Still catching up on sleep from the turn of the calendar to 2023? Been focused on work and ignoring the charts? Whatever your situation — the updates below should make you feel like you were tailing the markets all week long.

Portfolio Updates:

Quick update for the week — I added screenshots to the “Performance” tab of the Portfolio Tracker so you all can see exactly how much I have invested into each company. I also included a screenshot from my Quantbase account.

The plan is to invest $10K / month toward the Dividend Growth Strategy on Quantbase (click here to invest alongside me for free) — and then invest “everything else” toward the single stocks listed in the tracker.

Important Quant Rating Changes:

Lowe’s (LOW): 3.48 to 4.91 — mind you, Lowe’s has been flashing these “Strong Buy” ratings on Seeking Alpha since late-November, so it could be another one of those.

Taiwan Semiconductor (TSM): 4.92 to 3.26 — first “Hold” rating on this stock since early-November.

Google (GOOGL): 4.51 to 3.32 — the stock has been floundering back and forth violently between “Strong Buy” and “Hold” throughout 2023, so I wouldn’t put too much weight in this.

Balance: $20,355 — which means we’re 1% of the way to our $2M goal!

Best Callouts of the Week

We’ve been bearish for about a year now, however, the market sentiment has markedly improved to start 2023. With that being said, a leg lower in the markets (at some point) remains our prediction — but it’s clear that bulls are currently in control.

The year is all-but-guaranteed to remain volatile and paying attention to updates like the ones below will continue to be important!

It’s also worth noting: ~legendary investor~ Nancy Pelosi just had a fire sale of many of her holdings — specifically, Netflix (NFLX) Tesla (TSLA), Disney (DIS), and Google (GOOGL).

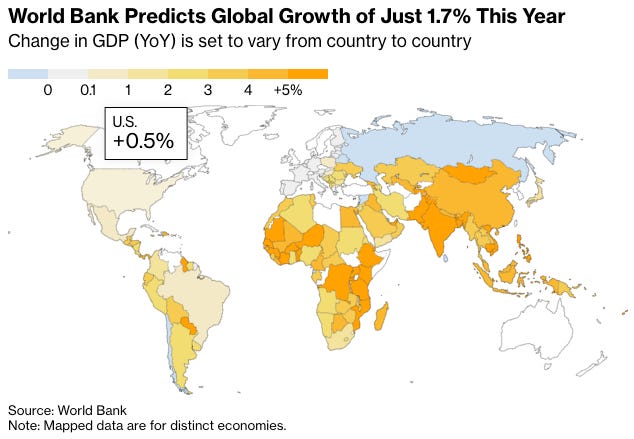

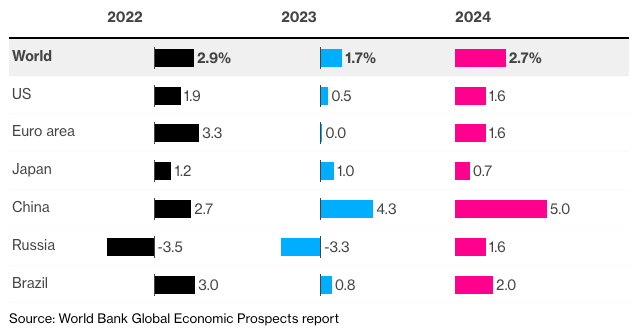

World Bank Sees Sluggishness for the U.S.

We were a bit surprised by the quietness of the media surrounding the World Bank’s recent global growth projections — depicting the United States in a tough spot.

The World Bank predicts that global GDP will rise around +1.7% this year — roughly half the forecast that it had previously published in June of 2022. If true, this would be the third-worst global productivity in over three decades.

As for the United States — we’re expected to have slower levels of growth than China for years to come and an extremely underwhelming 2023. From 1948 to 2022, the average annual GDP growth rate of the U.S. was ~3.1%.

The Collapse of the U.S. Savings Rate

Over the last couple of months, the U.S. Personal Savings Rate has hovered around 2.2% — 2.4%. The last time the level was this low was in 2006-2007 — just before the Great Financial Crisis.

We don’t need to talk about what has caused a decline in savings — we all know the answer is inflation running rampant paired with total credit spending in the U.S. continuing to rise.

But what we absolutely should talk about is what could actually happen as a result of this — a significant decrease in consumer spending has the potential to cause a pile-up of inventory that is extremely difficult to quantify and project.

One of the most interesting things about studying the Personal Savings Rate is that during the 1970s — with inflation peaking above 10% — the personal savings rate was still ~10% consistently.

