📈 4.7% Return, Guaranteed

📈 4.7% Return, Guaranteed

Introducing T-Bills...

Rate of Return is not only a publication about investing and the world economy — we also talk about smart money habits and personal finance.

Introduction

In case you missed our last personal finance-focused post — Be Better with Your Money in 2023 — I’ve shared it below.

We walk through creating your first budget, investing toward retirement, and paying off high-interest debt.

This post is going to be sort of a follow-up to that one — but this go-around I’m going to assume you’ve been able to build that budget and you’re beginning to find extra money in your bank account every month that you’re not too sure what to do with.

Transparently, This is What I Do

As you all know, I’m a full-time content creator.

I make my living by writing this newsletter, sharing short-form videos on social media, hosting podcasts, and consulting fintech companies on their go-to-market strategies.

As you could imagine — there’s a ton of uncertainty with all of that.

Will Biden ban TikTok?

Will all of my Substack subscribers unsubscribe?

Will the companies I consult for lose interest?

These are all questions I ask myself — causing me to sort of live my life on my heels. Having to always be prepared for what might be lurking around the corner.

This is much different than when I was working my corporate finance job before the pandemic. I had a paycheck, health insurance, PTO, and even a 401(k) — in other words, stability and predictability.

On the contrary, I’m incredibly grateful I’ve been afforded the opportunity to do what I love every single day — create content and tell stories that educate people about personal finance and investing.

How I Save Money

As you all might know — I’m an unmarried 26-year-old with no kids living in Nashville, TN. I can only speak toward my experiences and unique circumstance — so I apologize in advance if my perspective doesn’t provide value.

With that being said, this is my current gameplan:

Pay myself a reasonable annual salary ($70K).

Live on less than I make.

Save for emergencies.

Invest the rest.

This post, however, isn’t about my salary or my budget — that was the purpose of the post linked above.

This post is all about those last two bullet points — saving for emergencies and investing the rest.

So here’s the deal — Dave Ramsey preaches his “7 Baby Steps,” and they work for a lot of people. “Baby Step 3” is to build an emergency fund worth 3-6 months of expenses — and for most people is this $15-20K.

It’s a great idea, and everyone should have an emergency fund / rainy day fund.

When it rains, it pours — and the only thing I know for certain in this world is that it’s gonna rain..

However, because of the inconsistencies with how often I get paid — I wanted to bump up my savings to 9-12 months of expenses, especially if there might be a recession in the back-half of the year.

For me, that looks like $50-60K sitting in a savings account.

If your job is also cyclical or sales-driven in-nature, you might want to consider doing the same thing!

As someone who is always looking to maximize their financial situation — having $50-60K sitting on the sidelines is a terrible idea.

Sure, it’s “insurance” against the unexpected — but inflation is also eating away at it to the tune of 6% annually.

However, this is what I’m doing to hedge against inflation..

Introducing Treasury Bills (T-Bills)

“A Treasury Bill (T-Bill) is a short-term US government debt obligation backed by the Treasury Department with a maturity of one year or less.” — Investopedia

Think of it like this — your Uncle Joe asks to borrow $100 from you so he can get his oil changed. You lend him the money and a week later he pays you your $100 back — interest free of course be you’re family.

Now this time, it’s not Uncle Joe — it’s the US Government.

So, instead of “getting an oil change” it might be “help fund public programs.”

And unlike your Uncle Joe who just needed the money until he got his paycheck on Friday — the US government needs the money for exactly 6-months.

However, after the 6-months are up the US Government buys the the Treasury Bill back from you for more than you paid — allowing you to collect “interest” on your loan.

Essentially, they’re giving you back all of the money you lent them for 6 months with “interest” on top.

Now here’s the important part — if you’re sitting on $15-20K in savings right now, it’s likely earning you between 3-4% interest assuming it’s in a high-yield savings account.

But how do you think Wealthfront, M1 Finance, and Robinhood are able to pay you that 3-4% APY on your deposits?

Because they use your money to purchase these same T-Bills paying 4.7% — pay you 3-4% and then pocket the difference.

Don’t get me wrong — buying T-Bills on TreasuryDirect.gov is hard and no one wants to actually learn about auctions, bids, issue dates, and the complicated jargon that comes with purchasing these things.

It makes a lot of sense to just collect your 3-4% and go on with your day — until now..

