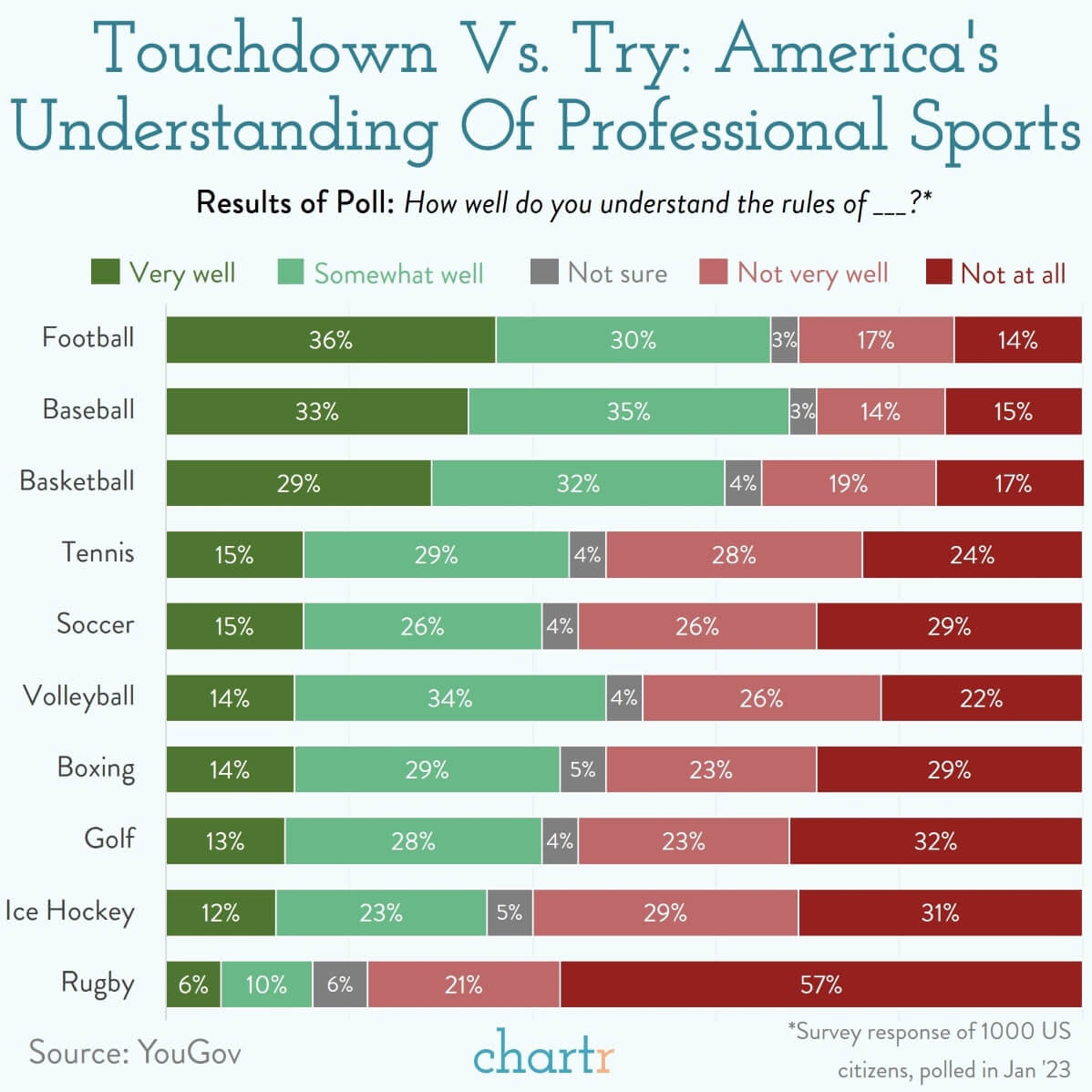

The annually most watched TV event in the United States has returned. If you don’t fully understand the rules of the game — don’t worry.

At least a third of Americans don’t either according to the data below:

Even if you’re not very captivated by American football, let’s not forget about the show-within-the-show: advertising.

Alcohol ads are in focus this year, as Anheuser Busch (BUD) backed away from its long-running exclusivity rights to promote the alcohol category. The likes of Molson Coors (TAP), Heineken (OTC — HEINY), Remy Cointreau (OTC — REMYY), and Diageo (DEO) will be showing off their booze to the masses.