The *Good* — The fact that Americans had excess savings in the 70s very much allowed inflation to continue ripping higher. Consumers continued to buy given this excess cash in their monthly budgets. This is clearly not the case today — and we’ve even begun to see inflation trend downward with no material improvement to the savings rate. However, there is a chance this could change.

Shoutout to Nick Gerli of Reventure Consulting for highlighting something that we’ve been screaming from the rooftops for almost a year now!

Week in Review — Too Long, Didn’t Read:

UnitedHealth’s revenue per patient increased +29%, JPMorgan & Bank of America foresee an increase in delinquencies, layoffs continue with Goldman Sachs & Salesforce, all flights in the U.S. were grounded for the first time since 9/11, elevated P/E averages in the market are raising the anticipation of Q1 earnings, charts that you need to see about inflation, and the biggest takeaways from Fed leadership this week.

Key Earnings Announcements:

United Health’s revenue per patient increased +29%, and JPMorgan Chase & Bank of America are both expecting delinquencies to rise in the near-term.

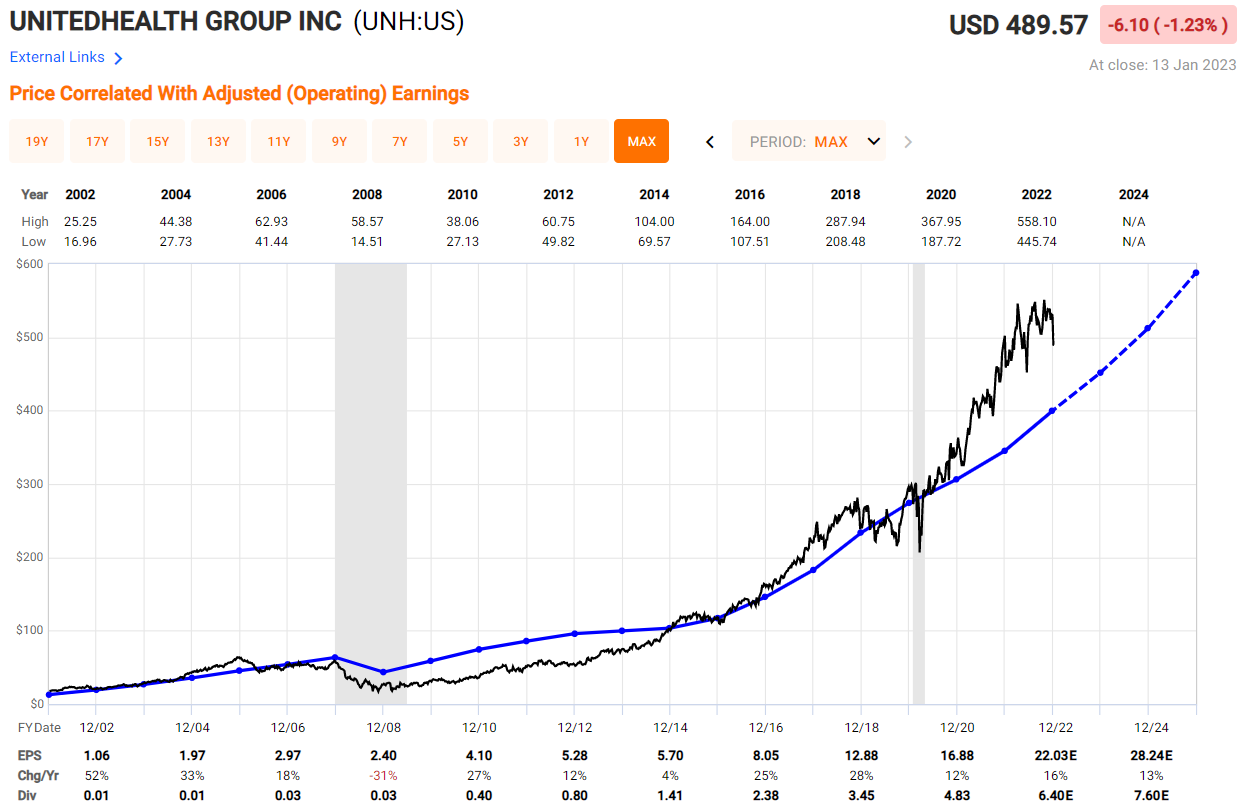

UnitedHealth Group (UNH):

Key Metrics

Revenue: $82.8 billion, an increase of +12% YoY

Operating Income: $6.9 billion, an increase of +24% YoY

Profits: $4.9 billion, an increase of +17% YoY

Earnings Release Callout

“We expect the efforts by the people of our company that led to strong performance in 2022 will define 2023 as well, especially delivering balanced growth enterprise-wide, improving support for consumers and care providers, and investing to make high-quality care simpler, more accessible and affordable for everyone.”