How to Easily Convert Your Savings into T-Bills

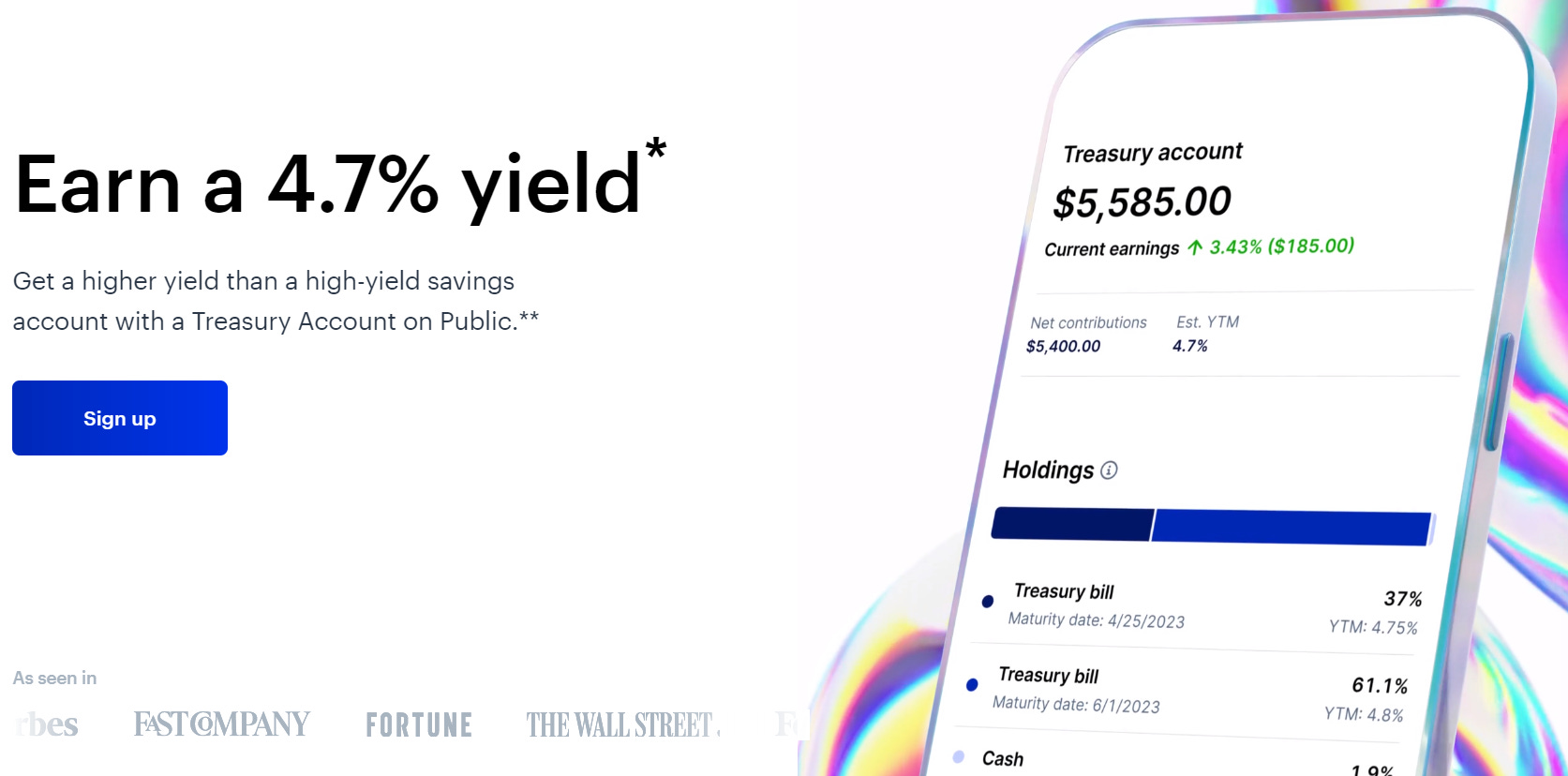

Announced just a few weeks ago, Public.com introduced a new product feature called Public Treasuries — unlocking access to 6-month T-Bills paying 4%-5% for everyone.

Here’s how it works:

“Enable” their Treasuries product

Purchase the Treasuries and collect the “interest”

It’s so simple, I’ll do it right now to demonstrate.

Mind you, only $5.2K of my $15.2K deposit cleared last week — the other $10K is still pending (as you can see below).

