Instagram is developing a text-based app to compete with Twitter, according to sources (1 | 2). Apparently — the company has been secretly testing the app idea with a small group of celebrities and influencers for feedback. While select creators have been in discussions about the project, none have had access to the full version of the app.

The new app, separate from Instagram but allowing account connections, is expected to launch as early as June. It may also be compatible with other Twitter competitor apps, including Mastodon. Meta Platforms hasn’t made an official statement on the matter, but we’re very interested to see where things head from here.

Meta Platforms (META) Stock Performance, YTD Chart

A somewhat odd addition from Bloomberg — “The Mumbai-based news site Moneycontrol.com reported Meta was exploring plans for a text-based app in March, saying it had the internal code name P92. Others have reported the code name Barcelona.”

Portfolio Updates: (+9% YTD)

Quick reminder to check in on the Portfolio Tracker every once and a while.

As you all might remember, I’ve opened new positions in:

Napco Security Technologies (NSSC)

Uber Technologies (UBER)

Mastercard (MA)

On Holdings (ONON)

Analog Devices (ADI)

To reflect upon the returns of our positions YTD, it’s awesome to see so many companies having exceeded +20% already. I’m eager to see how these names continue to perform throughout 2023 and 2024.

With that being said, we’ve certainly experienced our ups and downs.

My position in PayPal is down -20%. I saw this incredibly well-researched video by QuiverQuant that hypothesized why their stock has experienced such a deep decline YTD — and it makes a ton of sense.

Over the coming week, I’m going to begin really dialing in on the positions I want to remain invested into as we head into the back-half of the year.

Remember, countless economists and “experts” have been calling for a recession to officially begin in Q3 / Q4 — how will that impact the companies in your portfolio?

Eager to share what I find!

Week in Review — Too Long, Didn’t Read:

Monday.com reported record free cash flow, Home Depot remains an exciting idea, On Cloud raises their full-year guidance, Hedge Funds unloaded plenty of Apple (AAPL) and picked up plenty of Pfizer (PFE), Google is tripling-down on A.I., Shipping in the United States may be in better shape than meets the eye, Leading Economic Indicators (LEI) continue to flash red, Fed officials are looking more hawkish over the last couple of weeks, and Existing Home Sales display the mixed-bag situation in the housing market.

Key Earnings Announcements:

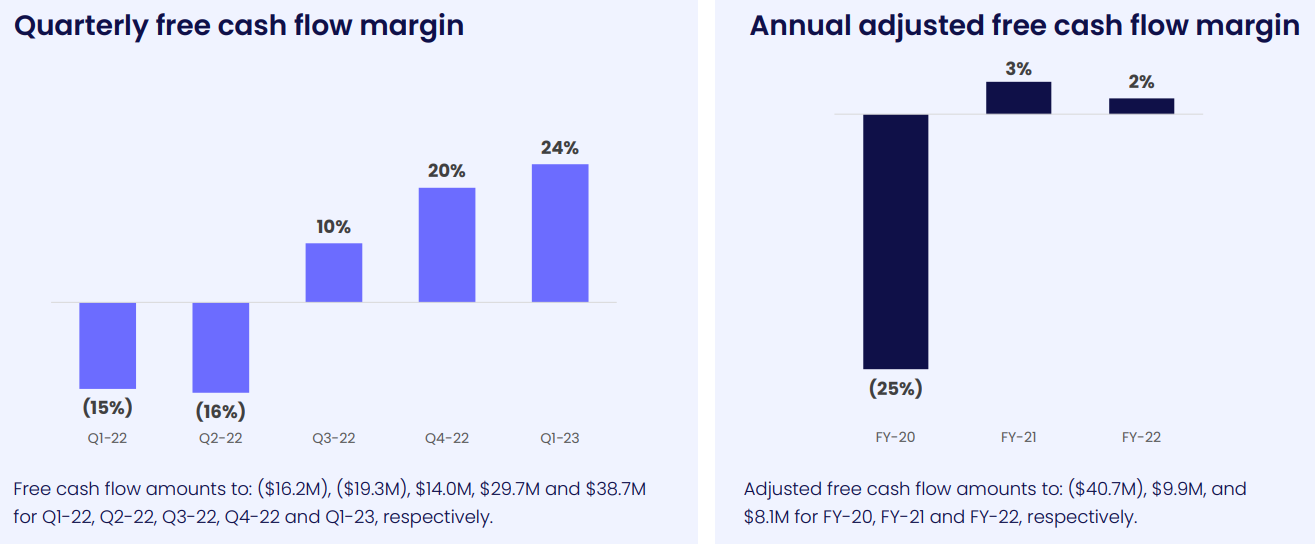

Monday.com reports record free cash flow, Home Depot remains an exciting idea, and On Cloud raises their full-year guidance.

