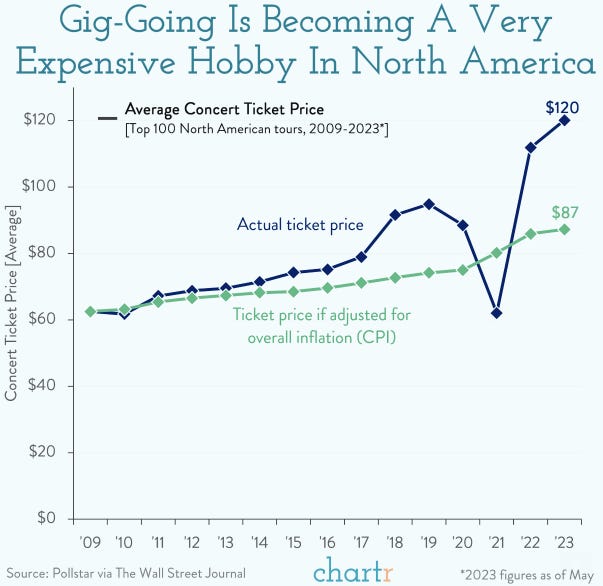

We often start out these Week in Review editions with profound research or big-time callouts. This time, we just want to ask one question — WHEN did ticket prices to pretty much ANYTHING skyrocket?

Is it because the pandemic made us appreciate live events more? Are sports and concerts simply becoming more in demand? Is Taylor Swift just the greatest individual economic driver that the world has ever seen?

This has gotten out of hand!

Portfolio Updates:

Above are screenshots of the updated portfolio values. This month has been a slower month for me from a capital deployment perspective, so I’ve only invested $5,000 into the markets — and all $5,000 of that went to purchasing Chainlink (LINK).

As you all know, Chainlink (LINK) is the largest cryptocurrency I have. It’s not displayed above because of that reason + I keep the tokens offline in a cold wallet. The price of Chainlink is up +53% since reminding you all about my position in this July post.

As it relates to the stock portfolio, I owe you all an update watchlist / breakdown. I’ve been traveling for work throughout the last two weeks, leaving me little time to sit down and conduct updated research.

Expect an update this week!

Week in Review — Too Long, Didn’t Read:

Tesla reported a “disaster quarter,” Netflix delivers an all-around solid quarter with updated FCF guidance, American Express is on track to report +15% growth in 2023, China export drama causes chip stocks to slide, yields fly after Powell’s speech and Retail Sales come in stronger than expected, Congress can’t choose a Speaker of the House, the Leading Economic Index (LEI) projects a not-so-fun first half of 2024, and Existing Home Sales are down more than -15% since last year.

Key Earnings Announcements:

Tesla reports a “disaster quarter,” Netflix delivers an all-around solid quarter with updated FCF guidance, and American Express is on track to report +15% growth in 2023.

Tesla (TSLA)

Key Metrics

Revenue: $23.3 billion, an increase of +9% YoY

Operating Income: $1.8 billion, compared to $3.7 billion last year

Profits: $1.8 billion, compared to $3.3 billion last year

Earnings Release Callout

“Our main objectives remained unchanged in Q3-2023: reducing cost per vehicle, free cash flow generation while maximizing delivery volumes and continued investment in AI and other growth projects.”

My Takeaway

There’s a lot to breakdown here.

First, Elon’s comments surrounding his macroeconomic concerns — essentially Elon Musk’s excuse for such a slow growth quarter are high interest rates. As long as interest rates remain this high, the everyday customer won’t be able to afford to purchase a new car from Tesla. To combat this dilemma, Tesla has continued to lower the price of their cars — eating into their operating margins (down -10% YoY). This isn’t good in the near-term.

Second, the company has rapidly increased (+58% QoQ) their amount of money spent on research and development for their AI. The company’s AI capabilities have a massive impact of their market cap — so when / how the company decides to leverage this technology will be a massive determining factor going forward.

Third, Cybertruck on-ramp and cash flow concerns. Management mentioned how incredibly difficult it has been to create and scale the Cybertruck — specifically mentioning how they’re building a completely new product from scratch. They mentioned how it will take several years for this product to reach profitability.

As a shareholder, I believe this recent “mini disaster” of a quarter is an incredibly buying opportunity. It’s freaking Tesla! Their products are here to stay. If you already own shares of the stock like I do, consider selling covered calls against your position to essentially lower your cost basis. I’ve been able to lower by cost basis from $262 / share down to $238 / share over the last two months doing this.

Netflix (NFLX)

Key Metrics

Revenue: $8.5 billion, an increase of +8% YoY

Operating Income: $1.9 billion, an increase of +25% YoY

Profits: $1.7 billion, an increase of +20% YoY

Earnings Release Callout

“Our primary financial metrics are revenue for growth and operating margin for profitability. Our goal is to accelerate revenue growth, expand operating margin and deliver growing free cash flow. Nine months through the year, we are well positioned to meet these objectives in 2023.”

My Takeaway

Commentary during the earning call skewed very positive — retention metrics continued to hold up as the paid sharing rollout broadened, with better-than-expected churn and solid subscriber conversion leading to revenue lifts across markets.

However, the SAG-AFTRA strike still looms over 2024 content plans and has contributed to near-term free cash flow volatility — but the company’s Q4 2023 content slate is still shaping up to be strong. Long-term free cash flow outlook remains unchanged.

Netflix added +8.76M members in Q3, which outpaced estimates by more than 2 million — mainly driven higher in the EMEA region of the world. Netflix still expects a multi-quarter member tailwind from their password sharing efforts, which is why Wall Street is forecasting +18M more members in 2024.

The company raised their 2023 FCF guidance to at least $13B as the impact of the WGA and still-ongoing SAG-AFTRA strikes reduced spend during the period. The company is hoping to generate $17B in FCF in 2024 assuming a more normalized strike environment.

I believe a lot of these near-term headwinds (strikes in particular) are overblown. This quarter demonstrated the underlying thesis remains in-tact and that there’s something to like for everyone — share buybacks, stable content spend, free cash flow, double-digit growth. I remain a bullish shareholder.