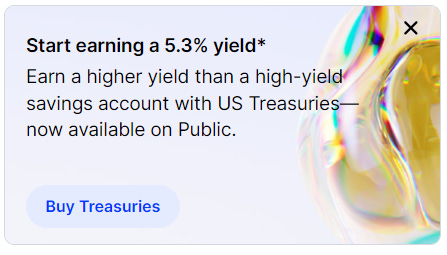

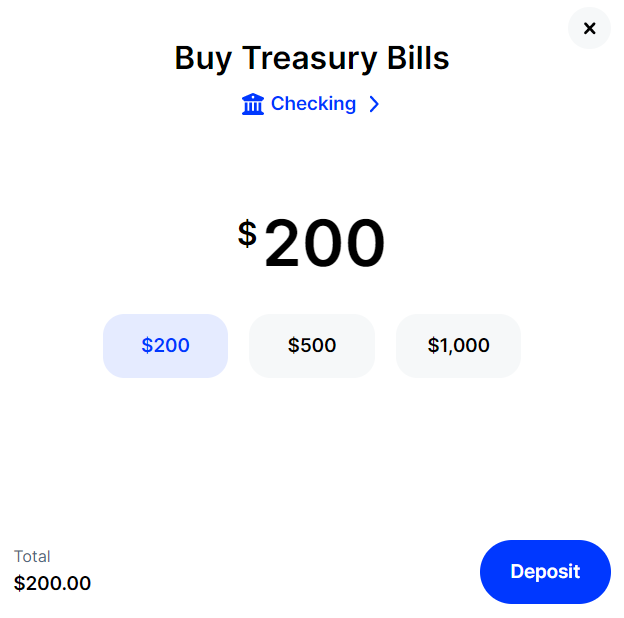

Once you’ve opened your account, you’ll see a “Start earning 5.3% yield” banner on the right side of your screen — click the “Buy Treasuries” button.

You’ll be prompted to “Enable” Treasuries — AKA agree to Public.com’s terms and conditions — once you agree, click “Buy.”

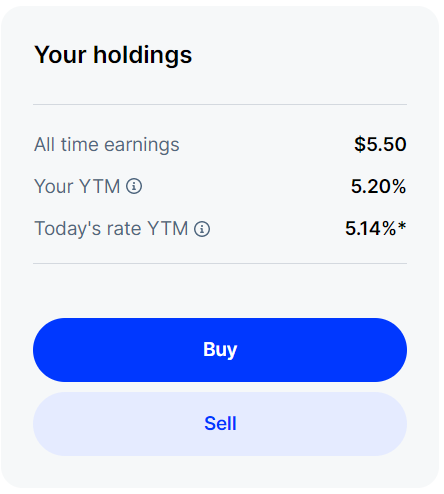

Input however much you want to purchase — in this case, I’m going to purchase another $200 worth.

Congrats!

You just purchased 6-month T-Bills from the US Government that will yield you 4-5% on your savings.

Are T-Bills on Public.com Safe?

Yes, they’re held securely in custody at The Bank of New York Mellon — the world’s largest custodian bank and securities services company.

Other Perks:

Unlike interest earned in a high-yield savings account, you are exempt from state and local income taxes on your interest income from T-Bills.

There is no lock-up period, which means you can sell the T-Bills at anytime and initiate a withdrawal back to your checking account whenever you might need the money.

In Conclusion

To be honest, a lot of people are rightfully shaken after what happened to Silicon Valley Bank. It’s hard to tell what bank might be sitting on billion dollars in unrealized losses from interest rate risk.

Despite the Fed and the FDIC guaranteeing depositor’s funds, a lot of people are withdrawing their money from regional banks and moving it into the “too big to fail” banks like JPMorgan Chase.

Personally, I’d rather move my money into the largest “too big to fail” bank — the United States Government.

These T-Bills are backed by the full faith and credit of the United States, all while guaranteeing us a healthy yield in that 4-5% range.

Here’s a link for you to sign up.

Have questions?

Drop a comment below — I’d be happy to answer them!

Learn something new and want to share it with a friend?

Use the button below!

Disclaimer: This is not financial advice or recommendation for any investment. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice.

Austin, truly appreciate your efforts, diligence, detail to investing strategies.

I have a question about something I never hear discussed on CNBC or other bloggers: $8 dividend with IEP accounting for 15% yield.

Is there a place in a retail investors strategy to include this seemingly juicy deal?

is there a way to take the money back within 6 months . i guess we will lose the interest but is it possible to cash in T bill within 6 month