👉 Week in Review: 03/26/23

👉 Week in Review: 03/26/23

+13% upside "guaranteed."

“First, the Fed, Treasury and FDIC should come to terms with — and agree on — the breadth of the problem.

It’s not about a few troubled banks and an irrational run by panicky depositors. Weekend fire-fighting only buys time. The liquidity-induced holiday from economic history has ended.

They should be prepared for a pullback of everything everywhere all at once.”

If that terrifying quote from a former Fed official isn’t enough to get your attention, see below from Morgan Stanley (via Carl Quintanilla):

What happens when one or more of these five things are happening?

S&P 500 forward earnings guidance declining.

Yield curve inverted.

Unemployment below average.

Manufacturing PMIs < 50.

40%+ of banks tightening lending standards.

“All five are in place today, which is rare.”

This post is all about catching you up on the most important (or underrated) callouts from the market — hopefully showing you that the grim outlook is something to embrace and plan toward.

Let’s jump in!

Portfolio Updates:

I just updated all of the tracking data for the 46 positions listed in our Portfolio Tracker (paying subscribers only) — including the Quantbase Dividend Growth Strategy.

Here are a few big takeaways to keep in mind..

Dividend growth stocks remain 50% weighting in my portfolio — this is because I’m a firm believer that over the coming 9-24 months we’ll see immense volatility in the markets, giving us an opportunity to own quality cash-flowing companies at reasonable prices. We’ve already begun to accumulate shares in companies like Lowe’s, Home Depot, Visa, and Union Pacific at deep discounts.

Long-term technology remains my second largest category — think Apple, Salesforce, Microsoft, Tesla, and others. This is because it’s obvious technology is eating the world, and I want to ensure I have meaningful exposure to these types of long-term compounders. Google and Amazon specifically are poised to see immense share price appreciation over the coming years (see graphs below).

I’m still allocating meaningful capital toward various technology companies — think Palo Alto Networks, Hims & Hers Health, Monday.com, and Crowdstrike. As stated here, I’m a big believer in the investing strategy of “positive / nearly positive operating and free cash flow.” This strategy allows me to double down on companies who have proven to be self-sustaining compounders.

New Positions on the Horizon:

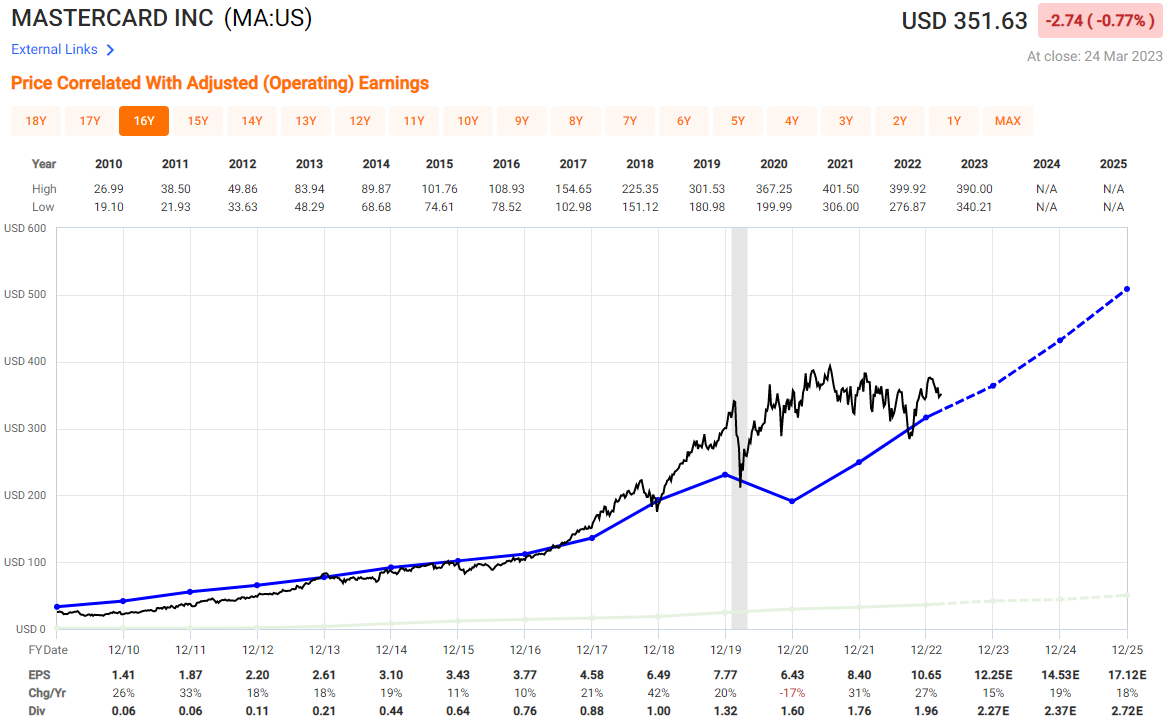

Mastercard (MA) — again, I love buying shares of proven companies at reasonable prices. Mastercard is operating alongside Visa in an oligopoly, is slated to grow their earnings per share by +15%, +19%, and +18% over the coming three years, and their 5-year dividend compounded annual growth rate is over +17.5%. Their stock price has also begun to align better with their earnings — you can see the “bubble” their stock traded in during 2020 & 2021. The black line (stock price) is now much closer to the blue line (earnings per share).