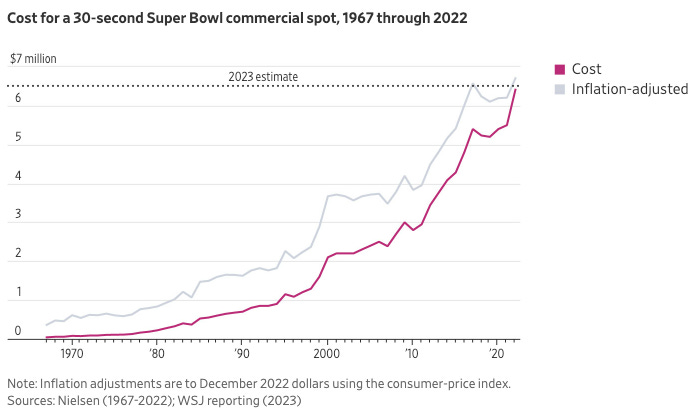

Fox (FOX) announced that it had sold out of advertising for its Super Bowl broadcast, with some 30-second slots selling for more than $7 million. Others sold for closer to $6 million due to multiyear deals or the purchasing of multiple ad slots. The company expects to gross $600 million in ad revenue from Super Bowl coverage.

Forget the football — bring on the halftime show!

Rhianna hasn’t released a studio album since 2016 and hasn’t performed on stage since the 2018 Grammys — so it was shocking when she was announced as the headliner for the Super Bowl LVII Halftime Show.

What you may not have realized… she’s been spending her time becoming a first-time mother and the richest musician in the world.

By taking on acting roles and launching businesses — Rhianna’s net worth is expected to be as high as $1.7 billion. At least $1 billion of this fortune is expected to come from her beauty brand called Fenty and her lingerie brand called Savage x Fenty.

And yes… her beauty brand has been selling football-branded makeup kits for passionate fans that want to get dolled up before watching her halftime show:

So she’s being paid millions for her performance, right?

Wrong.

Super Bowl halftime performers actually don’t get paid much at all.

According to a representative from the NFL, the league “covers all costs associated with the show and does pay the halftime performers’ union scale.” According to Forbes, the union scale is “a fraction of the six- and seven-figure sums" that artists of Rhianna’s caliber would typically be paid.

It’s no wonder why The Weeknd holds the most-ever streamed track in Spotify history — he was the lone 2021 halftime performer.

Rhianna is hoping for a revival of many of her hit tracks in the rankings, and is preparing for an absolute deluge of online purchases for her brands.

She’s unlikely to relinquish her title as the richest musician in the world after Sunday evening.

Portfolio Updates:

Quick question — would you all like to also be able to copy the trades I’m making inside of the Portfolio Tracker, similar to how you’re investing alongside me on Quantbase?

I’m working with a company that might be able to make this happen — and if there’s enough demand for this type of seamless copy-trading of my personal portfolio, we can work on it!

I have exposure to 52 positions, right now, so the lift might take a few weeks but we’re optimistic we can get it done! All you’ll have to do is deposit money into their platform and you’ll be copy-trading my portfolio in real time.

Reply to this email and let me know, please.

In other news — nothing too much has changed.

I’m still betting big on dividend growth stocks like Tractor Supply Company, Broadcom, and Kroger. However, I have plans to expand my HIMS position.

The Dividend Growth Strategy on Quantbase is now hovering around $20,500 in value (above) — up about +3% YTD. We’re up to 139 folks who are investing alongside me toward this strategy, resulting in $161K in AUM invested in the strategy, and $384K invested across Quantbase strategies in total.

Remember, if you’re a paying subscriber to Rate of Return — you’re able to invest toward this rules-based dividend growth strategy on Quantbase for free. If you’re not a paying subscriber, the cost is $5 / month (same as a monthly Robinhood Gold subscription).

I’ve updated the holdings in the Portfolio Tracker to accurately reflect my brokerage account as of Friday close – so be sure to check those out!

Balance: $70,239 — which means we’re 3.5% toward achieving our $2M goal!

Week in Review — Too Long, Didn’t Read:

Uber reaffirms $5B in adj. EBITDA in 2024, Disney completely restructures their business, Cloudflare delivers record operating profit, Google made quite an expensive mistake, War Games may be beginning with more foreign objects entering our airspace, Russia vows to cut oil output, Consumer Credit growth slows a bit, the U.S. Consumer Sentiment is absurdly high, and breaking down Jerome Powell’s biggest issues.

