Reminder — Week in Review posts are only for paying subscribers to Rate of Return. If you like what you see, consider subscribing below. At only $13 / month, it’s cheaper than Netflix.. and arguably more entertaining.

I spent a few hours this week compiling some of my favorite 2023 predictions across the board — specifically in relation to the economy and the stock market.

If you’re a super-nerd like me, you’ll really appreciate the below post written by Caleb Franzen of Cubic Analytics. He does a wonderful job of laying out the main factors impacting the economy. His piece is long, but full of pictures — highly recommend reading and subscribing to his newsletter if you’re into that kind of stuff.

The 2023 kick-off episode of the All In Podcast did a great job laying out macroeconomic predictions for the year. Specifically, they predict the year’s biggest political & business winners / losers, biggest business deal, best / worst performing asset, most contrarian belief, most anticipated trend & media, among entertaining banter.

Finally, I found this Google Drive that includes dozens of 2023 predictions made by folks from BlackRock, Accenture, Adobe, Deloitte, Forerunner, Expedia, JP Morgan, Shopify, and many more. I highly encourage finding the company that aligns with your respective career / industry and learning more about what could be coming your way!

My favorite is actually Pinterest. Over the last three years, 80% of Pinterest’s report predictions came true — which makes a ton of sense because before people do something they plan it.. using inspiration from Pinterest.

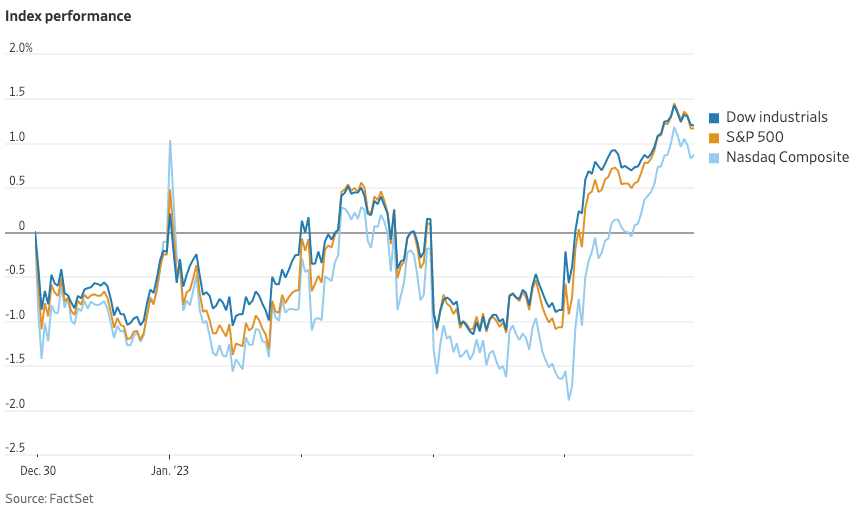

Why did the market rally nearly +2.5% on Friday?

The main factor was the signal of slowing wage growth that came from Friday’s jobs report. In December, average hourly earnings rose +0.3% from the month before — a slower increase than forecasted (after a downward revision for the prior month had already taken place).

The +4.6% annual wage growth in December was the lowest since August of 2021.

Why does this matter? Isn’t slowing wage growth a bad thing?

The Federal Reserve actually cares a lot about wage growth metrics — specifically because inflation is all-encompassing. The tools at the Fed’s disposal can directly impact things like consumer demand and real estate, but what it cannot do is make companies stop bidding up the “price” of their employees.

Takeaway:

This is positive news — as the Fed is continually moving toward accomplishing its 2% inflation goals. However, there is still so much further to go. Wall Street has lowered their consensus estimates for 2023 corporate profits, and the sentiment of Fed leadership at the bottom of this post isn’t necessarily filled with celebration.

Portfolio Updates:

Before we get started, I wanted to introduce a new section to our Week in Review posts — “Portfolio Updates.”

Since I’m updating the portfolio tracker on a consistent basis, I want to ensure you don’t miss anything — specifically as it relates to major changes in Seeking Alpha’s Quant Rating.