My Takeaway

UnitedHealth Group continues to pour billions into their five pillars for growth — with the most obvious progress being in value-based care.

The company exited 2022 with +1.8M more fully-accountable value-based patients than they had in 2021. Many of these patients have opted-in to UNH’s Medicare Advantage plans, or other MA plans powered by Optum.

Another exciting development for this company in 2023 is their focus on seniors. To remind everyone, roughly 1 in 5 Americans are 65 or older — which means this is a massive market to tend to if done correctly.

In 2023, UNH will continue to lay the groundwork in efforts to benefit from this “Silver Wave” sweeping the nation — HouseCalls, in-home testing and vaccinations, SDoHs, and other in-home initiatives they’re piloting are having an outsized impact on hospital visits.

In 2022, UNH’s in-home solutions led to a +42% increase in closing gaps in care, lowered hospital visits by -15%, and increase clinical program enrollment by +10%.

The company’s underlying fundamentals are also moving in the right direction — revenue per customer grew by +29% (driven by these value-based arrangements), and they’re expecting to serve another +750K patients in value-based arrangements in 2023 and +900K more from a Medicare Advantage perspective.

With that being said, the stock’s price seems frothy — if you’re interested in opening a position, perhaps consider dollar cost averaging over several months.

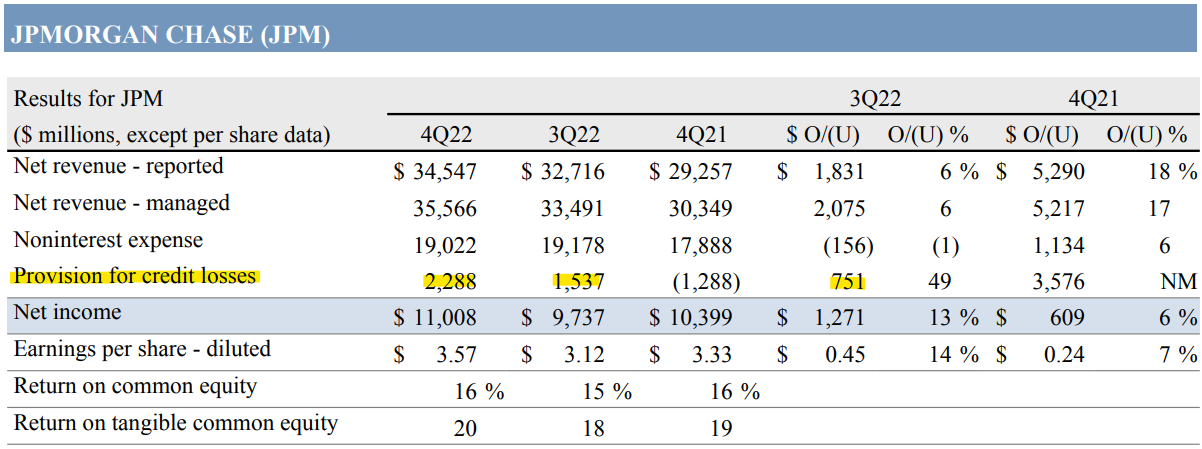

JPMorgan Chase (JPM):

Key Metrics

Revenue: $34.5 billion, an increase of +18% YoY

Profits: $11.0 billion, an increase of +6% YoY

Earnings Release Callout

“The U.S. economy currently remains strong with consumers still spending excess cash and businesses healthy.

However, we still do not know the ultimate effect of the headwinds coming from geopolitical tensions including the war in Ukraine, the vulnerable state of energy and food supplies, persistent inflation that is eroding purchasing power and has pushed interest rates higher, and the unprecedented quantitative tightening.”

My Takeaway

As you all know, I’m not an investor in bank stocks. There are so many variables that impact their success on a quarterly basis — and they’ve largely underperformed the marker over the last five years.

Instead, I like to use the information they provide in their earnings calls to better understand the current economy, their consumers, and where the “experts” think the world is headed.