Key Earnings Announcements:

Uber reaffirms $5B in adj. EBITDA in 2024, Disney completely restructures their business, and Cloudflare delivers record operating profit.

Uber Technologies (UBER)

Key Metrics

Revenue: $8.6 billion, an increase of +49% YoY

Operating Loss: -$142.0 million, compared to -$550.0 million last year

Profits: $595.0 million, compared to $892.0 million last year

Earnings Release Callout

“We ended 2022 with our strongest quarter ever, with robust demand and record margins. Our global scale and unique platform advantages position us well to accelerate this momentum into 2023.

In 2022, we significantly exceeded our profitability outlook, with an incremental margin of 10%. Our outlook for a Gross Bookings and Adjusted EBITDA step up in Q1 builds on that progress, and sets us up for yet another record year."

My Takeaway

“Is it finally time to buy stock in Uber?”

I ask myself that all of the time — especially after seeing just how strongly they bounced back from the pandemic’s headwinds. Let’s dive into their recent quarter results — then come to a conclusion.

Gross bookings clocked in north of $30B, an increase of +26% (constant currency) — but revenue grew at an even faster clip of +49%. However, this spike in revenue was further catalyzed by their recent acquisition of Transplace by Uber Freight.

What is particularly exciting about Uber’s financials is their recent stride toward GAAP profitability. During the 4th quarter of 2019 the company lost nearly -$1B, this quarter it was narrowed to only -$142M. Their operating expenses as a percent of gross bookings have declined dramatically from 16.6% in 4Q19 to 10.6% in 4Q22.

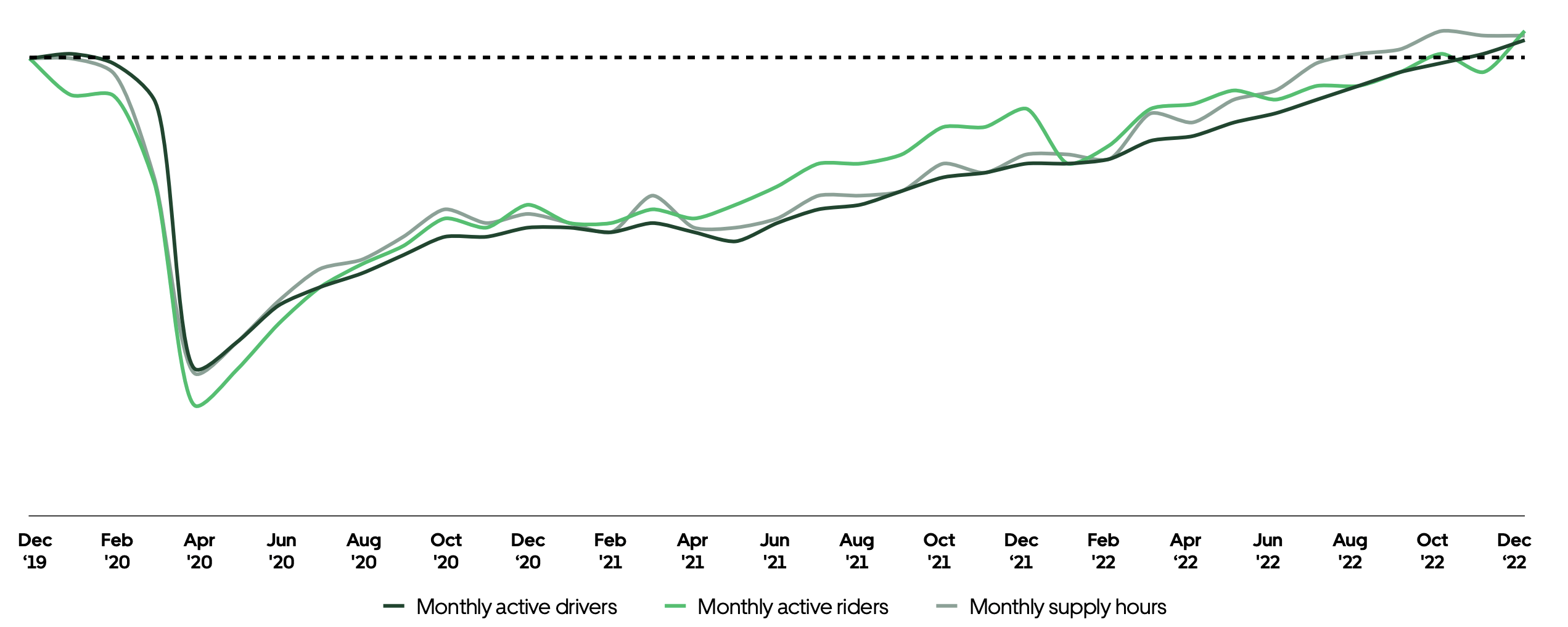

As you might recall, during the pandemic Uber’s Mobility business segment was absolutely decimated — everyone was under lockdown and had no reason to travel anywhere. The above graph proves this is no longer the case — as Uber just posted their highest ever number of monthly active customers and drivers.