The first big update I wanted to share is that you’ll now see inside of our Portfolio Trackerthe names of 18 companies in the “Fun Ideas” tab. This includes their Wall Street price targets, Seeking Alpha Quant Ratings, and research. You’ll also notice a new tab called “Quantbase Strategy,” containing the 20 companies our Strategy is invested into.

Important Quant Rating Changes:

Realty Income Corporation (O): 4.13 to 4.83 — keep your eye on this one heading into the remainder of Q1.

American Tower Corporation (AMT): 3.10 to 4.78 — the first “strong buy” rating this stock has seen in the last few years.

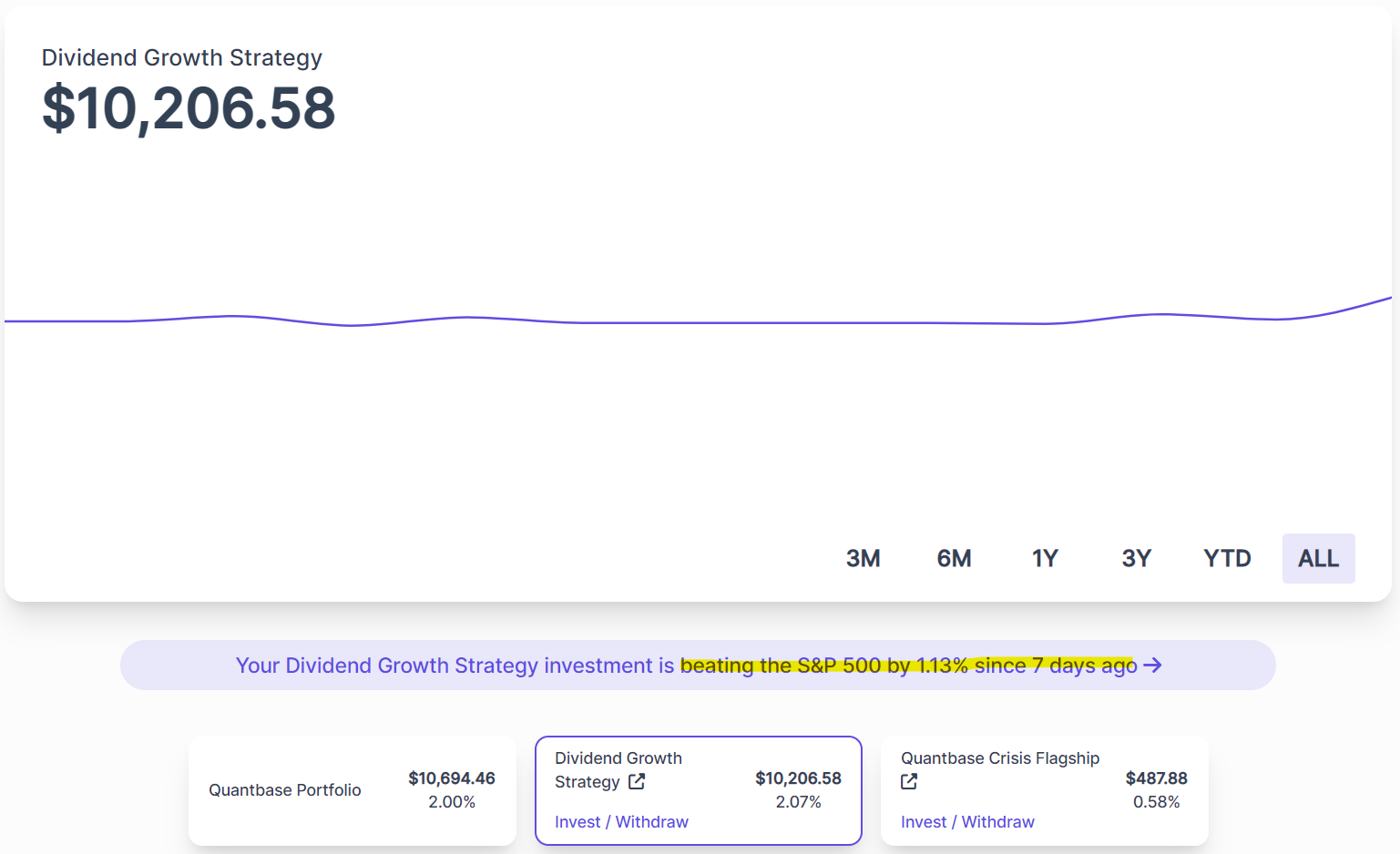

Finally, I wanted to sincerely thank the 217 people who have signed up to Quantbase to invest alongside me in the Dividend Growth Strategy. I know it’s only been a week — but we’re up +1.1% against the S&P 500.

Excited to see these returns materialize over the coming months!

Week in Review — Too Long, Didn’t Read:

Walgreens posted weaker-than-expected results despite high Covid volumes, Constellation Brands is seeing a slow down in beer consumption, Conagra Brands finally beat inflation, electric vehicles are becoming increasingly present in the United States, Bed Bath & Beyond has officially entered “dumpster fire” territory, the Consumer Electronics Show was filled with another year of head-turning reveals, the U.S. labor market shows signs of cooling, the question of the Fed cutting rates this year grows more intense, and we see direct reactions of FOMC leadership to the current market climate.

Key Earnings Announcements:

Walgreens posted weaker-than-expected results despite high Covid volumes, Constellation Brands is seeing a slow down in beer consumption, and Conagra Brands finally beat inflation.

Walgreens Boots Alliance (WBA)

Key Metrics

Revenue: $33.4 billion, compared to $33.9 billion last year

