Obligatory Fun Fact: A living president cannot have their face on money. This rule was created to show that the US was not a monarchy — because living kings and queens are often printed on money in other countries.

👉 Win a Free Airbnb Vacation:

As you’re well aware, I’m always looking for ways to provide you all value. Well, this time it comes in the form of a weekend trip to a cabin in Gatlinburg, TN.

My best friend from college just purchased this property with the intention of it becoming a short-term rental on Airbnb. To help kickstart his journey, I told him I’ll purchase a weekend stay and give it away to one of our Rate of Return subscribers.

The weekend stay is worth ~$600 and I’ll cover the entire cost for you — all you and your partner have to do is show up and enjoy yourselves.

How to Enter:

Share Rate of Return with a friend — post a link of our publication to your social media, send it to your work colleague, or whatever you want!

Reply to this email with some sort of proof — this could be a screenshot, the friend’s email address, or anything in between.

I want to make winning this weekend cabin stay as easy as possible — so be sure to enter and send us your proof and we’ll add your name to the prize pool!

Also, if you’re looking for a cozy weekend cabin stay with you partner — consider booking Jacob’s property! It would mean a lot to me.

Goal Posts Keep Moving:

For months now, the S&P 500 has traded within +/- 10% of “fair value.”

Currently hovering around 4,080 — the S&P is now back to being ~10% overvalued based on forward earnings and interest rates.

So essentially, buyers of the S&P 500 today are banking on one of the following:

Lower interest rates than currently expected — The general expectation is a terminal fed funds rate between 5.25%-5.5%. (link)

Higher earnings growth than expected — The forward 12-month P/E ratio is 17.8, which is below the 5-year average (18.5) but above the 10-year average (17.2).

Analysts expect earnings declines for the first half of 2023, but earnings growth for the second half of 2023. For Q1 2023 and Q2 2023, analysts are projecting earnings declines of -3.0% and -2.4%, respectively. For Q3 2023 and Q4 2023, analysts are projecting earnings growth of +3.7% and +10.3%, respectively. For all of CY 2023, analysts predict earnings growth of +3.4%. (link)

Higher multiple expansion vs. historical performance — particularly during recessionary times. As of the end of January, Raymond James forecasted multiple expansion across the S&P 500 due to the prospect of reduced inflation, with price increases moderating back to ~3%; a consequent slowdown in interest rates, as higher rates will not be needed to combat increasing prices; and a Fed shift to just two further increases in the funds rate, ceasing in March. This was accompanied by a prediction of the S&P reaching 4,400 by year’s end. (link)

Positive Thoughts:

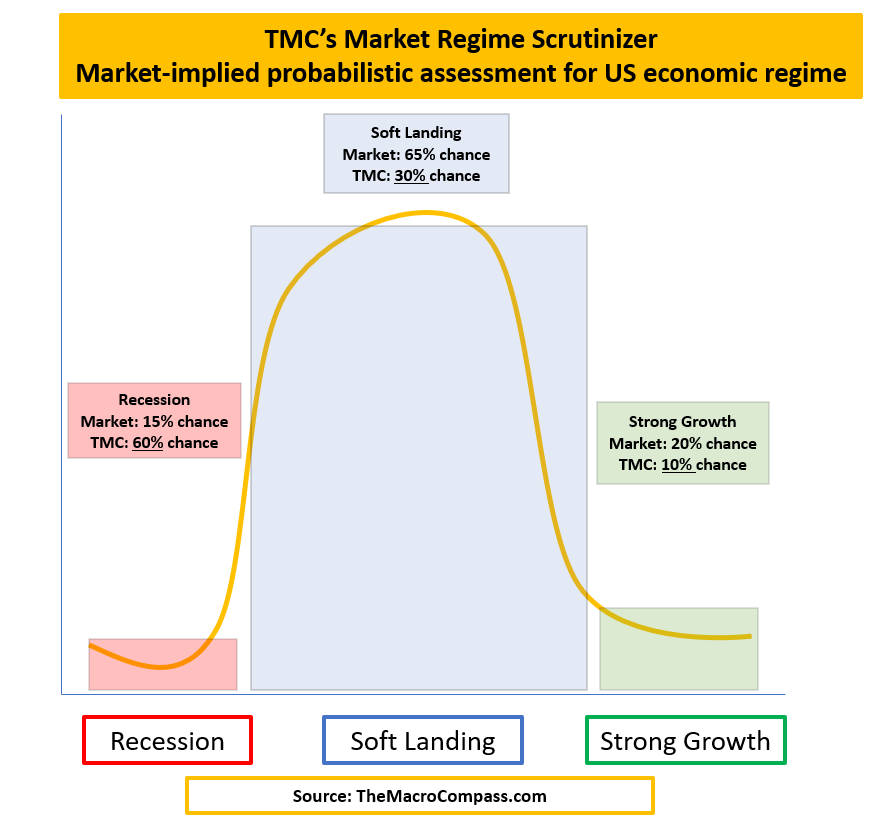

As you can see above, the market is pricing in an about a 1-in-5 chance of a recession being declared by the NBER. Positive thoughts are clearly infectious.

Folks, like us and The Macro Compass, see a much higher likelihood.

Last week I sat down with the folks from NEOS Investments to talk about their three ETFs — $SPYI, $BNDI, and $CSHI.

Their ETFs are built for those looking to produce income with their investment portfolio — they achieve this by buying / selling options against their holdings.

To learn more about their ETFs, please watch / listen to the podcast episode below!