Monday.com (MNDY)

Key Metrics

Revenue: $162.3 million, an increase of +50% YoY

Operating Loss: -$22.8 million, compared to -$67.5 million last year

Net Loss: -$14.7 million, compared to -$66.7 million last year

Earnings Release Callout

“We are very pleased with our results in Q1, achieving quarterly records for our free cash flow and revenue. As a result, we are increasing our full-year guidance, and now expect to achieve non-GAAP operating profitability in FY’23, two years ahead of our prior expectations.”

My Takeaway

LET’S GO!

This is exactly what we’ve been talking about for the last 12-18 months now — finding and investing aggressively into companies who are 1) going to eventually benefit from economies of scale and 2) flipping free cash flow / operating income positive in the immediate term.

Monday.com was highlighted a few times over the last 9 months (here where I spoke about my excitement for them to flip FCF positive in 2023, and more recently here where I reaffirmed my excitement regarding their cash flow expectations).

The company reported record free cash flow, guided to positive operating income two years ahead of original expectations, and their number of customers spending >$50K / year with them is growing like wild fire.

In my previous analysis I stated “I don’t think this stock will continue rocketing higher in the near-term, but instead slowly grind higher quarter after quarter,” and that’s exactly what’s happening.

It’s not too late with this one, and I’m eager to continue dollar cost averaging into a larger and larger position over the coming quarters and years.

Home Depot (HD)

Key Metrics

Revenue: $37.2 billion, compared to $38.9 billion last year

Operating Income: $5.6 billion, compared to $5.9 billion last year

Profits: $3.9 billion, compared to $4.2 billion last year

Earnings Release Callout

"After a three-year period of unprecedented growth for our sector, during which we grew sales by over $47 billion, we expected that fiscal 2023 would be a year of moderation for the home improvement market.

Our sales for the quarter were below our expectations primarily driven by lumber deflation and unfavorable weather, particularly in our Western division as extreme weather in California disproportionately impacted our results.”

My Takeaway

It’s obvious Home Depot has seen a rough start to the year, but that was to be expected. All of 2022, existing home sales as well as new construction builds were on the decline — this company’s bread and butter.

With that being said, their reasons causing a drag on their profits this year is transitory (weather and lumber prices) — which means over the next 12-24 months the company’s stock price should experience a healthy rebound.

Management has done an incredible job offsetting softer-than-expected sales with effective cost control measures — which should result in 2023 EPS of ~$16 or so.

Let me be very clear — the market is forward-looking, and this company’s next 12-24 months will be met with volatility. I believe Home Depot’s stock price could fall another -10-15% depending on their sales.

With that being said, zoom out. Home Depot, alongside Lowe’s, has the home improvement category in a chokehold, and will continue to do well over the coming decade. I’m eager to purchase more shares in the $220-250 range.

If you’re a fellow shareholder, brace for impact. This volatility is just getting started.

On Holdings (ONON) — reported in CHF

Key Metrics

Revenue: $420.2 million, an increase of +78% YoY

Operating Income: $42.3 million, an increase of +1,144% YoY

Profits: $44.4 million, an increase of +210% YoY

Earnings Release Callout

“On starts the year with another record net sales quarter ahead of expectations. On delivers a first quarter gross profit margin of 58.3%, up from 51.8% in the prior year period, reflecting the normalized supply chain environment and the resulting discontinuation of exceptional air freight usage, which had weighed on profitability during the first quarter of 2022.

On's strong order book for the second half of the year, driven by existing and exciting upcoming product launches are increasing the confidence of On in its growth aspirations for 2023. On is therefore raising its outlook for the full fiscal year 2023 to reach at least CHF 1.74 billion.”