Operating Loss: -$6.1 billion, compared to $1.3 billion in income last year

Net Loss: -$3.7 billion, compared to $3.6 billion in profits last year

Earnings Release Callout

“We're making significant progress in driving our U.S. Healthcare segment to scale and profit, including the recent VillageMD acquisition of Summit Health. Our core retail pharmacy businesses in both the United States and United Kingdom remain resilient in challenging operating environments.”

Takeaway

Walgreens reported relatively sloppy results, with softer-than-expected results in all three of their operating segments.

Their core US pharmacy business came in weaker-than-expected, despite strong Covid vaccine and test volumes — operating income was down -20% year-over-year. Their International segment also posted weaker-than-expected results, and the currency conversion didn’t help.

Their guidance is forecasting a relatively fast flip in the right direction for all three of their business segments during the back-half of 2023 — and Wall Street is very skeptical they’ll be able to pull it off.

Their core US pharmacy business is forecasted to be down another -30% next quarter due to tough Covid comparables and labor investments — which means they’ll need to grow +20% in 2H23 to hit their guidance targets. For International, Wall Street is estimating profits -10% lower than guidance. WBA is convinced a change in reimbursement will help close that gap.

WBA management is optimistic that since the Summit deal is now closed it’ll begin to show profitability later this year.

From my perspective, a lot has to go right during macroeconomic uncertainty for this company to see the light at the end of the tunnel. I’m not counting them out — I just won’t be along for the ride. With that being said, I’m going to add this company to my watchlist. If they’re able to execute against this lofty vision — we might see a 2X in stock price in three years (dotted line).