Airbnb reports their first profitable year since inception, Monday.com is experiencing wonderful economies of scale, Palantir commits to profitability, Apollo Global Managements “no landing” viewpoint, the majority of Americans can’t pay for an emergency, inflation breakdowns for consumers and producers, and one of our favorite recession gauges from The Conference Board.

Key Earnings Announcements:

Airbnb reports their first profitable year since inception, Monday.com is experiencing wonderful economies of scale, and Palantir commits to profitability.

Airbnb (ABNB)

Key Metrics

Gross Booking Value: $13.5 billion, an increase of +20% YoY

Revenue: $1.9 billion, an increase of +24% YoY

Adj. EBITDA: $506.0 million, an increase of +52% YoY

Profits: $319.0 million, an increase of +480% YoY

Earnings Release Callout

“Looking forward to 2023, we’re seeing strong demand in Q1, indicating that consumer confidence to travel remains high.

This year, we’re focusing on three strategic priorities: making hosting mainstream, perfecting the core service, and expanding beyond the core.”

My Takeaway

2022 marks the first calendar year of profitability for Airbnb since their inception in 2008 — and 2023 is looking to be just as bright. The company’s management team claimed Q1 2023 nights and experiences booked has been “nearly as strong” as Q4 — which came in at +20% growth.

However, bearish analysts claim that for Airbnb to remain growing their “nights and experiences” by double digits annually, total supply of locations need to continue ramping up. Throughout 2022, Airbnb added +900K more locations around the world — totaling 6.6M globally. Most analysts believe the “supply side” of the equation will work itself out — the demand side is the main concern.

Personally, I don’t own Airbnb.

Don’t get me wrong — there’s a lot to be excited about. Supply growth acceleration, steady margins heading into 2023, continued cross-border travel recovery, and strong free cash flow.

But there are a handful of concerns that keep me on the sidelines at $130 / share — the Q1 2023 bookings momentum they’ve seen is likely to decelerate throughout the year, management expects long-term stays to decline substantially in 2023 (accounted for 21% of bookings in 2022), as well as their average daily rate.

I’m optimistic for Airbnb and I like the company — I just want to see how things shake out from an economic perspective over the coming months before jumping in.

Monday.com (MNDY)

Key Metrics

Revenue: $150.0 million, an increase of +57% YoY

Operating Loss: -$10.1 million, compared to -$31.6 million last year

Net Loss: -$1.4 million, compared to -$32.6 million last year

Earnings Release Callout

“Q4 capped off an amazing year, exceeding our expectations on both the top and bottom lines. We finished FY’22 with strong revenue growth, improving efficiency, and positive free cash flow for the second consecutive year. Despite macro uncertainties, we believe we are well positioned for the road ahead.”

My Takeaway

I do, however, own Monday.com — and couldn’t be happier about their recent earnings report! Before we dive deeper into the numbers — take a look above at how much their operating loss and net loss has improved.

The company also delivered their first quarter of positive adjusted operating profit!

In 2022, MNDY added +34,000 net new customers — resulting in a +69% increase in annual revenue. MNDY’s total customer count is now >186K, an annual increase of +22%. This is especially important to mention because despite experiencing only +22% growth in customer count — the company grew revenue by +69%.

This means MNDY is upselling their existing customers again and again on new products — letting economies of scale do its thing.

Looking forward, MNDY is guiding to +33% growth in 2023 — which comes with an improved operating margin. However, this also likely comes with moderate deceleration in net new customers paying >$50K / year as enterprises continue to pullback their operational spend.

Why I’m excited for their future: solid enterprise customer growth, overall dollar-based net retention rates holding steady amid broad spending pullback, healthy new customer pipeline, and their CRM product is expanding to existing customers in mid-2023.

They’re also guiding to positive free cash flow in 2023, and sustainable profitability by 2025. I’m a shareholder and I’ll continue to dollar cost average into my position. Right now the position hovers around 2% of total portfolio weighting.

Palantir (PLTR)

Key Metrics

Revenue: $508.6 million, an increase of +18% YoY

Operating Loss: -$17.8 million, compared to -$58.9 million last year

Profits: $33.4 million, compared to a loss of -$156.2 million last year

Earnings Release Callout

“In Q4 2022, we earned a profit of $31 million. A threshold has been crossed, and this is the start of our next chapter.

We expect to generate a profit for the current fiscal year, our first profitable year in the history of our company.”

My Takeaway

Well, Palantir was indeed profitable during the quarter — however, their profitability came from “interest income,” and “other income.” Despite the profitability, they still reported an operating loss of -$17.8 million during the quarter.

However, as stated above and during the earnings call — their CEO told us profitability is their new identity and they will remain profitable throughout 2023 and beyond. In my opinion, the only way they’ll be able to achieve this is by slimming down stock-based compensation and continually managing R&D effectively.

Don’t get me wrong — GAAP profitability is great and there are a ton of reasons to be excited about Palantir right now. However, I’m a bit worried about the slowing growth — having guided to only +15% in 2023.

Rewind 18 months and you all might remember they were telling us they’ll be growing at +30% compounded annually through 2025. I suppose it’s a trade off since they were also telling us they had no plans to be profitable until 2025.

This quarter they weren’t only GAAP profitable, but also reported the 8th consecutive quarter of positive operating cash flow and the 2nd consecutive quarter of positive free cash flow.

No position.

Investor Events / Global Affairs:

A PE firm with over half a trillion in AUM sees no landing (for now), and more than half of Americans can’t afford a $1000 emergency expense.