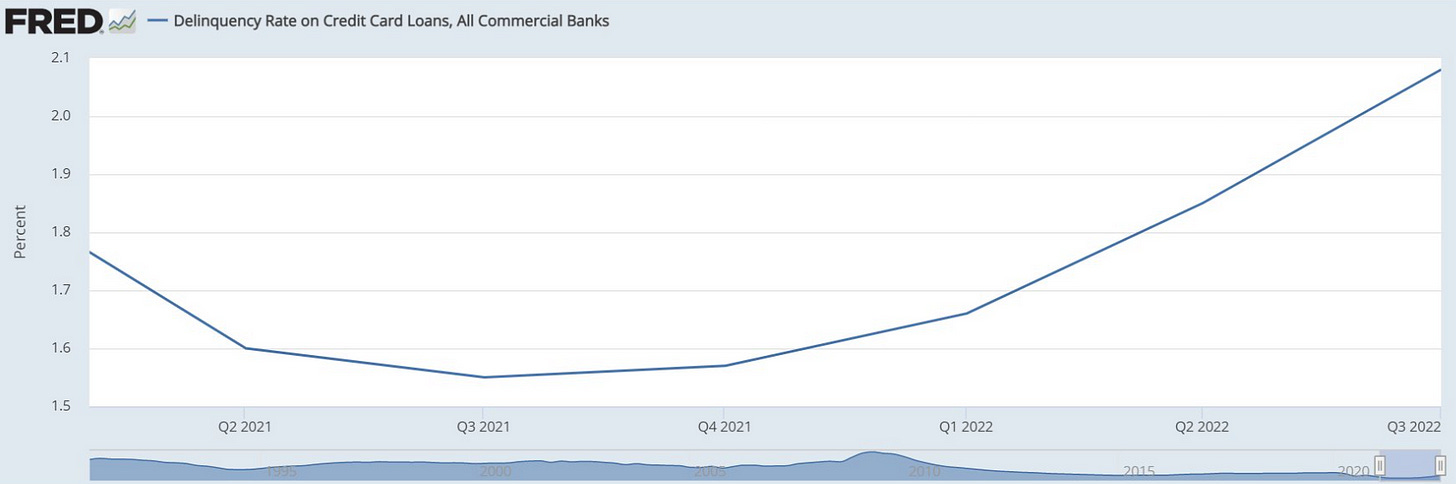

This quarter, JPM shared a tidbit of information that raised my eyebrows — their provision for credit losses increased substantially (+$751M) quarter-over-quarter. This essentially means JPM is preparing for billions of dollars worth of defaults to materialized in the near future — setting aside $2.3B in the process.

Which makes a ton of sense when you compare this growth to the spike in delinquencies we’ve seen on credit cards (below).

Remember, financial statements tell us about past performance — how a company performed several weeks ago. However, this line item is a clue into the future.

Bank of America (BAC):

Key Metrics

Revenue: $24.5 billion, an increase of +11% YoY

Profits: $7.1 billion, an increase of +1% YoY

Earnings Release Callout

“We ended the year on a strong note growing earnings year over year in the 4th quarter in an increasingly slowing economic environment.”

My Takeaway

I’ll keep this short as I already explained my stance with bank stocks above — but BAC saw the same thing as JPM re: credit loss provisions. The company is setting aside an additional +$400M to cover delinquencies in the near-term.

Below is an incredibly quote from their CEO about consumer credit card delinquencies from their earnings call..

“Credit card charge-offs increased in quarter four as a result of the flow-through of modest increase in last quarter’s late-stage delinquencies. This should continue as we transition off the historic lows and delinquencies to still very low pre-pandemic levels. Provision expense was $1.1 billion in quarter four. In addition to our charge-off provision included roughly $400 million reserve build. This was higher than quarter three, reflecting good credit card and other loan growth combined with the reserve setting scenario.

Our scenario — our baseline scenario contemplates a mild recession. That’s the base case of the economic assumptions in the blue chip and other methods we use. But we also add to that a downside scenario. And what this results in is 95% of our reserve methodologies weighted towards a recessionary environment in 2023. That includes higher expectations of inflation leading to depressed GDP and higher unemployment expectations. This scenario is more conservative than last quarter scenario.

Now to be clear, just to give you a sense of how that scenario plays out, it contemplates a rapid rise in unemployment to peak at 5.5% early this year in 2023 and remain at 5% or above all the way through the end of 2024. Obviously, much more conservative than the economic estimates that are out there.”

Investor Events / Global Affairs:

New updates for headcount cuts, the U.S. airline system has a widespread failure, and price-to-earnings ratios are questionably high.