More importantly, the company’s guidance for 1Q23 was higher than analysts were expecting — with adj. EBITDA coming in at $665M. They also confirmed GAAP profitability in 2023 — this could potentially pave the way for inclusion in the S&P 500.

After the recent quarter’s results — analysts are now modeling for $5B in adj. EBITDA in 2024, as well as $4.6B in FCF. Assuming this holds true — the company will report $2.30 in FCF per share in 2024. Valuing the company’s current $34 / share stock price around ~15X 2024 FCF — a healthy discount.

Personally, Uber has always been a “show me, and then I’ll believe you” company — they’re doing just that. I’m going to begin nibbling into a small position. I’m very optimistic about this one over the next 3 years.

I also want to mention that Lyft’s (LFYT) stock plummeted last week because of their very poor Q1 guidance of only $10M in adj. EBITDA compared to Uber’s $665M. Lyft is a ride-hailing-only business, where Uber is ride-hailing, delivery, and freight. There are plenty of reasons to be bearish about Lyft — those same headwinds don’t impact Uber.

Below is a real quote shared by a Wall Street analyst in their report after listening to the Lyft earnings call:

“In 22 years on the Street as a tech analyst we have listened to 1,000s of conference call with many highs and lows. Last night's Lyft call was a Top 3 worst call we have ever heard as in our opinion as management is trying to play darts blindfolded with the expense structure going forward and gave an EBITDA outlook which was a debacle for the ages.

We are downgrading from OUTPERFORM to NEUTRAL as its now clear after some ebbs and flows that Lyft's business model faces an Everest-like uphill climb to show growth while profitable in a stark contrast to big brother Uber which is moving in the opposite direction of balanced fundamentals.”

Disney (DIS)

Key Metrics

Revenue: $23.5 billion, an increase of +8% YoY

Operating Income: $1.8 billion, an increase of +5% YoY

Profits: $1.4 billion, an increase of +18% YoY

Earnings Call Callout

“Organizational changes will be implemented immediately and we will begin reporting under the new business structure by the end of the fiscal year.

This reorganization will result in a more cost-effective, coordinated and streamlined approach to our operations and we are committed to running our businesses more efficiently, especially in a challenging economic environment. In that regard, we are targeting $5.5 billion of cost savings across the company.”

My Takeaway

Probably one of the most important quarterly earnings calls this company has hosted since announcing Disney+ 5 years ago. So here’s the deal — Bob Iger is separating the business into three categories: Disney Entertainment (streaming + content), ESPN (self-explanatory), and Disney Parks, Experiences and Products (self-explanatory).

Alongside this announcement came a laundry list of others — including -$5.5B in cost reductions in 2023, their intention to give creative control back to executives, reinstatement of their dividend by the end of the year, a greater focus on core brands vs. general entertainment, and reiteration that streaming will be profitable by the end of 2024.

Bob Iger is a long-standing Disney veteran — he led the company through their two prior strategic pivots (2005 and 2016), and I have the utmost confidence he’ll be able to do it again.

I’m happy to begin accumulating shares at these ~$100 / share prices — assuming their historical 22X P/E holds true in 2025, their stock has +40% upside potential in just a few years time.

