARR growth accelerated to a record $223 million and ending ARR surpassed $3 billion.

Our single platform architecture and unique data advantage unites security and I.T. teams in solving cybersecurity’s mission-critical challenges, driving increased win rates and record pipeline.”

My Takeaway