Free Money?

You all might remember this post from several months back — walking you all through a “merger arbitrage” opportunity between Microsoft and Activision Blizzard.

Shared earlier this week from the UK Government was the following statement:

“The [Competition and Markets Authority] has provisionally concluded that the anticipated acquisition by Microsoft Corporation of Activision Blizzard, Inc. will not result in a substantial lessening of competition in relation to console gaming in the UK.”

This means the merger / acquisition is much more likely to receive the “greenlight” from regulators — leaving a +13% upside opportunity for anyone that owns shares of Activision Blizzard as of market close on Friday.

I remain confident this deal will close — as does Citi bank — having just raised their likelihood from 50% to 70% as shared here.

If you want the opportunity to earn a “guaranteed” ~13% return on your money, buy stock in ATVI for $84 / share and let Microsoft buy it from you for $95 / share in the coming months.

Week in Review — Too Long, Didn’t Read:

Nike is taking their “markdown medicine,” On Holding’s growth story is far from over, Presidents Putin and Xi seem to have a historic plan in movement, Cash App gets wrecked with fraud and fake account claims, Amazon lays off thousands of more employees, Coinbase gets a late Valentine from the SEC, the Fed’s rate decision, Jerome Powell’s brutal body language, the Fed’s balance sheet sees massive expansion after months of contraction, and a brief Housing Market update.

Key Earnings Announcements:

Nike is taking their “markdown medicine,” and On Holding’s growth story is far from over..

Nike (NKE)

Key Metrics

Revenue: $12.4 billion, an increase of +14% YoY

Operating Income: $1.5 billion, compared to $1.7 billion last year

Profits: $1.2 billion, compared to $1.4 billion last year

Earnings Release Callout

“Fueled by compelling product innovation, deep relationships with consumers and a digital advantage that fuels brand momentum, our proven playbook allows us to navigate volatility as we create value and drive long-term growth.”

My Takeaway

Strength was once again broad-based in nature, except for China. To right-size their inventory, Nike is taking their “markdown medicine,” which is hurting their gross profit margins — while catalyzing sales growth in their Direct and Wholesale channels.

However, this should allow inventory levels to be healthy as they exit next quarter.

In my opinion, the companies clearest drivers of revenue over the coming quarter are: 1) ongoing inventory mix shift toward Direct as the company continues to move toward their 60% penetration steady-state, 2) accelerating revenue growth in China, 3) higher average selling prices, and 4) new products surrounding their Airmax franchise + women’s clothing.

Personally, I don’t see a reason to allocate capital toward Nike at the moment — sure, the company is bouncing back from a rough 2022 but given there’s no clear “catalyst” around the corner to move the stock price higher I’m on the sidelines.

On Holding (ONON)

Key Metrics — reported in Swiss Franc

Revenue: $366.8 million, an increase of +92% YoY

Operating Loss: -$24.4 million, compared to -$191.0 million last year

Net Loss: -$26.4 million, compared to -$187.0 million last year

Earnings Release Callout

“After navigating through a challenging 2022, including supply shortages, tight production capacities and disruption of global trade lanes, we are looking forward to a great year with largely normalized operations.

We have made significant progress in many areas in the 18 months since our IPO, which will set us up for ongoing success and market share gains.”

My Takeaway

This is interesting! I’ve heard of the company and their products, but I’ve never really taken the time to dive deep into their business model + financials.

Here’s what I took away from their recent earnings:

Their +92% YoY increase in revenue was achieved with no increase to marketing spend — which means strong word of mouth and existing customers are coming back to purchase new products.

New products accounted for 65% of the revenue generated during the quarter — with pre-orders of their Cloudmonster, Cloudgo, and Cloudrunner products up +80% YoY.

Wholesale expansion is well under way — with 9,200 doors now selling their products, including Foot Locker, Dick’s Sporting Goods, and Fleet Feet (up from only 8,000 last year).

This company’s growth story is far from over — and I’ll definitely be along for the ride. I don’t have a position in ONON just yet, but I’ll be sure to share a deep dive on the company with you all very soon. I’m really liking what I’m seeing re: diversified growth, product endorsement, geography momentum, etc.

And, of course, our friend Chris Camillo saw this +85% run YTD coming a mile away.. be sure to follow him on Twitter and YouTube.

Investor Events / Global Affairs:

The decline of the Western World’s reign, Cash App gets called out in a big way, Amazon adds to their already-high layoff tally, and Coinbase gets an SEC notice.