Cloudflare (NET)

Key Metrics

Revenue: $275.0 million, an increase of +42% YoY

Operating Loss: -$50.7 million, compared to -$41.1 million last year

Net Loss: -$45.9 million, compared to -$77.5 million last year

Earnings Release Callout

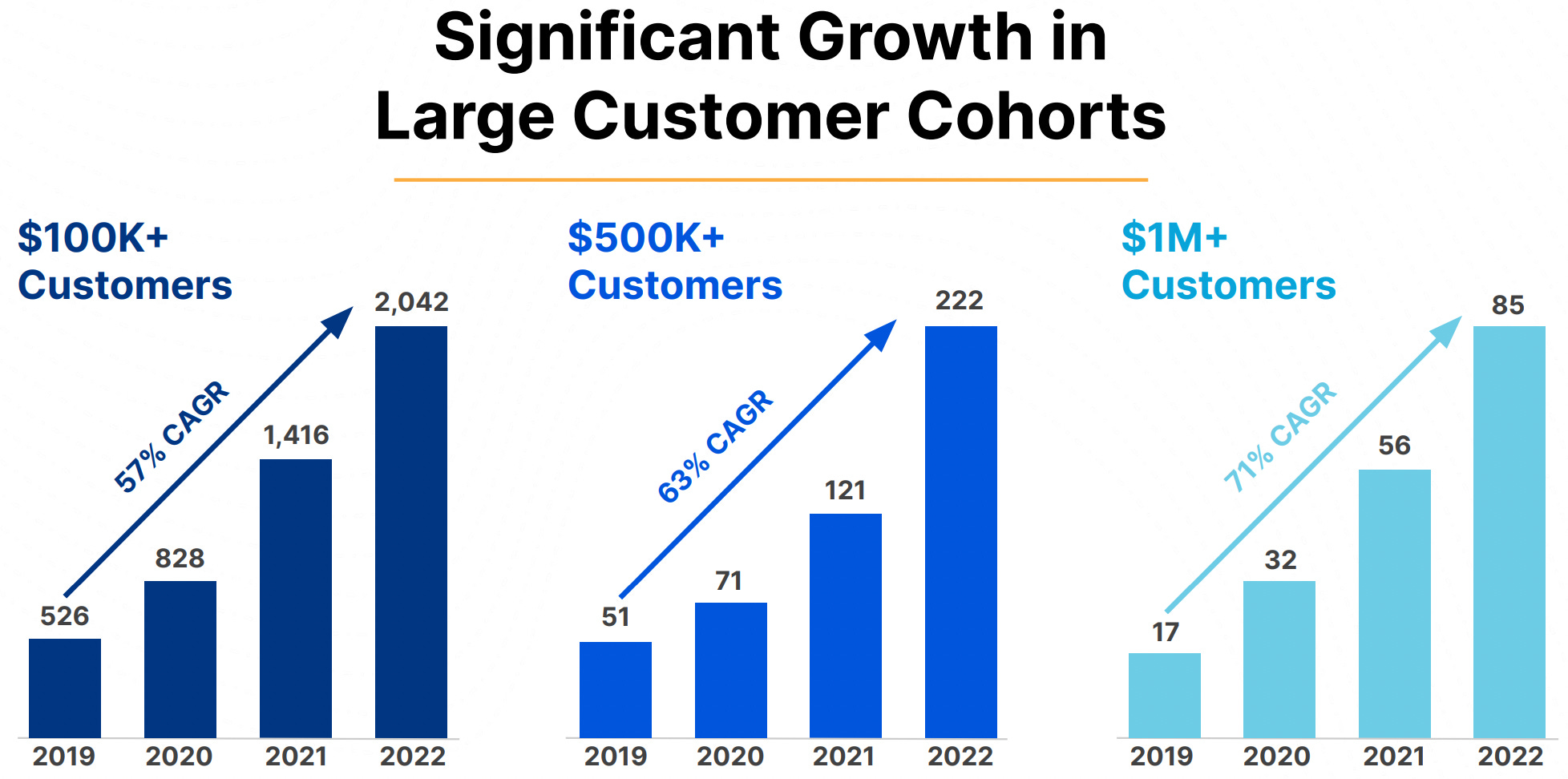

“In the fourth quarter, we delivered record operating profit, operating margin, and free cash flow. We also surpassed more than 2,000 large customers paying us over $100,000 per year and signed a record number of deals greater than $500,000.

During economic slowdowns, we believe that it's important to show discipline and optimize for efficiency.

We have our hands on the levers of our business and a full-throttle innovation engine that is the envy of the industry. There's no better time to outpace the competition and continue to deliver products on our customers' ‘must-have’ list.”

My Takeaway

I own stock in Cloudflare, and will continue to after this earnings report.

Starting with the positives — the company’s non-GAAP operating margin increased to 6%, up +0.5% YoY. Cash flow from operating activities also came in just shy of $80M, up +7.0% YoY. They now have 2,042 customers paying them >$100K annually for their services, up +44% YoY.