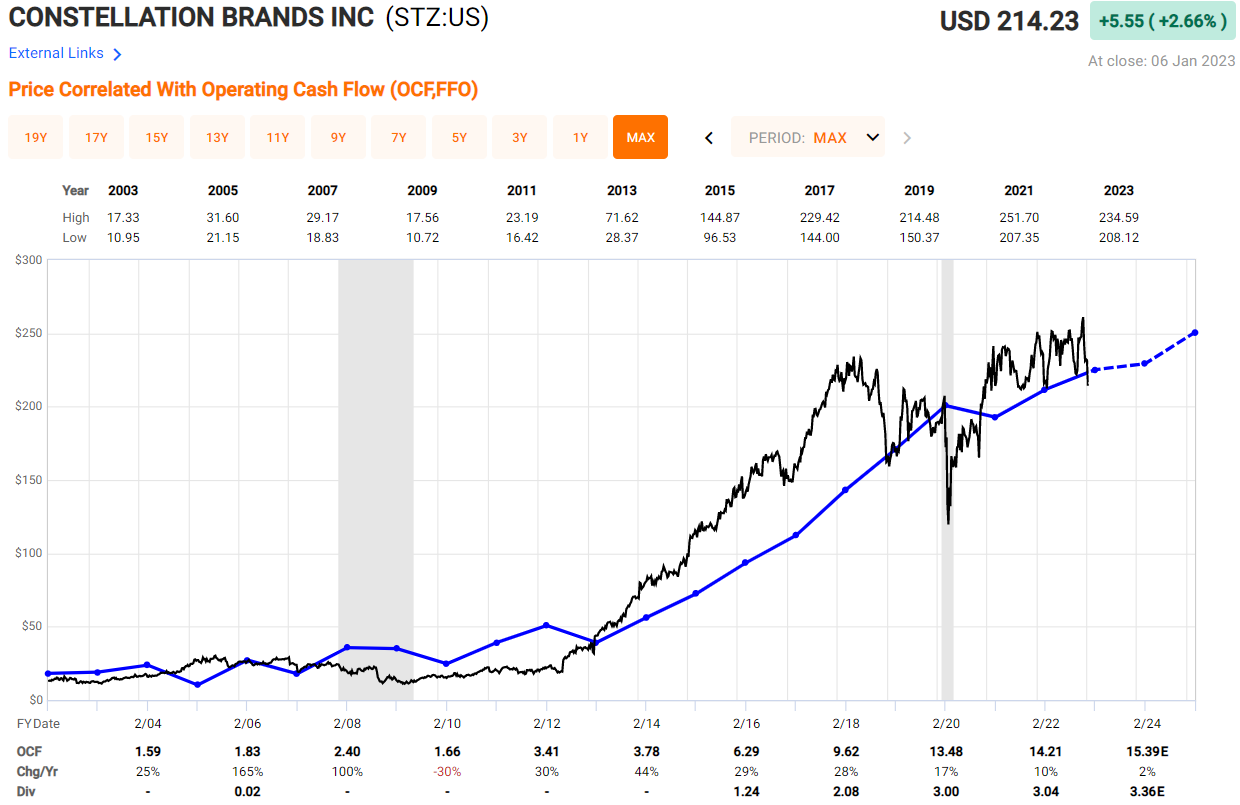

Constellation Brands (STZ)

Key Metrics

Revenue: $2.4 billion, an increase of +5% YoY

Operating Income: $746.7 million, compared to $839.9 million last year

Profits: $467.7 million, compared to $470.8 million last year

Earnings Release Callout

"Our Beer Business continued to outperform the market as the top share gainer for the sixth consecutive quarter. Looking ahead, we remain confident that we can continue to build on our strong track-record of solid growth and value creation."

Takeaway

Softer-than-expected beer depletions and commentary around pricing plans for FY23 prompted investors to question the company’s long-term growth and the resiliency of their brands. Their stock price falling -10% after the results were published showed proved just that.

The main concern for this quarter’s results is beer volume depletion (a proxy for consumption) — slowing from +8.9% to only +5.7%. In my opinion, the sequential performance in beer depletion will be a key driver for this company’s stock throughout the next 3-6 months. If beer depletion continues to slow, this might not be a temporary “trend.”

However, Wall Street believes the drop in beer depletion during the quarter was due to changes in pricing — as STZ raised prices by about +2.5% across all of their brands in October. They believe there are three main headwinds the company is facing as calendars turn to 2023 — pricing, distribution, and poor weather. The poor weather callout specifically is talking to California’s current state of emergency — the state accounts for 25% of STZ’s annual beer consumption.

Zooming out, we can see the stock is now trading below their long-standing operating cash flow average. With the near-term headwinds discussed above likely to ripple through 2023 earnings results, this lower valuation seems warranted.